|

|

Barely one in three (36%) unretired over-55s had started their retirement planning during Q2 2016: the lowest percentage since Aviva’s Real Retirement Report began tracking this data two years ago, the latest report reveals. |

Post-EU referendum poll shows 25% of over-55s are concerned about their financial future, up from 19% before the vote

Barely one in three (36%) unretired over-55s had started their retirement planning during Q2 2016: the lowest percentage since Aviva’s Real Retiremement Report began tracking this data two years ago, the latest report reveals.

The Aviva report – which has tracked personal finances among over-55s before, at and during retirement since 2010 – also shows an income dip and rising uncertainty over the economy in Q2 ahead of the UK’s vote on its European Union (EU) membership last month.

Income and savings

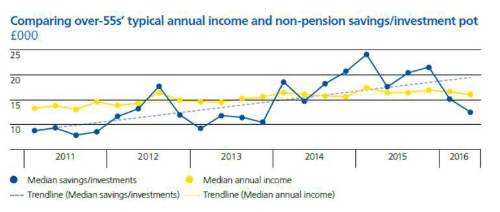

The typical over-55s’ (median) monthly income has risen by 11% over the last three years from £1,212 in Q2 2013 to £1,341 in Q2 2016. However, the latest quarterly figure was down from £1,382 in Q1 and £1,419 in Q4 2015

The dip corresponds with a fall in the percentage of over-55s receiving an income from investments and savings: falling to 25% in Q2 2016, down from 29% a year earlier.

Q2 2016 also saw the highest proportion (12%) of over-55s with no non-pension savings and investments in almost three years. Over-55s’ typical savings and investments pot fell for a second successive quarter to reach £12,590.

However, there was a rise in the percentage of over-55s whose savings included a tax free lump sum from their pension savings. This increased to 16% – the highest level since Aviva started tracking the data in Q2 2014 – and is likely to be influenced by the launch of ‘pension freedoms’ in April 2015.

With incomes and savings squeezed in Q2, monthly spending dropped to £774: the lowest seen since Q3 2014 (£754).

Graph 1: Over-55s’ typical annual income and non-pension savings/investment pots

Planning for retirement

When asked whether they had started planning for retirement, just 36% of unretired over-55s had done so in Q2: the lowest percentage in two years since Aviva began tracking this. While 41% have thought about it but not taken any action, almost one in four (23%) have not even thought about it yet.

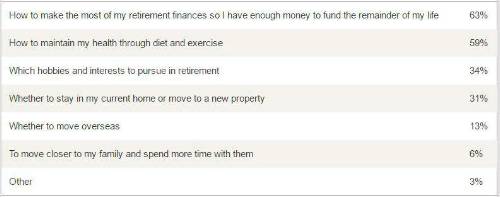

Asked to identify the most important personal choices or decisions they face to ensure a happy retirement, the most common response from unretired over-55s was making the most of their retirement finances so they have enough money to fund the remainder of their life (63%). This was more likely to be singled out as an important personal choice than maintaining their health once they retire (59%) and deciding whether to stay in their current home or move to a new property (31%).

Among those who have already retired in Q2 2016, one in four (25%) said budgeting their money has been the most difficult aspect of their retirement so far, making it their most common concern.

Mirroring over-55s’ general concerns about making their money last in retirement, 13% who are yet to retire feel more anxious about this as a direct result of the ‘pension freedoms’ launched in April 2015, up from 10% a year ago.

There is also uncertainty about their options as a direct result of the new pension rules: just 12% feel their retirement plans might be affected by the extra flexibility offered by the pension freedoms, yet almost a third (32%) don’t know.

Table 1: Unretired over-55s’ most important choices to ensure a happy retirement

Unsecured debt

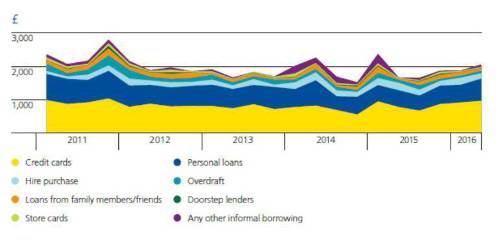

In Q2 2016, the average amount of debt held by over-55s rose for the third successive quarter from £1,662 in Q3 2015 to £2,067.

Comparing back to Q2 2011, the average amount over-55s owe on credit cards has risen from £871 to £967 in Q2 2016, while the average amount owed through hire purchase has risen from £70 to £159.

Graph 2: Average aggregate debt levels among over-55s – Q1 2011 to Q2 2016

Confidence in the UK economy

Aviva’s tracking data shows just 29% of over-55s felt confident in the UK economy during the first half of 2016 (Q1 and Q2) ahead of the referendum on the UK’s European Union (EU) membership, down from 36% in Q4 2015.

There was also growing concern over the threat of rising inflation and the state of the economy, with 28% registering this as a risk to their living standards over the next five years, compared with 22% in Q1 2016.

A separate poll carried out that took place after the ‘Leave’ announcement found that the percentage of over-55s concerned about their future finances rose to one in four (25%), compared to one in five (19%) before the referendum.

Alistair McQueen, Savings and Retirement Manager at Aviva, says: “The UK is entering uncharted territory after the EU referendum, but with relatively few unretired people beyond the age of 55 having started their retirement planning, it is important not to lose sight of long-term savings goals.

“Tracking attitudes to retirement finances since 2010 has helped Aviva understand and support consumers in the wake of the financial crisis, and our findings offer important lessons for times of uncertainty. Deciding how to make the most of our finances so we have enough money to last in retirement, and then budgeting effectively, are consistently picked out as the most important challenges we face in later life. It means the importance of saving for the future remains one of life’s certainties.

“Changing social, political and demographic factors mean that the outlook for retirement finances in the UK is constantly evolving. We will continue to monitor developments closely in order to understand and support consumers’ needs.”

To download the full report click here

|

|

|

|

| Take the lead client-facing projects ... | ||

| Various locations - Negotiable | ||

| Choose Life! Choose a major global co... | ||

| Various locations - Negotiable | ||

| Actuarial skillset? Apply now for Snr... | ||

| South East / hybrid with travel requirements - Negotiable | ||

| Financial Risk Leader - ALM Oversight | ||

| Flex / hybrid - Negotiable | ||

| Be the very model of a modern Capital... | ||

| London - Negotiable | ||

| Pensions Actuary seeking a high-impac... | ||

| London or Scotland / hybrid 3dpw office-based - Negotiable | ||

| Great opportunity for Pensions Actuar... | ||

| London or Scotland / hybrid 3dpw office-based - Negotiable | ||

| Responsible Investing Manager - Clima... | ||

| London/Hybrid - Negotiable | ||

| Quant Strategist | ||

| London/Hybrid - Negotiable | ||

| Multiple remote longevity contracts | ||

| Fully remote - Negotiable | ||

| Multiple remote inflation hedging con... | ||

| Fully remote - Negotiable | ||

| Play a vital role in shaping a new He... | ||

| London or Scotland / hybrid 50/50 - Negotiable | ||

| Support the Longevity team of a globa... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Delve into financial risk within a ma... | ||

| Wales / South West / hybrid 1dpw office-based - Negotiable | ||

| Project-based Life Pricing Actuarial ... | ||

| South West / hybrid 2 dpw office-based - Negotiable | ||

| Pricing Actuary | ||

| London - £120,000 Per Annum | ||

| Develop your career in motor pricing | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Experience real career growth in home... | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Be at the cutting edge of technical p... | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Use your passion for innovation and t... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd