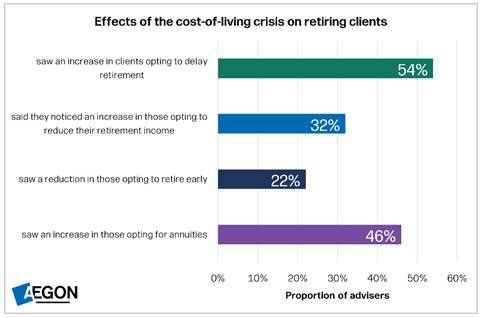

Working longer and taking less – 54% of advisers said more clients are choosing to delay their retirement, and 32% have received more client requests to reduce their retirement income.

But stick to the financial plan – In spite of the recent economic environment, 70% of advisers recommend that concerned clients stick to their existing financial plan.

While inflation is now returning to target levels and economic performance slowly improves, findings from Aegon’s latest Adviser attitudes report show how recent financial challenges have been impacting financial advisers and their clients.

Of the 200 advisers surveyed by Aegon’s research partner, Opinium, 33% reported having received an increase in queries from clients since 2021, with older clients the most eager to understand how they should adapt their financial plans to reflect the difficult economic environment (58% of queries came from over-55s).

In adapting to meet these challenges, according to 54% of advisers, the most common action taken by clients was to delay their retirement in favour of working and saving for longer. This was followed by an increase in the number of clients choosing to take an annuity (46% of advisers had experienced this), and a jump in those reducing their retirement income (32%).

Data source: Adviser attitudes report. Aegon UK, August 2024.

Despite the growing number of advised clients choosing an annuity, only 11% of client assets are held within them. Instead, it’s clear that drawdown remains the dominant investment strategy for most retirees, with 67% of client assets invested in such solutions.

Moreover, 70% of advisers believe that sticking to your current financial plan is the best recommendation for clients who are concerned about financial challenges. This is far greater than the second-most common recommendation, with only 9% suggesting their clients should switch investments.

Lorna Blyth, Managing Director, Investment Proposition, comments on the findings: “Our research shows that the UK’s savers and retirees have been struggling to catch up after three years of significant financial challenges.

“Professional financial advice is a hugely valuable part of financial planning, but never is this more apparent than in difficult economic times. The fact that a third of advisers have reported an increase in queries from their clients is further evidence of that, with the work done by advisers in the past few years having been a vital and appreciated support mechanism for many.

“It’s also not a huge surprise that over-55s represent the bulk of queries posed to advisers, given many of them will likely be close to or in retirement, and so have less time to combat and recover from recent challenges.

“It’s interesting to see how recent times have changed advised client behaviour, too, particularly when it comes to delaying retirement. As financial challenges have mounted, many pre-retirees may have been concerned that their savings would be unable to meet rising costs now, let alone in the future. The result is a greater proportion of advisers seeing their clients choose to continue earning and saving for longer, possibly until they feel their retirement income will be sustainable.

“With interest rates having been much higher, it’s also not necessarily a surprise that 46% of advisers we spoke to have seen an increase in the number of clients choosing to purchase an annuity. However, despite becoming more popular, they still only represent 11% of the market by assets held.

“Considering many will have sought greater security during the recent challenges, you would have thought that if annuities were to have their day, it would be now – but it doesn’t quite seem to be the case. It’s clear that drawdown remains the dominant retirement strategy for most retirees.

“Reassuringly, it would appear that advisers have been keen to focus on long-term outcomes, with 70% recommending their clients stick to their original financial plan. Retirement saving is a long-term game and making changes that benefit short-term needs could hurt your pension when you need it most in the future. This is a great example of advisers applying their expertise to produce better client outcomes.”

|