interactive investor calculates that workers wanting to retire at age 57 could need an extra £38,000 in savings to bridge the gap until they can access their private pension pot at 58 to ensure a comfortable retirement if the State Pension age is hiked sooner than billed.

Under the current law, the State Pension age will rise from 66 to 67 by 2028, and then to 68 between 2044 and 2046. However, the government is considering making the change even earlier, with some reports citing a rise in state pension age to 68 by 2034.

The government’s intention is that the normal minimum pension age for private pensions should be ten years below state pension age. From 2028, the government plans to increase the normal minimum pension age in lockstep with the state pension, keeping it 10 years earlier, although it won’t automatically rise at the same time.

Changing the private pension minimum age to 58 from 2034 only gives people eleven years to adjust their plans or invest on the basis of the new rules.

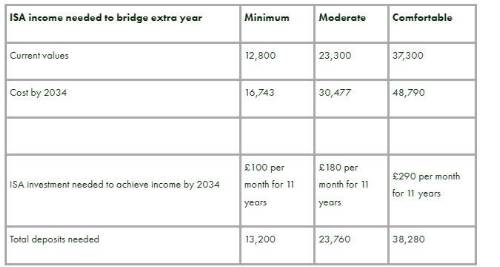

The PLSA retirement living standards estimate that a single person needs around £12,800 to achieve the minimum living standard, £23,300 per year for a moderate retirement. In contrast, you’ll need around £37,300 for a comfortable retirement.

But those figures are net of tax, meaning you could need more if that income is coming from a taxable source, like a pension or part-time job. Also, they do not factor in inflation.

Assuming inflation of 5.2% in 2023 and 2% thereafter, interactive investor calculates that the cost for a minimum, moderate and comfortable rises to £16,743, £30,477 and £48,790, respectively.

This means that workers who still want to retire at 57 could be required to save an extra £38,280, before investment growth, for comfortable living standard to bridge the gap until they can access their private pension pot at 58. That equates to investing £290 a month for 11 years, assuming investment growth of 5% and fees of 0.5%.

For a moderate standard of living, the £23,760, or £180 per week, would be required under the same assumptions (investment growth of 5% and fees of 0.5%), falling to £13,200 or £100 a month, to achieve the minimum living standard.

Cost of covering one year lost pension income

Assumptions: investment growth 5%, 0.5% fees, minimum, moderate and comfortable retirement per PLSA retirement living standards, inflation 5.2% then 2% from 2024 onwards.

These scenarios should not be taken as advice.

Alice Guy, Personal Finance Editor, interactive investor, says: “The increasing private pension age will make it significantly harder to retire early. People make retirement plans decades in advance and rely on the current rules for their planning. Changing your retirement plans isn’t always easy – people set their heart on a certain retirement date and press on, perhaps in a tiring role or with health problems, with that date in mind.

“Our calculations show that workers who still want to retire comfortably at 57 would need to save an extra £38,280, or £290 a month, to bridge the gap until they can access their private pension pot at 58, assuming investment growth of 5% and fees of 0.5%. That’s a huge amount for someone to find from their budget, at a time when spiralling costs are hitting household hard.

“The change will be a blow to people who need to retire early or cut their hours due to ill-health or family caring responsibilities. ii’s Great British Retirement Survey 2022 revealed that only one in three 55-to-65-year-olds say they work full time – one in three have cut hours due to health issues or care responsibilities. Some physical jobs are difficult for older workers, and greater pension flexibility allows them to choose to take a part-time role, alongside drawing a modest pension income.

“The changes will also affect us even if we’re not aiming for early retirement. Many of us plan to withdraw a tax-free lump sum from our pension and have ear-marked it for essential costs like clearing our mortgage or paying for university costs. There’s a risk that many people will struggle financially and find it takes longer to clear debts. For example, if you had a £200,000 pension pot at 55 and planned to withdraw £50,000 to pay off your mortgage, you could end up paying around £7,000 more interest over the three years between 55 to 58, assuming a 5% interest rate.

“There’s a danger that continual tinkering with the pension system and pushing back when we can dip into our pensions will put people off pension saving, at a time when we need to encourage people to invest more to build an adequate retirement income.”

Myron Jobson, Senior Personal Finance Analyst, interactive investor, says: “Unlike the state pension age, there isn’t a universal answer to the question of what constitute the normal minimum retirement age. The working lives in some professions can be short and pushing back the private pension age sooner than expected means that many savers will need to act now to account for the lost year of private pension access - which, by our calculations, amount to over £13,000 for a no-frills standard of living at retirement.

“Many savers will be forced to rethink how their assets are spread between their pensions, ISAs and other savings. Homeowners with an interest-only mortgage deal that matures before they can access their private pension would need to ensure they have enough cash to pay off the original amount borrowed from their lender and to make up for the lost year of private pension access.

“There is no escaping the fact that Britons will have to do most of the heavy lifting to ensure a healthy income at retirement. But planning for retirement is difficult when the pension regime is up in the air. Savers have grown tired of tearing up finely tuned retirements plans in response to changes to the pensions regime.”

|