By Joseph Lu, Head of Longevity Risk at Legal & General

Here are my top 3.Between 1990 and 2010, life expectancy at birth in the UK has increased by 4.2 years so the prospect of spending more time in our old age, sounds great but potentially these increased years might be spent with disabilities.

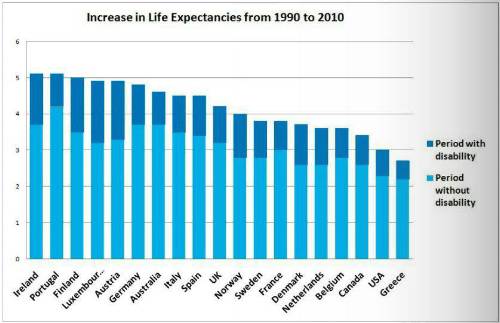

The expectation is that a person in the UK could spend possibly 3 months with physical or mental disability for every year of increase in life expectancy. Other developed countries have experienced similar trends (Figure 12).

In 2010, the top category wasdisabling illnesseswhich contribute to more than half of the total estimated number of years living with disabilities were disorders of muscles and bones including back pain, neck pain and arthritis. They accounted for over 30% of the estimated number of years people in the UK would live with disability1. The second largest contributor was mental and behavioural disorders, which includes depression, anxiety and drug use1. Diseases of the heart, brain and lungs also lead to disabilities in old age.

The number of people affected by these illnesses is expected toriseasmore of the UK population age, with on average, one person turning age 65 every 41 seconds today3. By the end of next year there would be about a quarter of a million more people above age 65 than today. The House of Lords has recently announced that there will be just over a 50% increase in people aged above 65 between 2010 and 2030 and a 80% increase in people suffering from declined brain function, which is some form of dementia, over the same period4.

This leads us to the second challengeto longevity – health and social care costs. Taking dementia,for example, the total cost of providing health and general care for UK’s dementia sufferers in 2010 was over £40,000 ( £43,760) per minute. With 55% of this care provided by unpaid carers,such as family and friends5. This is more than the equivalent care costsfor cancer, which is over £20,000 (£22,831 per minute) and heart disease at over £15,000, (£15,220 minute) combined5.As the population ages, the costs of treatment and care for chronic conditions willrise. So, it’s not surprising that the House of Lords has recently warned that the UK’s current healthcare and social care systems are inadequate to cope with the ageing population - especially with apredicted healthcare funding shortfall4. With this rather gloomy outlook on funding care in the future, its not surprising that the House of Lords has asked the Government to invent a more efficient, innovative and personalised 24/7 health and social care system.**

Finally, we have the challenge of providing for retirement, without generous Government handouts. With 87% of private defined benefit pension schemes closed to new joiners, defined contribution pensions is now a life-line for providing income in retirement for most of us4. Whilefor defined benefit plans, regulartotal contributions of 20-25% of salary, before taxis now considered unaffordable, for the newer defined contribution schemes’, average contributions of 5-15% salary are considered insufficient4. The UK’s Department of Work and Pensions estimated that there are 10.7 million people in Great Britain who can expect inadequate retirement incomes..

The 3 most talk-about solutions to this long term life expectancy conundrum, is saving more, working longer and tapping into any equity in ahome,if you have one. For many people it may be difficult to save more, especially in the currentunfavourable economic climate.The pensions industry and the government continues to try to encourage more saving in our pension funds, by showing us how much we need to save to attain a reasonable retirement lifestyle. The introduction of auto-enrolment is helping to make this happen. Legal & General’s experience shows that over 90% of eligible staff have chosen to remain in the schemes offered, rather than opt-out.

There is also the option – If you live longer so you work longer. The UK’s recent Pensions Bill has proposed to equalise men's and women's state pension age at 65 in November 2018, and for it then to rise to age 66 for both ages by April 2020.This isn’t so unreasonable if people might only spend 3 months in disability for every year of increase in life expectancy2 so they will hopefully have the remaining 9 months in good health, potentially being able to work and so earn money during that period.

People also consider that their home is their pension. According to the Office of National Statistics House Price Index, the average house price has increased by 687% between 1986 and 20126. So it seems reasonable that pensioners, who have gained from the rocketing property prices, consider this as a means of funding theirlonger life, by releasing property wealth through financial products4.

Weare experts of solving old problems by creating new ones. As we celebrate our success in solving the problem ofsomekiller diseases such as reducing heart attack death rates,we now face the challenges of having to live longer in ill health and the rising cost of healthcare and elderly care,balanced with thelack of sufficient pension income. To meet these challenges, we must radically change the current ways of providing for older agewith fresh solutions and to help address these problems for the next generationLet’s hope we all live longer to benefit from those solutions..

Sources

1. Murray and co-authors (2012). UK health performance: findings of the Global Burden of Disease Study 2010. The Lancet.

2. Own analysis of data from Murray and co-authors above.

3. Own analysis of the Office of National Statistics’ 2010-Principal Projection.

4. ** House of Lords’ Select Committee on Public Service and Demographic Change (2013). Ready for Ageing?http://www.parliament.uk/business/committees/committees-a-z/lords-select/public-services-committee/news/report-press-release/

5. Own analysis of ‘Dementia 2010: Executive Summary’. Health Economics Research Centre, University of Oxford for Alzheimer’s Research Trust.

6. Office National Statistics.

Acknowledgement

Mei Chan for sourcing the supportive graph on life expectancy

|