Analysis of the Financial Conduct Authority’s (FCA) Financial Lives Survey1 from leading independent consultancy Broadstone, reveals a worrying gap in trust and engagement in pensions which is at its widest among younger savers.

The regulator’s seminal survey asked pension savers with at least one Defined Contribution (DC) pension that hasn’t been accessed how much trust they had in their pension provider on a scale of 1 to 10.

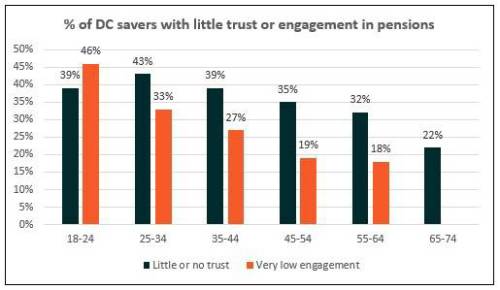

Over a third (36%) of savers answered with a six or less, with just 15% saying they had complete trust in their provider.

Most concerningly the data revealed that younger pension savers trusted the industry least with 43% of 25-34 year olds ranking their trust as a six or less. This drops to under a third (32%) among 55-64 year-olds and just over a fifth (22%) of 65-74 year-olds.

Similarly, the FCA calculated an ‘engagement’ score among adults with at least one DC pension into which they were making contributions. It found that over a quarter of adults (27%) had a very low engagement with a further 24% quantified as ‘low engagement.’

Again, the younger the pension saver, the more worrying the results as without trust and engagement, younger members, who will rely almost entirely on DC savings for their retirement income, aren’t likely to take the action needed to ensure they have adequate retirement savings. Or, worse, opt-out entirely.

Nearly half of those aged 18-24 were said to have very low engagement, remaining at a third (33%) of those 25-34 and, hopefully, well along their pension accumulation journey.

Damon Hopkins, Head of DC Workplace Savings at leading independent consultancy Broadstone, said the figures were evidence of auto-enrolment’s ‘inertia issue’.

“Funnelling millions more employees into DC pensions as soon as they start earning a salary was brilliant in kickstarting a new era of pension saving – but the sector now faces the downside of inertia,” he said.

“The FCA findings suggest a significant proportion of this new cohort struggle to trust the industry and have low engagement. This is a problem because we need these employees to be looking at their pension and working out how much they are likely to need in retirement so they can make the right decisions as early as possible.

“It is also a stark reminder of the variability in the quality of DC provision. Providers and employers must ensure they are at the top of their game when it comes to administrative procedures, delivering robust risk-adjusted returns and engaging with members.

“By doing so we can drive a virtuous circle of positive change within the industry as motivated, trusting pension members derive increasing value for money from their scheme.”

|