-

59% would struggle to pay for daily essentials without the state pension

-

Confusion over the new state pension means almost 2 million people aged 55-64 are unaware it is coming, while 16% of over-75s expect to receive it – despite being too old

-

30% of women do not know the qualifying age is increasing to align with men

-

Barely half of 55-64s (51%) realise the state pension age is rising to 69 by the 2040s

-

98% of over-55s feel the universal state pension is important to UK society

-

80% of recipients say it is important to their own retirement finances.

The winter 2015 report examines over-55s’ attitudes to the state pension and its importance to them, as well as their understanding of changes in progress to the state pension system.

It reveals 98% of over-55s feel the universal state pension is important to UK society, while 80% of recipients feel it is important to planning their own individual retirement finances. Almost one in three (32%) would not be able to cover basic living costs without it, while a further 27% would find this difficult.

Women are more likely than men to rely on the state pension: 60% feel it is very important to their individual finances (vs. 46% of men) while 68% of female recipients would struggle to cover day-to-day costs without it (vs. 51% of male recipients).

But despite its importance, Aviva’s research uncovers worrying signs that many over-55s are confused about, or completely oblivious to, the changes being made to the state pension system, even though its launch is only 120 days away.

120 days until the new state pension is born

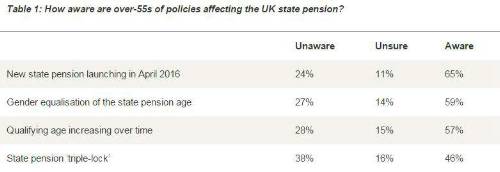

Barely two in three (65%) are aware of the new ‘flat-rate’ state pension that will launch in 120 days on 6April 2016.[1] Almost one in four (24%) are completely unaware, rising to 27% among 55-64s: most of whom will draw their state pension for the first time under the new rules. 27% of the 55-64 age cohort equates to about 2 million people in the UK.[2]

There is also significant confusion about who is and who is not affected by this change. One in six over-75s (16%) believe they will receive the full flat-rate state pension, which has a qualifying age of 65 or less for men and 63 or less for women.[3] A further 26% of over-75s are unsure if they will receive it, despite being at least ten years older than the qualifying age.

Even among the target 55-64 age group, 42% are unsure if they will receive the full flat-rate payment. The findings highlight the importance of communicating with consumers about the new system, with Government having so far issued 500,000 personalised statements to individuals telling them where they stand.[4]

Gender equalisation of the state pension age

Over-55s are even less aware of moves to equalise the state pension age for both genders (59%) than they are of the new state pension (65%).[5] Fewer women than men know that gender equalisation is taking place (57% vs. 62%), despite some women facing a longer wait to receive their state pension as a result.

More than one in four over-55s (27%) are completely unaware of this policy, including 30% of women (vs. 24% of men). Women are twice as likely as men to disagree with this policy when prompted for a view (10% vs. 5%).

Qualifying state pension age increasing

There is also limited awareness that the state pension age is rising over time,[6] especially among those who are potentially most affected. Just 57% of over-55s are aware of this policy, with 28% unaware and the rest unsure. Awareness is lowest among 55-64s (51%), 34% of whom are unaware of this change despite its potential to extend their working lives.

The research also shows less than half (46%) are aware of the Government’s flag-ship state pension “triple lock”[7]: the lowest for any pension policy measure examined by Aviva.

Most underestimate the value of the new state pension

Government data shows today’s pensioner households rely on the state pension for almost half (49%) of their typical weekly income, with 51% coming from other sources.[8] However, Aviva’s analysis raises concerns that despite cherishing the state pension, many over-55s underestimate its value and the level of personal savings needed to provide an equivalent retirement income.

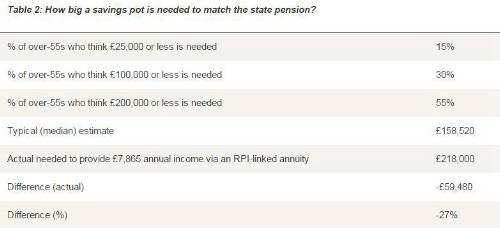

The Government had advertised that the new full flat-rate state pension will provide no less than £151.25 per week or £7,865 a year to those who qualify for it.[9] Asked how much they would need to save to generate this retirement income from their personal savings, almost one in three over-55s (30%) felt a pension pot of no more than £100,000 would suffice, including nearly one in six (15%) who felt up to £25,000 would do.

However, Aviva’s calculations show an annual income of £7,865 (equivalent to the state pension) would cost £218,000 via an RPI-linked annuity which, like the state pension, guarantees a fixed income over the lifetime of the policyholder.[10]

Compared to over-55s’ typical estimate of £158,520, it suggests they underestimate the value of the state pension by £59,480 or 27%. Only one in ten over-55s (10%) correctly identified that between £200,001 and £250,000 would be needed to match it.

Clive Bolton, Managing Director, Retirement Solutions, Aviva UK Life, said:

“It is clear from these findings the British people remain firm believers that the state pension is good for society and fundamental to their own retirement finances. The strength of these views makes it vital that Government pays heed to public sentiment as it implements its overhaul of the state pension system.

“We welcome the new state pension and the issuing of personalised statements – it is clearly an ongoing challenge to communicate the impact of changes to state provision, and we all have a role to play in ensuring that consumers have a better understanding of their pension. In particular, there are major gaps in awareness of age and gender-related changes to the qualifying criteria, especially among those people whose plans may be most affected.

“The state pension should be the foundation on which all other retirement savings are built. It is vital that people take steps to understand their entitlement and consider what actions they can take to supplement this income. People may be living and working for longer, but they still need to take responsibility for their own savings – ideally the sooner, the better. Quite simply, the prospects of enjoying financial security in later life are far greater for people with a healthy pot of personal savings and investments to boost their state pension payments.”

|