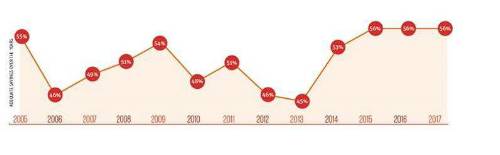

Since auto-enrolment was introduced five years ago, the number of adequate savers in the UK has risen from 46% to 56%, according to Scottish Widows research. One in five adults in the UK (18%) is still not saving anything into a pension and 70% of under 30s are not saving adequately.

Scottish Widows Adequate Savings Index

Pete Glancy, Head of Policy Development at Scottish Widows, said: “There is no doubt auto-enrolment has been a success in kick-starting the savings habit for millions – but it is not a silver bullet. Auto-enrolment may well be lulling people into a false sense of security that they are putting away enough for a comfortable retirement. For many, particularly those only making the minimum contribution, that is simply not the case given retirement is looking more expensive, and longer, than ever. We want the Government to take the opportunity with the auto-enrolment review to make some rule changes to help people save more.”

Recommended changes are:

1. Minimum contribution level lulling people into false sense of security - increase to 12%

While minimum pension contributions will rise to 8% in April 2019, from 2% now, this is not enough to provide an adequate income in retirement for most. Scottish Widows has calculated that 12% of salary is an adequate savings level - the Government should make this the new minimum contribution level into a workplace pension by 2020.

2. Make pensions inclusive for low earners

Britons can only start to benefit from auto-enrolment when they are earning over £10,000 and this unfair barrier needs to be removed to ensure low earners, those working part-time or in multiple jobs can benefit from auto-enrolment. Scottish Widows believes the industry should go further and that every worker should benefit from auto-enrolment – even those who can’t afford to contribute. The Government and industry needs to explore how these people can still receive an employer contribution, while not discouraging others from making personal contributions.

3. Ditch qualifying earnings

Auto-enrolment needs to be simplified with contributions paid on every pound earned, rather than qualifying earnings which can see the first £5,876 of salary discounted when calculating contributions.

*Scottish Widows suggests a combined 12% employer and employee contribution as an adequate level of saving.

Stephen Coates, Principal, JLT Benefit Solutions, said: “While saving something is better than saving nothing, an 8% contribution is a long way from delivering fully-funded retirements. The next challenge is to move the conversation from the policy-makers, scheme providers and the employers, to the policyholders themselves. They need to be actively involved in determining and reviewing their savings levels, monitoring charges and investment performance, as well as making the right choices at retirement. The first hike in contributions provides a great opportunity to further prompt savers to take greater responsibility towards their retirement.”

|