Conventional wisdom is that the US dollar has a strong influence on commodity prices. The explanation for this relationship is that since commodities are priced in dollar terms, then commodity prices must move lower when the dollar strengthens to reflect its increased purchasing power.

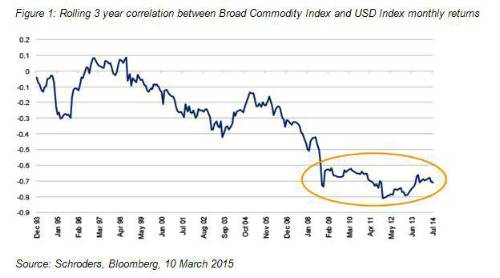

After the 2008 global financial crisis there has indeed been a very strong inverse relationship between commodities and the US dollar, as shown by the correlation chart in Figure 1 below.

However, this has not always been the case. Prior to the financial crisis, the correlation was much less obvious. For example, during the boom years of the 1990s there was almost no relationship between the US dollar and commodity prices. Then, in the recovery after the dotcom bubble bursting from 2003-2006, the relationship weakened again.

We therefore reject the gross simplification that all you need to know to have a view on commodities is the direction of the dollar. It does, however, help if you can identify which type of dollar environment you are in.

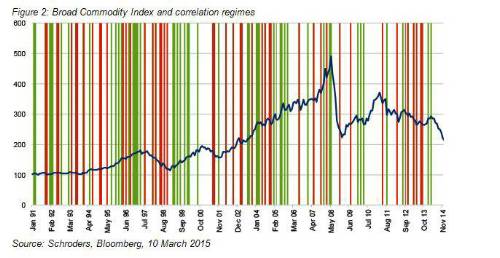

Looking at the period from 1990 to 2015, 61% of the time there was a negative correlation between US dollar and commodities, and 39% a positive correlation. This 39% can be further subdivided into 23% for both commodities and US dollar rising, and 16% both US dollar and commodities falling. Figure 2 highlights in green those periods where we have both rising US dollar and commodities; the periods of both falling are highlighted in red.

Generally speaking, during Federal Reserve rate-hiking cycles we see a positive correlation regime where both the dollar and commodities rose together. The greatest concentration of green observations occurs in these periods: June 1996 – March 1997, March 1999 – January 2000 and June 2003 – December 2005. These were periods of both rising interest rates and stronger growth.

We are approaching a tightening cycle in the US and this is likely to result in a continued strengthening of the dollar. If this is associated with continued positive economic growth then both the US dollar and commodities can go up. In the event that tightening is a policy mistake, or it exerts so much pressure on emerging market economies that we enter an emerging market crisis phase (slowing growth and exacerbating the demand for the US dollar) then commodities are likely to suffer.

|