|

|

Shifting economic conditions and pension surpluses could spur the revival of defined benefit (DB) pension accrual.DB pension accrual was once commonplace in the UK private sector and a fundamental component of an employee’s benefit package. However, a combination of low interest rates and rising life expectancies put paid to DB as the primary form of retirement provision during the 2000s, with companies almost universally switching to lower risk (and lower cost) defined contribution (DC) pension arrangements for current employees. |

By Lewys Curteis, Principal and Senior Consultant - Corporate Actuary at Barnett Waddingham While the companies hampered by years of deficit reduction contributions will instinctively be in no hurry to revive DB pensions, the reappearance of DB scheme surpluses and the altered economic environment could make the case for re-considering DB pension accrual in some form as an attractive employee benefit for certain companies. This is particularly the case for those companies that are considering the potential value that could be obtained from running on an existing DB scheme, where existing and future surpluses could be used to fund future pension accrual. Companies considering closing their DB schemes may also think twice. Below, we have outlined some of the key reasons why DB pension accrual could again be a feasible option for certain companies.

Competitve DB accrual costs

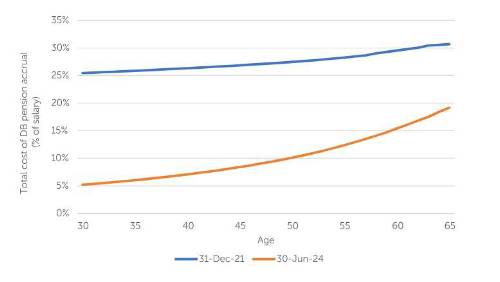

Calculation details for chart

Assumptions: Our analysis suggests that the expected cost of DB pension accrual has reduced by 40%-80% (varying by age) over the period since the start of 2022. If we assume members contribute the auto-enrolment minimum rate of 5%, based on the benefits modelled this would suggest a current contribution rate for the employer of 1% for a 30-year-old, increasing to 15% for a 65-year-old, and an overall average employer contribution rate of 6%. This compares to the current minimum auto-enrolment contribution rate of 3%. These are not unreasonable costs for a generous DB pension benefit, particularly if some of this cost can be borne from an existing DB surplus or if the member contribution rate is set at a higher level. Of course, DB pension accrual costs are sensitive to changes in financial and demographic factors, and a reversal in bond yields would push up the expected cost of DB pension accrual again. This can be mitigated by appropriate scheme design and setting clear parameters for risk. In the case where an existing DB scheme surplus is used to fund DB pension accrual costs, if the surplus is sufficiently large relative to accrual costs, absorbing volatility in the contribution rate may well be manageable and a price worth paying for providing an attractive employee benefit at what is currently a competitive rate.

Risk management is much improved The lack of liability hedging in the early 2000s meant schemes were woefully underprepared for the collapse in yields after the global financial crisis. DB pension risk management has undoubtedly improved because of this, with liability hedging strategies in particular significantly more advanced than they were a couple of decades ago. Solutions are also emerging in the capital-backed funding market to provide schemes with a higher degree of certainty regarding growth asset performance – providing mitigation for companies that would prefer not to bear this risk. The evolution in risk management strategies should provide a higher degree of confidence that asset strategies will keep pace with liabilities that are built up from new DB accrual, and materially reduce the chance of significant deficits emerging in the same way as they did after the global financial crisis. Re-opening to accrual could also help with the management of legacy liabilities, where scheme closure has led to funding challenges as a result of the shortened time horizon and cashflow pressures. Increasing the investment time horizon and reducing cashflow pressures could potentially supporting a degree of re-risking and the generation of additional surplus. The final point to note is the significant strides we have seen in administration practices due to advances in technology over the last couple of decades. The days of paper records and manual calculations have now passed, significantly reducing the risk of calculation errors, benefit uncertainty and suboptimal member experience.

Is there a DC crisis on the horizon? The Pensions and Lifetime Savings Association's (PLSA) analysis suggests that only around 50% of the UK’s population are projected to meet the retirement income targets set by the 2005 Pensions Commission. This falls to 35% for those individuals with DC savings but no DB entitlement . "Unless this pension shortfall is addressed in the coming years by significant increases in DC contribution rates, it is very likely that we are slowly walking into a retirement crisis, with many employees soon facing the choice of retiring with insufficient savings for a comfortable retirement or not retiring at all." The appreciation of DB will only increase as a result of this and offering this benefit in some form will help to set an employer apart from its competitors.

Workforce planning This is an issue that could be addressed by offering some form of DB benefit, and once again using this as a valuable tool for recruiting and retaining the best employees. This may well be a natural consequence of the looming DC retirement crisis but could already be a consideration for industries where there are competitive labour pressures, competition with other companies offering DB, or where employees tend to remain in employment for a longer period. DB will also support companies with workforce planning issues at the other end of the career path, by ensuring that older employees are able to retire when they want to, rather than remaining in employment due to insufficient retirement savings.

What would DB look like in today's world? Scheme design will be particularly important to ensure employees receive a retirement benefit that is understood and valued, while not exposing the company to significant risk.

Some of the potential options include:

A DB benefit that tops up the State Pension with the aim of providing employees with a retirement income in line with that required to support a minimum/moderate living standard in retirement. This could be provided alongside a supplementary DC scheme for employees that want to target a higher level of income.

A DB benefit that comes into payment at a defined older age (e.g. age 80), in combination with a DC scheme to cover the earlier years of retirement. This would provide a fixed period in retirement for managing DC savings (addressing one of the key challenges of managing one’s own longevity risk) and provide a regular income at a time when managing a DC pension could become more challenging. Cash balance – i.e. members receive a cash benefit at retirement that is defined by reference to salary and service.

This is not merely theoretical - IBM have recently re-opened their DB plan in the USA on a cash balance basis to utilise the large surplus that had built up in respect of past service benefits.

While the regulatory landscape is different in the US, this is a clear example of a large, important employer dipping its toes back in the DB pension market. Could this encourage others to follow suit? We are already starting to see signs of this happening. We have several clients that have recently delayed decisions to close their schemes due to significantly improved funding positions – it would not be a huge leap further for a scheme to reopen to new accrual. |

|

|

|

| Take the lead client-facing projects ... | ||

| Various locations - Negotiable | ||

| Choose Life! Choose a major global co... | ||

| Various locations - Negotiable | ||

| Actuarial skillset? Apply now for Snr... | ||

| South East / hybrid with travel requirements - Negotiable | ||

| Financial Risk Leader - ALM Oversight | ||

| Flex / hybrid - Negotiable | ||

| Be the very model of a modern Capital... | ||

| London - Negotiable | ||

| Pensions Actuary seeking a high-impac... | ||

| London or Scotland / hybrid 3dpw office-based - Negotiable | ||

| Great opportunity for Pensions Actuar... | ||

| London or Scotland / hybrid 3dpw office-based - Negotiable | ||

| Responsible Investing Manager - Clima... | ||

| London/Hybrid - Negotiable | ||

| Quant Strategist | ||

| London/Hybrid - Negotiable | ||

| Multiple remote longevity contracts | ||

| Fully remote - Negotiable | ||

| Multiple remote inflation hedging con... | ||

| Fully remote - Negotiable | ||

| Play a vital role in shaping a new He... | ||

| London or Scotland / hybrid 50/50 - Negotiable | ||

| Support the Longevity team of a globa... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Delve into financial risk within a ma... | ||

| Wales / South West / hybrid 1dpw office-based - Negotiable | ||

| Project-based Life Pricing Actuarial ... | ||

| South West / hybrid 2 dpw office-based - Negotiable | ||

| Pricing Actuary | ||

| London - £120,000 Per Annum | ||

| Develop your career in motor pricing | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Experience real career growth in home... | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Be at the cutting edge of technical p... | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Use your passion for innovation and t... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd