|

|

EB: In the first article you established that GIP was a product you were focused on as it is at risk of stagnating and extinction. Is AE for GIP really on the table? PA: I feel like a lone voice, or perhaps I am a classic marketer who believes in product lifecycle-introduction, growth, maturity, decline? We are at decline with no new employers and fewer every year buying GIP! AE has to be the answer as what else is? Swiss Re’s 2013 Group Watch Survey advised: ‘The response remains split on the case for extending the AE model into simple products and specifically those used to protect income1.’ In the report one insurer commented: “No. We have a mandatory scheme in SSP. It’s a stretch too far at the moment – the focus should be on incentivising employers to provide GIP2.” An employee benefit consultant commented: ‘In theory it is a good concept but difficult to achieve with simple products meeting a high level of these needs. Employers are looking to reduce costs for group risk products and AE for pension costs. This would be made worse if legislation were to be introduced for disability benefits3.’ Hence, while I acknowledge that the industry is not aligned, I simply do not believe that GIP incentivisation is the answer. Looking at the first article in this series, I am genuinely concerned at the clear naivety and lack of customer understanding in some of my peer and supplier group when they believe that financial incentives are the answer. They are not the answer. I am almost incensed with their lack of foresight and the critical state this product is in, bearing in mind our commitment to it, and they should start listening to their employer customers. There are, however, some positives – GIP AE is being discussed with many conceding, as the 2014 Group Watch report highlighted: ‘That this is a “long- term game”, with little government appetite to extend the concept until pensions auto-enrolment has been completed4.’ They are exactly right. As we hit 2018 and every employer is paying 3% towards pensions contributions, it is only then that any change should be considered. In the interim we have a clearly challenging role to simplify state benefits and the tax regime associated with individual and group income protection.

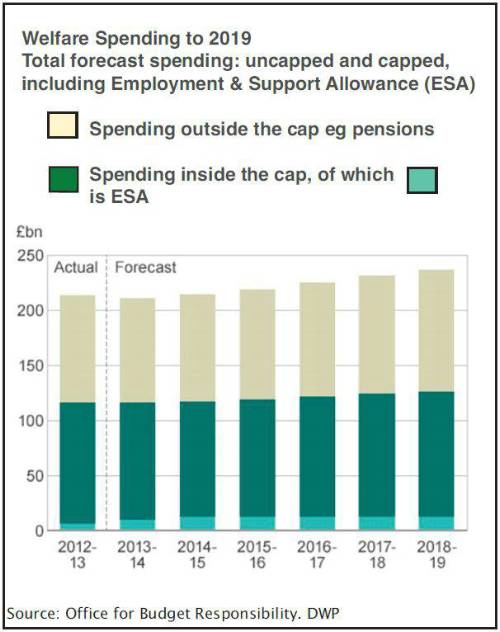

EB: You mentioned the need to simplify state benefits and mentioned in the first article that the state has a major problem in supporting the sick and disabled in society. What is the Government doing to address this problem? PA: Whichever way you look at it, the Government is in trouble and the cost of ESA is projected to rise by £13.3bn between the current financial year and 2018-19, and has been described by the DWP as "One of the largest fiscal risks currently facing the government". In simple terms it is fair to say that already state benefits cannot be relied upon – unless you have the profile of no savings, a mortgage under £200K, a number of children with no additional bedrooms and can live under £500 per week! The biggest demographic that needs support is that of single people and couples in rented accommodation but the current system is more supportive of families with children. The Work Capability Assessment, used to assess whether a claimant qualifies for benefit is, put simply, broken. The Work Capability Assessment has, in the words of The Work Foundation, ‘Reached an unsustainably low position. More specifically, we are concerned that the credibility of the assessment process among claimants and patient advocacy has been severely undermined. We argue that, although the WCA is based on sound intents and principles, more must be done to improve the ‘face validity’ of the assessment process and the WCA tool as a credible assessment for work-related functional capacity5.’ Is it acceptable that 700,000 people are waiting for an assessment? We then have the poor implementation of the Personal Independence Payment, which is replacing the current DLA benefit andhas been described by MPs as a, ‘Fiasco’. This has resulted in claimants waiting, on average, 107 days for a decision on their case, while terminally ill people are waiting 28 days6 for decisions on their cases – a fact which Macmillian Cancer Support calls ‘Appalling’7. Another area of concern is the launch of Universal Credit, a single payment which will replace 6 benefits. Concerns have been raised at the speed of implementation, with ministers failing to deliver on their promise of 1 million people8 to be on the scheme by April 2014. Other concerns raised include how even a single penny of income will strip you of any rent/mortgage support, and how ‘The mechanisms being put in place to support vulnerable claimants of UC will be inadequate9.’ Clarity will really be seen when Universal Credit is successfully rolled out and the impact on individuals is fully apparent noting Labour’s comment to pause it if it gets into Government. The complexity and implementation of the UK welfare system needs to be addressed, which is why I am urging revolution and not evolution as the latter is clearly not working for anyone in the process. EB: What about the planned Health and Work Assessment and Advisory Service – billed as a service providing occupational health assessment to help people with a health condition to stay in or return to work? Prior to the launch of this service, it is already being scaled back. Initially, the DWP estimated that the Health and Work Service would be able to help between 350,000 and 700,000 people each year, between 40% and 80% of the population of employed people who have been absent for a period of 4 weeks or more. The Service has now slashed the optimum referral range to between 229,000 and 457,000 employees per annum, so that’s a cut in support of around 35% and further action may be taken to control this number. In addition, the tender document issued by the DWP for the Health and Works Service said that there may be changes required during the life of the contract to facilitate an increase or decrease in the number of employees being referred to the assessment process. It noted options to reduce the number of referrals including changing the qualifying period to after 4 weeks of absence for GP referrals, restricting employer referrals and potentially limiting workers receiving other certain benefits. In short, there are major concerns over the Work Capability Assessment, Universal Credit implementation, the Health and Work Service being scaled back prior to launch and DLA moving to PIP. Are these measures by the State really going to reduce the disability bill and retain people in work? I would argue no, but income protection as per the Dutch model is the answer they are actually looking for. EB: You argue that a system similar to that in the Netherlands is the answer - so what happens in the Netherlands when an employee is ill? PA: The Dutch model provides a clearly mandated rehabilitation programme provided by the employer, with an infrastructure that is supported by a private sector and state partnership. For the first two years in which the employee is absent through sickness or disability, the employer is required to pay at least 70% of the employee’s salary, up to a salary cap of €51,414. Many employers, motivated by staff attraction and retention, pay up to 100% of the employee’s salary. The employer has a legal requirement to provide support and rehabilitation with early intervention, with the employer and employee needing to have agreed a plan after 8 weeks. If employees are still absent after two years, the state then takes over. Similar to the UK, claimants are assessed against an ‘any occupation’ definition using objective tests. If the claimant is deemed to be over 80% disabled they qualify for the full state benefit of 70% of salary up to the cap, rising to 75% of salary if their disability is permanent. If the claimant’s disability is between 80% and 100%, but not expected to be permanent, then the benefit is 70% of the salary up to the cap while rehabilitation continues. If deemed between 35% and 80% disabled with the possibility to be re-integrated into work there is a benefit of 70% of the salary gap between the pay for work undertaken and previous earnings. Employers can opt to pay the benefits of the latter two previously mentioned in return for lower national insurance contributions. There is an element of employer choice here. EB: How are the Dutch state benefits funded? The employer makes payments to cover the state benefits through a payroll tax, with the amount of contribution based on an activating system10, also called an experience rating: employers with many ex-employees on disability benefits pay higher contributions than employers with fewer employees on disability benefits. There is also adjustment given for different sectors of the industry. Currently, in 2014, the standard contribution rates are 4.95% of salary, up to €51,000. An extra 0.69% is paid if the employer does not accommodate the partially disabled, and a further 0.34% is paid if the employer does not accommodate for sickness partial disabled. Again, the employer has a choice in paying these rates and if confident in their rehabilitation schemes, can only pay the basic 4.95% rate. EB: Is the Dutch model considered a success? PA: Without these reforms it had been projected that 17% of the Dutch working population, 1.2million, would have been in receipt of disability benefits by 204011. Instead, due to the reforms and focus on rehabilitation, the number of claimants on state benefits has fallen from 100,000 in 2000 to 40,000 in 201012. The Government has shown that they understand the sickness absence process in the Netherlands, as it was assessed in the Frost/Black independent review of sickness absence13. In the report two specific concerns were raised over the Dutch system: • The possibility of potential employees being disadvantaged through being higher risk would go against the message of the Disability Discrimination Act and make life more difficult both for employers and those with health conditions. • The British economy is currently emerging from a recession. Part of the Government’s plan for recovery is to stimulate small and medium- sized businesses. Placing a burden of this scale on them would clearly not help The first concern stating that disabled people would be at a disadvantage is not technically correct. Where an employer has a group income protection scheme, employees can receive an amount of benefit without the need for medical underwriting – a ‘free cover’ limit. There is still a duty on the adviser to disclose health conditions if they are aware of them, but everyone is assumed to be 100% healthy in that ‘free cover’ limit and actively at work when the scheme starts. The second concern that implementing a system like the Dutch model would place a burden on small and medium businesses ‘post-recession’ is remedied by the fact we are not talking about compulsion. I am not saying that everyone has to pay 5%, and we are not saying that you have to pay 0.5-1% on top of your pension contribution. We are proposing that with the next pension increase take half a percent and allow employers to opt in to a disability product. Most employers in my view will choose the disability cover because it serves a clear business need – retention, sick pay, equality act, SSP/OSP payments and so forth. If we can overcome the concerns raised in the Frost/Black review then the Government should be open to a discussion on auto-enrolment style GIP. EB: Do you have any evidence to support that AE for GIP would work in the UK? PA: When the government launched stakeholder pensions in 2001 the plan was that they would be an easy, low cost, easy to access pension the employer had to offer by law. This would encourage more long-term savings for retirement, particularly for those on low to moderate incomes. The plan was a simple one – you turn up at, say a supermarket, you pass over your credit or debit card and you get £20 paid into your pension. It could not have been simpler, but it did not work. Consumers did not suddenly rush out and start saving, with only 1 in 3 private sector employees saving toward a workplace pension. As a result, from October 2012 the rules on stakeholder pensions changed with employers no longer having to offer these, with the government introducing AE. So some level of paternalism is needed to get people to save and it is the same with disability protection-people do not buy it for themselves-this has been acknowledged elsewhere. The Government, via the Sergeant review, has recognised that consumers are not purchasing enough financial products to meet their needs in times of difficulty, hence the simple products work that has been going on in our industry. Work on a simple income replacement product review has started under the stewardship of the ABI and Grid with a focus on workplace distribution. This programme of work on simple products is floundering under the weight of the complexity of both state benefits and taxation of group and individual income protection, and as a result no one should believe that a simple product will be easy to deliver as the underpin to an AE GIP style product. EB: Can you really see a similar system being successfully implemented in the UK? PA: I view the Dutch model as an ideal solution. I am not saying that the UK would immediately adopt the Dutch model, because we do not want a compulsory payment. We should give employers the choice of a pension or a pension plus a disability product with a simple opt-in option. Disability benefits provide a problem to a business issue today and not a personal or state one tomorrow. We have a successful model for GIP AE and it is a model that works. Everything points to a viable model, but what are the benefits of implementing such a thing? This is a question which I will address in the final article of the series.

1. http://media.swissre.com/documents/20130424_GroupWatch2013.pdf |

|

|

|

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Head of Capital | ||

| London - Negotiable | ||

| Portfolio Actuary | ||

| London - £140,000 Per Annum | ||

| Deputy Head of Capital | ||

| London - £140,000 Per Annum | ||

| Senior Pricing & Portfolio Management... | ||

| London - £150,000 Per Annum | ||

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Lead Capital Actuary | ||

| London - £150,000 Per Annum | ||

| Take the lead on capital oversight | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Be at the forefront of creative GI co... | ||

| London/hybrid 2-3dpw office-based - Negotiable | ||

| Remote Market and Credit Risk Calibra... | ||

| Remote - Negotiable | ||

| Contact us about a Capital Contract i... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Head of Insurance Risk | ||

| London - £160,000 Per Annum | ||

| Director - Pensions Risk Transfer (PRT) | ||

| London, Midlands, North West - hybrid working 2dpw in the office - Negotiable | ||

| Dip a toe into public sector work wit... | ||

| Flex / hybrid 2 days p/w office-based - Negotiable | ||

| P&C Consultant | ||

| London / hybrid 3dpw office-based - Negotiable | ||

| Take the lead client-facing projects ... | ||

| Various locations - Negotiable | ||

| Choose Life! Choose a major global co... | ||

| Various locations - Negotiable | ||

| Actuarial skillset? Apply now for Snr... | ||

| South East / hybrid with travel requirements - Negotiable | ||

| Financial Risk Leader - ALM Oversight | ||

| Flex / hybrid - Negotiable | ||

| Be the very model of a modern Capital... | ||

| London - Negotiable | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd

In the second article of a landmark series to champion AE for GIP, Canada Life’s Paul Avis discusses with Editor Ellie Burns how we need to look to the success of the Netherlands, and how the Dutch model could be the answer to a stagnating product at risk of extinction, as well as the answer to a complex welfare system which is repeatedly missing the mark.

In the second article of a landmark series to champion AE for GIP, Canada Life’s Paul Avis discusses with Editor Ellie Burns how we need to look to the success of the Netherlands, and how the Dutch model could be the answer to a stagnating product at risk of extinction, as well as the answer to a complex welfare system which is repeatedly missing the mark.