|

|

On 7 February 2018, the International Accounting Standards Board (IASB) issued amendments to IAS19. These amendments further complicate the requirements and, in particular, have a particularly onerous knock-on effect on some Local Government Pension Scheme (LGPS) employers.In summary, the amendments affect employers with past service costs or settlements over the accounting period. If such events have occurred then all assets and liabilities are to be ‘re-measured’ using assumptions applicable at the time of each of the events. |

By Nicola Tait, Actuary at Barnett Waddingham On the face of it, this might seem like a simple and sensible enough change. Indeed, the IASB’s view is that this amendment will provide more useful information to users and enhance their understanding of financial statements. However, as we set out in this article, the amendment complicates the preparation of accounting disclosures considerably. We therefore question whether it has any real benefit for LGPS employers and, in particular, the users of their accounts.

About the amendment As many of you will be aware, these types of events are not uncommon for LGPS employers and multiple ‘re-measurements’ may be required over an accounting period as a result. The more re-measurements we need to do, the more complicated things get. (We explain further below.) These amendments are therefore particularly onerous for major local authority councils, who experience these types of events frequently throughout the year.

The old 'simple' approach This meant that we could calculate the amounts at the start of the year and any settlement/curtailment events could be dealt with separately, outside of the main roll-forward calculations, all using a single set of assumptions.

The new, amended approach This means that we end up with lots of mini accounting periods for which we need to calculate the P&L items separately, then add them all up at the end. So, for example, if an employer has five events over the year we essentially have to prepare accounts for six separate periods and then collate them all together. Rather you than me, you might say! Although the balance sheet position won’t change, the amounts recognised in the P&L and re-measurements in other comprehensive income (ROCI) will. So we’ve included an example towards the end of this article to help illustrate the changes. As an added complication, the projected pension expense will also now be less accurate, under the amended approach, if a material event is expected to occur. It’s impossible (even for us actuaries) to allow for future changes in market conditions until that date has actually passed.

When does the amended approach need to be used? It affects any employers reporting under IAS19 (typically the major councils) For employers that report under FRS102 (typically colleges and academies), there is no explicit requirement to adopt a similar approach yet, although the precedent is to follow suit The amendment does not need to be applied where its application is immaterial. In that instance the old simple approach can be used The assessment of materiality will therefore be key and is subject to each employer’s individual circumstances and auditor’s discretion. We can assist by providing additional information to help assess the materially of each event. However, we cannot conclude whether it’s actually material or not in our role as actuaries. This is an auditor decision. The Chartered Institute of Public Finance & Accountancy (CIPFA) is due to publish its Code of Practice on Local Authority Accounting in the United Kingdom 2020/21 in April 2020. This will incorporate changes relating to these amendments. We also hope it will provide more guidance on the assessment of materiality of an event. We recommend that all employees consider whether they wish to allow for this amended treatment, discuss it with their auditors, and let their actuary know! Due to the tight timescales put on employers to finalise their accounts, it will be much easier if the approach can be agreed in advance.

Let's look at an example In this example, £1m of liabilities and £0.8m of assets were transferred from the employer to the new contractor using accounting assumptions determined at the start of the year.

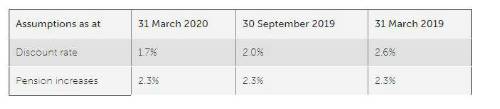

Assumptions For our example we’ve assumed the following assumptions are applicable at these dates. Please note, however, they are for illustration purposes only and do not represent market conditions at the respective times.

The balance sheet

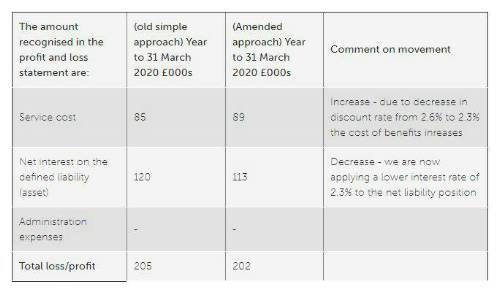

P&L statement This could either increase or decrease these items. That depends on the direction of change in assumptions and the relative value of the assets and liabilities involved. In our example, the discount date has decreased and pension increases have stayed the same, increasing the service cost and decreasing the net interest cost as shown below.

The magnitude of the effect here does really depend on the size of the event and the extent of the change in the assumptions applicable at the various dates. So this will be important to consider when assessing materiality. It is worth noting that the change in assumptions is actually more important than the actual size of the event when assessing materiality. This is because the change in assumptions will have a greater financial effect, due to the fact that we end up ‘rebasing’ the service cost and interest cost so that they are based on the revised assumptions.

Re-measurements These items, together with the ‘liabilities assumed on settlements’ item that goes directly into the defined benefit obligation reconciliation, will generally absorb the full amount of the P&L change. Essentially, this amendment moves items between the P&L and other areas of the accounts.

Is all the extra work worth it? The balance sheet figures are unaffected by the amendment so if those are the figures you are most concerned about, do you really want to complicate the adding up? For users who are more concerned about the amounts recognised in the P&L and the ROCI, do you believe the benefit of incorporating various changes in assumptions throughout the accounting period outweigh the additional work involved?

What are our views? However, we are happy to give employers the information they need to help determine the materiality of the changes. Given the complexity (and the fact that the amendment is now in place), we’re also putting together a webinar with the aim of helping employers through these issues and other key points to note for this year’s accounting exercises. (Unfortunately this isn’t the only complication. We haven’t even mentioned McCloud or GMP yet!) Further details will be released on our website shortly, so watch this space. As always, we are happy to talk to Funds or employers (and their auditors) about any accounting queries. We would always recommend that as much as possible is agreed with auditors before the year-end in order to ensure employers’ deadlines are met. |

|

|

|

| Take the lead client-facing projects ... | ||

| Various locations - Negotiable | ||

| Choose Life! Choose a major global co... | ||

| Various locations - Negotiable | ||

| Actuarial skillset? Apply now for Snr... | ||

| South East / hybrid with travel requirements - Negotiable | ||

| Financial Risk Leader - ALM Oversight | ||

| Flex / hybrid - Negotiable | ||

| Be the very model of a modern Capital... | ||

| London - Negotiable | ||

| Pensions Actuary seeking a high-impac... | ||

| London or Scotland / hybrid 3dpw office-based - Negotiable | ||

| Great opportunity for Pensions Actuar... | ||

| London or Scotland / hybrid 3dpw office-based - Negotiable | ||

| Responsible Investing Manager - Clima... | ||

| London/Hybrid - Negotiable | ||

| Quant Strategist | ||

| London/Hybrid - Negotiable | ||

| Multiple remote longevity contracts | ||

| Fully remote - Negotiable | ||

| Multiple remote inflation hedging con... | ||

| Fully remote - Negotiable | ||

| Play a vital role in shaping a new He... | ||

| London or Scotland / hybrid 50/50 - Negotiable | ||

| Support the Longevity team of a globa... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Delve into financial risk within a ma... | ||

| Wales / South West / hybrid 1dpw office-based - Negotiable | ||

| Project-based Life Pricing Actuarial ... | ||

| South West / hybrid 2 dpw office-based - Negotiable | ||

| Pricing Actuary | ||

| London - £120,000 Per Annum | ||

| Develop your career in motor pricing | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Experience real career growth in home... | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Be at the cutting edge of technical p... | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Use your passion for innovation and t... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd