That’s according to the latest benchmark AA British Insurance Premium Index, which has shown the average Shoparound* quote (using both direct/broker and comparison site prices) fell by 1% or £5.58, to £530.47.

That compares with a rise of just 0.2% over the last quarter of 2014, and a rise of 1.2% over the three months ending 30 September. Over 12 months, premiums have fallen by 5.8%.

Janet Connor, managing director of AA Insurance, says that the first quarter often sees insurers offering price reductions to build market share at a time when, with the new motor registrations, more policies are sold than at other times.

However she says the brakes are now coming and premiums are starting to rise and will continue to do so over the rest of 2015:

This is already beginning to happen among older drivers but she predicts: “the rate of increase isn’t going to be turbo-charged.

“We’re starting to see insurers quoting higher prices and I think that’s the beginning of a trend, but market remains very competitive.”

Janet Connor points out that for many insurers, the cost of claims is greater than premium income which means that present prices are simply unsustainable.

Ms Connor says she is hopeful that new medical reporting accreditation for whiplash injury assessment will help to curb the out-of-control claims that are now leading insurers to increase premiums.

“I hope this will put off those looking for an easy cash win but not discourage those with a genuine injury.

Recent research by the AA showed that 11% of motorists** say they see nothing wrong in making a claim for compensation in the event of a no-fault collision even if no injury is suffered. Ms Connor says this culture is encouraged by cold-calls from claims management firms.

The AA has called on the government to take firm action against such firms as it emerged from an AA-Populus study** that two-thirds (63%) of AA members have been cold-called by firms encouraging them to make a whiplash injury claim in the past year, a third of them (36%) more than 10 times.

“Despite the premium falls over the past couple of years, the cost of cover remains higher in the UK than in most other European countries***, thanks to the claims culture in the UK,” Janet Connor points out. “While the number of crashes on Britain’s roads has fallen, the number of injury claims has risen.

“It’s time consumers understood the connection between premiums and making fraudulent claims. Car insurance is there to protect drivers in the event of a crash, not as an opportunity to cash in. Insurance isn’t a savings account.

“My greatest fear is that if insurance fraud such as whiplash injury claims isn’t brought under control and quickly, we will see a repeat of the spiralling premiums of 2010 and 2011 when the cost of the average policy rose by over 40% in just 12 months.”

Shoparound summary, all channels *

(average of five lowest quotes for each ‘customer’ in basket of risks)

Winners and losers – by age

Winners and losers – by age

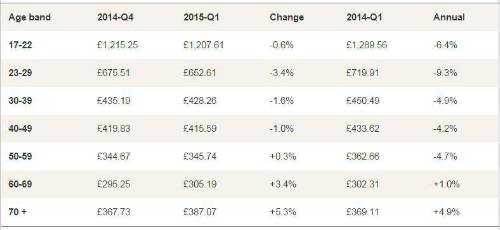

Overall, it’s younger drivers who have benefited this quarter with premium falls recorded for all age brackets up to age 49. The 23-29 age group has seen the biggest fall, 3.4%, to an average quoted premium of £652.61. The youngest drivers nevertheless benefited from a fall in average quoted premium of 0.6% to £1,207.61, compared with a rise of just 45p during the previous quarter. Those aged 70 and over suffered a sharp premium rise, with a jump of 5.3% to £387.07

Shoparound by age

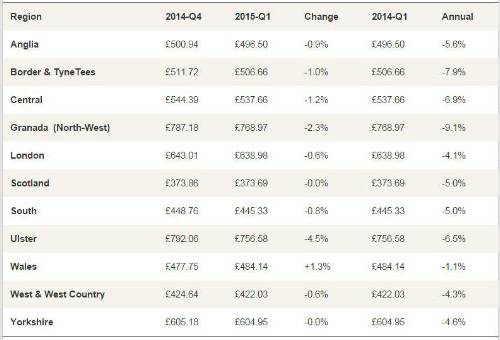

Winners and losers – by region The only region to see an average premium increase is Wales, with an average premium of £484.14, up by about £6 or 1.3%. The biggest fall was in Northern Ireland where premiums fell by 4.5% to £756.58, swapping places with the North-West which is now the most costly region to insure a car with an average quoted premium of £768.97 – down 1.2%. Scotland continues to be cheapest region in the UK for car premiums and has seen a fall in premium of just 17p.

Shoparound by region

|