9.3 million more employees3 have been introduced to saving for their retirement after being automatically enrolled into a workplace pension scheme since 2012. Aviva’s data highlights that thanks to rising contribution rates in 2018, an employee earning the UK average salary of £26,572 per annum4 could add £840 to their savings pot across 2018, up from £600 in 2017.

Rise in contribution levels set to provide retirement savings boost

Since the introduction of auto-enrolment in 2012, minimum workplace pension contributions have been set at 2% of qualifying earnings5, with 1% of that typically coming from the employee. However, from April 2018 the overall minimum level will rise to 5%, with employees typically contributing 3% of earnings, with a 2% contribution required from employers.

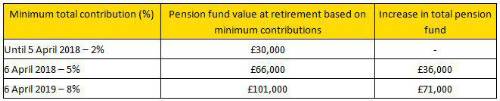

Aside from the expected savings boost in 2018, the changes should also boost the likely pension pot available to savers at retirement. Based on current contribution levels, an employee earning the average UK salary, who began saving into a workplace pension when auto-enrolment started in October 2012, could have a total of £30,000 in their pension fund at retirement. However, with increased minimum contributions of 5% from April onwards, they could benefit from a £36,000 boost, more than doubling their total pension fund to £66,000 when they retire.

And with minimum contributions set to rise again in April 2019 to 8%, the same saver would have £101,000 at retirement, representing an additional £35,000 in their pension pot and more than triple the amount they would have under current contribution levels.

Table 1: Increase in AE pension contributions boosts UK pension pots

Figures are based on assumptions and are not guaranteed. The value of investments can go down as well as up and actual returns could be more or less than shown here

Andy Curran, MD Corporate at Aviva, comments: “Saving via a workplace pension is one of the rare times in life when doing nothing pays. Simply by remaining in their workplace pension scheme, savers can benefit from their employers topping up their savings and receive the added peace of mind that comes from knowing they are contributing to their long-term financial health. While the changes mean employees will also need to increase contributions from their own pay packet, making a small sacrifice now can add up to a big difference when it comes to retirement.

“Auto-enrolment has been an incredible force for good since its introduction in 2012 with more people than ever before now contributing on a monthly basis towards their retirement. It is vital the latest milestone is used as a basis on which to build further momentum around the need for people to save for retirement. If as a society we are to avoid a retirement savings crunch further down the line, we must go further still in the years to come.”

• Savers set for boost as minimum auto-enrolment (AE) pension contributions set to rise from 2% to 5% in April 2018

• Average employee who began saving into a workplace pension when auto-enrolment started could benefit from £36,000 more in their pension fund on retirement as a result

• Average earners could add over £800 to pensions pots across 2018 alone

|