The cost-of-living crisis has been identified as the main barrier for two fifths (41%) of over 50’s that might prevent them from securing the income they think they’ll need in retirement, according to research from Standard Life, part of Phoenix Group. A further one in ten with a DC pension or SIPP (11%) say they are more likely to purchase an annuity with their pension pot in light of the cost-of-living crisis, and one in ten already are, according to FCA data.

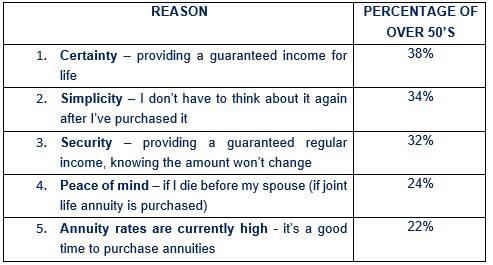

According to the research, which explores how the high cost of living over the last year has driven changes in how people plan to use their retirement savings, over a third (38%) cite certainty that an income would be guaranteed for life as a key reason why there are more likely to purchase an annuity in the current climate. Others cite simplicity (34%) as well as security in the knowledge that the amount of income won’t change (32%).

Top 5 reasons among the over 50’s who say that are more likely to purchase an annuity in response to the cost-of-living crisis:

Other barriers cited by over 50’s that might prevent them from securing the income they think they’ll need in retirement include potential changes to the state pension (24%), tax rises (17%), performance of the stock market (15%) and retiring early due to ill-health (13%), and not seeking out advice (8%). This comes as almost half (48%) of over 50’s expect their own financial situation to get worse over the course of the year. Just 16% expect their own personal finances to get better.

Pete Cowell, Head of Annuities – Individual Retirement at Standard Life, commented: “In a cost-of-living crisis, in which every penny counts, annuities can offer what many people are looking for in retirement – certainty and security, knowing that their money will last as long as they do. The income security benefits of annuities are well-known, however with the improvement in annuity rates, which have seen a total increase of 48% since the start of 2022, they also offer a better level of income.

Pete continued: “While annuities can be purchased standalone, it’s also important to bear in mind that they can also work well in combination with other retirement income solutions, such as drawdown. People may opt to buy an annuity with a portion of their savings and invest the remainder, which gives people certainty about their ability to meet fixed costs. They can take some risk on the money that remains invested while maintaining flexibility over when and how they access it. Alternatively, buying an annuity at different stages of retirement allows people to benefit from annuity rates, which increase with age. Whatever the course of action, a mix and match approach suited to individual circumstances can often be an ideal way to get the best of both worlds – security in the current economic climate, but also flexibility for the future.”

|