The amount that the average employee who is waiting to be auto-enrolled into a company pension scheme is willing to contribute towards their retirement savings has dropped by almost a quarter (24%) over the last year, according to the 2013 Scottish Widows Workplace Pensions Report.

Auto-enrolment has already seen over one million workers successfully enrolled in a workplace pension scheme. However, the study of over 5,000 people showed that among those who are still to be auto-enrolled - around 8.6 million people across the UK - the amount they are willing to save each month has fallen on last year's levels in every salary bracket, bar the highest of £50,000+ per annum. In real terms this amounts to a drop from £67 a month in 2012 to just £51 this year.

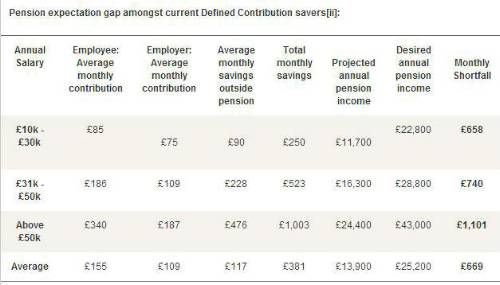

While the amounts are still above the minimum required contributions for automatic enrolment, they remain well below what is needed to match retirement aspirations. Even among those workers already paying into a Defined Contribution workplace pension scheme, a significant shortfall exists between the monthly savings employees (and their employers) are making and their desired income in retirement.

This shortfall between current savings and desired annual income in retirement indicates that despite the positive impact of auto-enrolment, employees are still removed from the reality of retirement.

Awareness of auto-enrolment and contribution levels

Whilst awareness of auto-enrolment has increased from just over a third (39%) in 2012 to almost two thirds (65%) this year, there are still significant gaps in people's knowledge - even among those who have already been auto-enrolled into their workplace pension scheme.

More than a quarter (28%) of those who have been auto-enrolled are unaware of how much they contribute and overall 44% of employees paying into their workplace pension scheme do not know how much their employer is contributing.

Worryingly, awareness remains particularly poor amongst those at whom the scheme is targeted, with one in five (21%) employees on an annual income of under £30,000 still not aware of the changes.

Lynn Graves, Head of Business Development, Corporate Pensions at Scottish Widows, commented: "We cannot ignore the fundamental correlation between poor employee awareness of the scheme and the lack of understanding of the realities of retirement. The alarming fall in the amount that employees are willing to contribute only serves to highlight this."

The value of advice in retirement planning

In light of the uneven awareness of auto-enrolment among the UK workforce, it is clear that there is a need for greater clarity and guidance on retirement options. Over half of employees (57%) think their employer should provide general information about retirement planning, in addition to providing a workplace pension scheme. More than a third (37%) go even further, demanding full financial advice from their employer.

Despite this demand, the report showed that employers are currently one of the last places people turn to for advice. Less than one in five (18%) would go to their employer for advice about pensions, behind the FCA website (20%), pension providers (21%), and friends and family. While a quarter (25%) said they would consult an independent financial adviser, this is down 5% on 2012's figures.

Lynn Graves added: "Auto-enrolment is a vital tool for improving savings behaviours, but it cannot work in isolation to change the nation's attitudes to retirement. The pensions industry, government and employers have to educate the UK workforce about the importance of saving adequately for retirement, and how their workplace pension scheme can help them to be comfortable in old age. Alongside encouraging better employee engagement around workplace pensions, we are committed to achieving greater access to information and guidance, as well as improving transparency around pricing and governance of pension schemes."

|