Retirees keen to secure a guaranteed income for life by investing in an annuity are often worried about whether some of their money will be wasted if they die too soon.

Sales of annuities are being boosted by higher returns but some retirees are still wary due to concerns that they may invest thousands of pounds in an annuity that is lost if they succumb to an early death.

“While it’s natural for people to worry about losing their pension money if they die prematurely, there are a range of options to make sure this can’t happen,” said Stephen Lowe, group communications director at retirement specialist Just Group.

“These options do come with a cost in terms of a reduced income, but the reduction can be quite modest although that will depend on how much you want to protect and your age.”

Annuities remain the only way to turn a pension pot into a secure, regular, guaranteed retirement income paid to you for as long you live. One option available to buyers is to add a feature called ‘value protection’ which can ensure up to 100% of the original cost of the annuity is paid out to beneficiaries minus the income already paid.

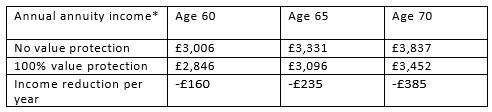

“Based on current rates, a 60-year-old using a £50,000 pension pot to buy an annuity could receive £3,006 a year guaranteed income for life with no protection, or £2,846 a year income with 100% value protection,” said Stephen Lowe.

*Based on £50k purchase price, single-life, paid monthly in advance, no escalation - rates on 03/01/24

“The cost of the protection is therefore £160 a year or £3 a week which is about the same as a high street coffee. If the annuitant was unfortunate enough to get hit by the proverbial bus after five years then £35,770 would be paid out to beneficiaries which is calculated as the original annuity purchase cost of £50,000 minus the five years of income already paid of £14,230.

“Under current tax rules the payout is usually free from Inheritance Tax and the beneficiary pays no Income Tax if the annuitant died before age 75.”

Value protection is one of several options that ensure annuity money continues to be paid out after the death of the annuitant.

“A joint-life annuity will continue paying income to a spouse or partner until the second death and so is a useful way for retirees to ensure a continuing flow of income to a partner without much retirement provision of their own,” said Stephen Lowe.

“Guaranteed terms are another popular option that ensure that in the event of early death of the annuitant, the payments will continue to be made to a designated beneficiary for the remainder of a term. It’s common for people to select five or 10-year terms, but it’s possible for the term to be as long as 30-years.”

He said that due to the range of annuity options, it is important that buyers seek professional help from an independent annuity broker or regulated financial adviser.

“They will help you ‘shape’ your annuity so that you get the right options for your circumstances in terms of capital and inflation-protection, and then help you shop around for the most competitive rate among providers, taking into account your health history and lifestyle details which can make a huge difference.

“The standard rates published online or in newspapers are really just a starting point and most annuity buyers will receive higher income by taking the time to properly shop around for the best deal.”

Annuity buying tips:

• www.moneyhelper.org.uk – the government’s money and pensions guidance service offers access to free, independent and impartial guidance service Pension Wise and also has a useful online tool allowing quick comparisons of annuity rates and options.

• Employ an expert – an annuity broker or regulated adviser will work with you to better understand your goals, to choose the right options and shop around for the best deal.

• Full disclosure – providing details of your lifestyle and medical history is the only way to get a personalised annuity rate based on your unique situation.

• Don’t settle for less – seek out the highest offer because small differences in annuity offers can add up to large amounts over a long retirement.

|