Over 50’s are much more likely to want to keep the triple lock promise with almost 6 in 10 (59%) supportive of maintaining it compared to around a third (34%) of those under 50. Women are perhaps more likely to see both sides of the argument, with more than a quarter (27%) saying they don’t know, compared to less than one in ten (9%) men.

Only 16% of respondents supported a move to a less generous ‘double lock’, which would lead to an increase in line with inflation or 2.5%. Even fewer people (14%) supported the idea of finding a compromise to use a lower earnings figure with the furlough impact stripped out.

Almost a quarter (23%) of respondents said they were unsure or uninterested in the decision.

Andrew Tully, technical director at Canada Life comments: “Maintaining the triple lock has long been a manifesto promise. However, no-one could have predicted the 18 months we’ve just experienced with the effect of millions of people being placed on furlough, artificially boosting the earnings data as they return to work.

“The Government has a difficult path to navigate, to ensure the state pension remains affordable in what is a difficult time for the nation’s finances, while also bearing in mind it’s manifesto commitments. It’s important to remember that each 1% rise in state pension costs the taxpayer around £850m a year.

“One option could be to strip out the artificial earnings growth from the data, making it more representative of the real underlying growth in earnings. The state pension would increase by a material amount, hopefully seen as fair in these exceptional circumstances, and making sure manifesto pledges are met.”

New State Pension Factoids

• There are currently 1,684,687 claimants of the new State Pension3

• You need 35 years NI records to qualify for the full new State Pension

• As at April 2019, 7,819,400 working age people had the full 35 years NI record4

• 429,2143 people receive less than £150 a week under the new State Pension

• Transitional arrangements mean anyone with a NI record as at 6th April 2016 could receive more or less than the full rate of the new State Pension with the full 35 years NI record, depending on their individual circumstances

• Your state pension age is based on your birth date. Currently it is age 66 for men and women (it moves to age 67 and then 68 for younger people, although there are no current plans to extend it further)

• 102,091 people in receipt of the new State Pension have moved overseas3

• Top five overseas destinations are Australia (12,544 people), followed by Spain (11,758 people), Ireland (11,442 people), France (10,392 people) and USA (8,525 people)3

• Just under a third (29% or 29,923 people) who have moved abroad have had their new State Pension frozen, meaning it doesn’t increase in line with the current triple lock guarantee3

• The new State Pension has increased by 15.4%5 since April 2016 (from £155.65 a week to £179.60 from April 2021)

• To buy the equivalent new State Pension of £179.60 a week would cost you around £320,0005 using an inflation-linked annuity at today’s rates

• You can elect to stop/start your pension once in payment, but only once. In 2018/19 14,300 people elected to stop received their state pension while a further 1,500 chose to restart6

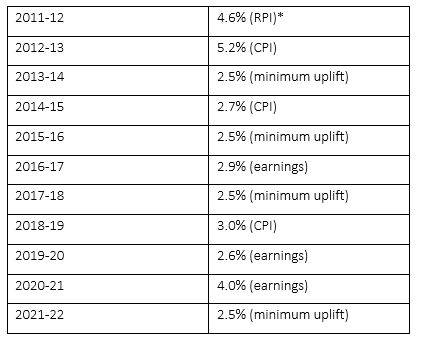

Since 2011/12, the following benchmarks have been used for the annual uprating in line with the triple lock guarantee.

|