|

|

9 out of 10 UK pension funds (91%) have underperformed a FTSE All Share tracker over ten years. 72% of UK pension funds have underperformed a tracker by more than 10% over 10 years……and 37% have underperformed by more than 20%. |

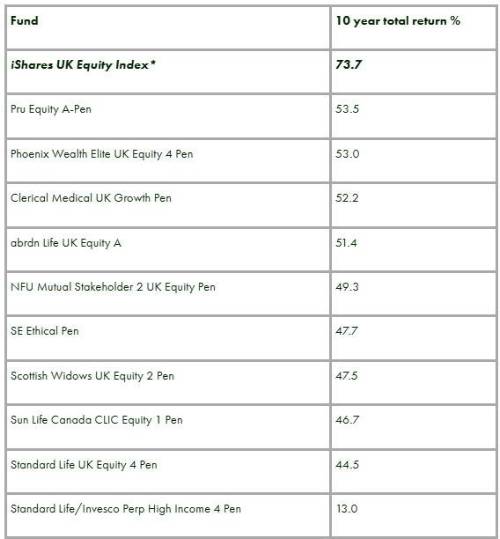

Funds from big providers like Clerical Medical, Phoenix, Scottish Widows and Standard Life find themselves significantly lagging a tracker Poor fund performance results in significantly smaller pension pots for savers Five step plan for investors to address underperforming pension funds Laith Khalaf, head of investment analysis at AJ Bell, comments: “It’s pretty shocking that nine out of ten pension funds investing in the UK haven’t beaten a simple tracker fund over the last ten years. The magnitude of some of the underperformance is equally concerning. Almost three quarters of these funds underperformed by 10% or more, and over a third underperformed by 20% or more. This doesn’t look like a market which is serving consumers well, and yet tens of billions of pounds are invested in pension funds posting disappointing performance. “This has seriously damaging effects in the real world because of the impact on the size of savers’ pension funds when they retire. If you are able to get a 6% net return on a £50,000 pension pot for 20 years you will end up with £167,357. Reduce that return to 4%, and you end up £57,801 poorer, with a pot of just £109,556. Returns from the UK stock market itself haven’t been great over the last decade, but funds which have fallen significantly behind a tracker add insult to injury. Big funds with small returns “Below are examples of some large pension funds which have underperformed an index tracker fund by more than 20% over ten years. Pension funds often have several share classes with different charges attached, and the below funds may have share classes which have performed better or worse than the figures detailed below. We have compared performance of these funds and the wider sample to the iShares UK Equity Index fund, a UK tracker fund which has an annual charge of 0.05%. Pension fund performance figures include the cost of the pension wrapper, and so to make a fair comparison we have reduced the annual return provided by the iShares UK Equity fund by 0.25% per annum to approximate returns net of platform costs.

Source: Morningstar total return to 30 April 2024. *Reduced by 0.25% per annum to approximate platform costs. Closet trackers are bad for your financial health “There are a number of factors which can lead to poor pension fund performance. Many of these pension funds were set up decades ago when there wasn’t a great deal of appetite from pension providers for investing too differently from the market. At the same time tracker funds were not widely available in the UK. The result was a horde of closet tracker funds sold to pension savers which largely follow the index, but charge fees in line with active funds. Index performance minus high fees is an equation which leads to negative outcomes for pension savers. The deep irony is some of these funds have hundreds of millions of pounds if not billions invested in them, and many aspiring active managers who are genuinely trying to beat the market through stock selection would give their eye teeth to run funds of such size. The Stakeholder boom and its legacy “Charges for older pension plans often therefore look high by modern standards, because they were set a long time ago before investment and platform costs started to fall. Many people bought Stakeholder pensions back in the early 2000s which were marketed as a low cost pension scheme and came with a regulatory seal of approval. That’s because there is a legal limit on Stakeholder charges of 1.5% for the first ten years and 1% thereafter. But you can now buy an index tracker fund for an annual charge of under 0.5% in a SIPP, and many successful active funds will cost less than 1% per annum including platform charges. “Part of the popularity of Stakeholders was driven by regulation in the early noughties. Advisers who recommended a personal pension plan were required by the financial regulator to provide an explanation of why the scheme they were recommending was at least as appropriate as a Stakeholder. The rule was known as RU64 and led to many advisers taking the path of least resistance and recommending a Stakeholder pension, complete with its regulatory halo. “Amazingly the requirement for advisers to benchmark their pension recommendations against a Stakeholder still exists in FCA rules today. It’s pretty straightforward to do this based on the wider investment options, greater functionality and usually lower charges of a modern SIPP, or indeed a workplace pension. But plenty of pension savers will still find themselves holding schemes from the Stakeholder boom of the early noughties. This is a bit like using a Nokia 105 in the land of iPhone 15s. You can make phone calls or play Snake, but posting a holiday snap on Insta would be challenging. Unfortunately the financial ramifications of holding an outdated pension can be significantly more troubling than missing out on a few social media likes. Closed books and the inertia tax “Many older pension funds are now closed to new business. A cynical interpretation of poorly performing funds would be that providers aren’t too interested in bringing them up to speed, choosing instead to invest resources in products they are still selling in the present day, and relying on pension savers not realising their funds aren’t doing too well to keep the older funds ticking along generating fees. From this viewpoint, poor performance is effectively an inertia tax. “The FCA’s Consumer Duty regulation will apply to closed books from July, which should in theory help drive improvements for investors in closed pension funds. There is still the risk that providers drag their feet, are hamstrung by the original pension fund mandates, or make improvements which still fall far short of the most competitive pension plans now available to savers. The life and pensions consolidator Phoenix Group recently put aside £70 million as the Consumer Duty might mean it has to introduce charge caps on some products and wrote the following in its latest annual report: ‘…the Group’s view is that the risk exposure around the Duty is elevated whilst the supervisory approach matures, and closed products are reviewed against the Duty’s principles, most notably fair value, ahead of the end-July 2024 deadline.’ “It remains to be seen whether the Consumer Duty will drive better performance from closed pension funds. But in the meantime pension savers can take matters into their own hands. Five step plan to deal with underperforming pension funds Step one: Assess performance “The first thing investors need to do is find out is whether their pension fund is underperforming. This is easier said than done because the information on these funds is not exactly abundantly available. The first step is to contact your provider to get a performance factsheet. Hopefully this should provide a comparison against the relevant benchmark index, which would be the FTSE All Share for most UK equity funds. If this isn’t included, then FTSE Russell provide a handy factsheet which shows the total returns of the major UK indices. Remember it’s the total return that you need to use as a benchmark as this includes dividends reinvested. If you simply google ‘FTSE All Share’ you’re likely to pull up the headline index which doesn’t include dividends, and would consequently be a poor benchmark for pension funds which receive and reinvest the dividends paid by UK companies. Step 2: Compare charges “At the same time ask your provider to send you details of the annual charges you’re paying for your pension fund so you can get an idea of whether these might be behind the poor performance. These will almost certainly include platform charges. As a rough rule of thumb you can now buy a UK tracker fund for around 0.3% to 0.5% including platform costs, and an active equity fund for around 1% to 1.2% including platform costs. Some active funds, especially multi-asset funds, cost significantly less. An FCA paper published in 2019 indicated some older pension products charged as much as 2.4% per year. It’s a recipe for retirement disaster if your fund is a closet tracker which is largely following the index and deducting high charges every year. Step 3: Check there aren’t any valuable guarantees “A few older defined contribution pension plans have valuable guarantees attached – these are usually in the form of guaranteed annuity rates or guaranteed investment returns and are often linked to investment in an insurance company’s With Profits funds. It’s worth checking if your plan has any of these attached as they may be worth hanging on for. This does depend on your personal situation and any weak fund performance also needs to be taken into account. Step 4: Escape from your fund “If you discover your pension fund is underperforming and/or has high charges, then it’s time to take action. There may be better alternatives available within your existing pension scheme, but if it’s an older plan there may be limited options, and the funds on offer may be cut from the same cloth as your existing fund. In this case you can transfer your pension to a new provider if you want to lower your charges or open yourself up to a wider range of investment options with better performance potential. Consider your current workplace pension or a SIPP as possible transfer options. To transfer you simply need to instruct your new provider to move the pension over and they will do the rest. Services like AJ Bell’s Ready-made pension will help you find old pension funds and allow you to combine them into a diversified fund easily if you don’t want to go through the process of moving each pension and choosing a range of funds to invest in. Step 5: Monitor your new pension funds “Once you have your new pension funds set up, it’s still important to keep an eye on them and make sure their performance is up to scratch. This is probably less of an issue for tracker funds which should simply do what they say on the tin, but even here over long time periods more competitively priced funds might become available. Old pension funds which now look expensive and outdated were once the latest shiny models off the production line. An annual review of your pension investments is a sensible idea, along with a check on whether you’re on track to meet your retirement goals.” |

|

|

|

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Head of Capital | ||

| London - Negotiable | ||

| Portfolio Actuary | ||

| London - £140,000 Per Annum | ||

| Deputy Head of Capital | ||

| London - £140,000 Per Annum | ||

| Senior Pricing & Portfolio Management... | ||

| London - £150,000 Per Annum | ||

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Lead Capital Actuary | ||

| London - £150,000 Per Annum | ||

| Take the lead on capital oversight | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Be at the forefront of creative GI co... | ||

| London/hybrid 2-3dpw office-based - Negotiable | ||

| Remote Market and Credit Risk Calibra... | ||

| Remote - Negotiable | ||

| Contact us about a Capital Contract i... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Head of Insurance Risk | ||

| London - £160,000 Per Annum | ||

| Director - Pensions Risk Transfer (PRT) | ||

| London, Midlands, North West - hybrid working 2dpw in the office - Negotiable | ||

| Dip a toe into public sector work wit... | ||

| Flex / hybrid 2 days p/w office-based - Negotiable | ||

| P&C Consultant | ||

| London / hybrid 3dpw office-based - Negotiable | ||

| Take the lead client-facing projects ... | ||

| Various locations - Negotiable | ||

| Choose Life! Choose a major global co... | ||

| Various locations - Negotiable | ||

| Actuarial skillset? Apply now for Snr... | ||

| South East / hybrid with travel requirements - Negotiable | ||

| Financial Risk Leader - ALM Oversight | ||

| Flex / hybrid - Negotiable | ||

| Be the very model of a modern Capital... | ||

| London - Negotiable | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd