Urgent action needs to be taken to address the UK’s gender pension gap, as new research of more than 4.5 million savers in the UK shows that it has barely changed since 2020, and in some age groups and sectors has deteriorated further.

Women are left with smaller pension pots at every stage of their career, with the situation worsening significantly as they approach retirement. The research, which analyses data from more than 4.5 million members across L&G’s defined contribution (DC) pension scheme clients, shows that women are always at a financial disadvantage, even at the start of their careers.

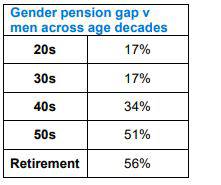

The initial gap of 16% widens as women reach their forties, accelerating to 31% as the impact of career breaks and unequal caring responsibilities begin to take effect. By the time people can take their tax-free cash at 55, the gap is over 50% and deteriorates further to 55% by retirement.

This new data for 2021 shows the gender pensions gap has decreased marginally across age ranges, but by only one percentage point for the start and end of women’s careers. On the current trajectory, women will still be retiring with vastly smaller pension pot sizes than men for many decades to come.

Retirement prospects still diverge starkly

L&G also analysed the size of the pension pots of more than 50,000 Britons who retired in 2021 and the picture remains just as stark as those yet to retire. On average, the size of a man’s pension pot at the point of retirement was £26,000 compared with just £12,000 for a woman. Whilst retirees are likely to have more than one pension pot from different employers, the gap is expected to be broadly similar for all pots.

Why there is an issue in the first place

There are many reasons identified for the gap, including the fact that women are still paid less and are less likely to be in senior leadership positions, resulting in lower pay and lower pension contributions. They are more likely to take career breaks for childcare or as an unpaid carer and are more likely to work part time or reduced hours, as well as self-identifying as having lower fiscal confidence.

The high cost of childcare in the UK* is a barrier to women returning to work after maternity leave, or returning full time, and the means test on benefits can be a driver for capping hours, particularly in certain industries. In addition, 900,000 women in the UK retire early each year due to Menopause, meaning women are leaving the workforce at the exact time when their earning potential is likely at its highest.

Reflecting on the challenges facing women who are saving for their retirement, Katharine Photiou, Commercial Director of Workplace Savings at Legal & General said: “There are many factors that have led us to this point but very few solutions offered. It’s time women stop being penalised for things outside of their control, like the high cost of childcare, or being paid less than their male counterparts.

“We know that women feel significantly less confident, and are more likely to struggle on knowing where to start, when it comes to making financial decisions. Industry and government must therefore work together to ensure education and engagement around savings and investments increase. For example, too few know about the flexibility that couples have in being able to contribute to their partners’ pension while they are on parental leave. This is something that can significantly reduce a women’s pension shortfall.”

L&G actively involved in exploring solutions with government and industry

Like the gender pay gap, the pensions gap is a structural and societal problem that will take time to solve. L&G recognises that urgent action needs to be taken now and is calling for all companies and DC pension providers to publicly disclose their own gender pensions gap, so that all stakeholders can understand the issue and work to fix it.

To do so, L&G has reviewed its own gender pension gap and will monitor it annually to ensure it is making progress, by reviewing internal support, processes and policies to make changes such as better support for menopause and a review of paternity and shared parental leave. Current analysis shows that there is a 60% gender pension gap for L&G retirees at the point of retirement with an average gap of 32% for current savers.

In addition to disclosing its own gender pension gap, L&G is committed to raising the profile of the gender pension gap across the companies it invests in and will continue collating data in order to include it in its stewardship activities going forward, as well as working with regulators, trade bodies and other providers on longer term solutions.

Going further, L&G has created a working group with 14 of its largest clients with 535,000 members and assets of over £7 billion, to help them tackle inequality in their own pension schemes by the end of 2022 and plans to expand this group further in 2023. In addition to promoting greater collaboration between schemes and providers, L&G has also committed to equipping all defined contribution clients and their underlying 4.5 million members with the tools they need to help address the gender pensions gap.

In terms of regulatory reform, L&G submitted a number of recommendations to the Work & Pensions Select Committee in January 2022 as part of the Pension Freedoms Consultation, including:

• Reducing the eligibility age for auto-enrolment to 18 and basing auto-enrolment pension contributions on the first £1 of earnings by removing the £10,000 eligibility trigger.

• Allowing greater flexibility for couples to pay into each other’s pensions, as well as considering an increasing the maximum allowed.

• Encouraging pay and job progression for part-time workers and examine whether eligibility to means-tested benefits acts as a barrier to women seeking to increase their income and savings ability.

• Promoting the inclusion of pensions in divorce proceedings.

• Prioritising the provision of suitable and affordable childcare to encourage women to work more hours.

Commenting on the need for cross-industry solutions to the gender pension gap, Stuart Murphy, Co-Head of Defined Contribution at Legal & General said: “These figures demonstrate the glacial pace of change on the gender pension gap, as well as the need for greater cross-industry collaboration between government, employers, pension fund providers and members to address the scale of the challenge.

“In our view encouraging full disclosure to highlight the scale of the issue is an important starting point. We are calling for full disclosure from companies and DC pensions providers to publicly share their gender pension gap so that we can better identify and fix this problem.

“We are also making a call for regulators and law makers to look at reform; including dropping the minimum age of auto-enrolment, abolishing the auto-enrolment minimum salary threshold and provide further support to help families with childcare costs.”

|