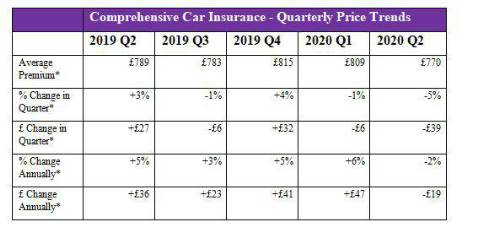

The average cost of car insurance is now £770, following a £19 (2%) decrease over the past year, according to the longest established and most comprehensive car insurance price index in the UK, which is based on price data compiled from almost six million customer quotes per quarter.

Graham Wright, UK Lead of P&C Personal Lines Pricing at Willis Towers Watson, commented: “The sudden drop in traffic during lockdown and fall in accidents and claims inevitably put temporary downward pressure on the cost of premiums. However, a forensic analysis of the complex changes in customer quoting patterns in the last quarter reveals the impact of the pandemic on market dynamics was about more than just price.”

The in-depth research looked beyond price to both changes in the mix of types of people quoting – for example less young driver quotes were conducted because fewer newly qualified young drivers were coming onto the roads – and to changes in the type of quote that customers were requesting. The analysis noted that, for example, customers who might typically be 10,000 mile-per-year drivers were now seeking quotes at lower mileage levels.

The research also investigated changes in the mix of insurers quoting and, with some providers ceasing to quote for different periods, this further affected the composition of insurers making up the top five average price. According to Willis Towers Watson, all of this reveals that whilst insurers took pricing action over the quarter, not all of the surface level changes in market price are necessarily exactly as they seem.

Example trends from April analysis

Research by Willis Towers Watson of individual car insurance market segments revealed significant insights concerning the wider market, in particular during the most restrictive period of lockdown in April, including:

• Dramatic fall in young drivers – A sharp reduction in new vehicle purchases during lockdown, furloughing of many young customers, and postponement of driving tests saw a drop in new drivers on the roads. In contrast, quotes for “mainstream” vehicles worth less than £18,000, owned for at least a year and for which the potential policyholder had multiple years of no claims bonus, made up 44% of April’s quote exposure. This same segment of quotes represented only 33% in March. The average of the top five quoted premiums for this business segment was £718 in April, down from £734 in March.

• More cars kept at home during the day – Quote volume for this segment –relating to drivers who have held a licence for at least a year, requesting cover for annual mileage of between 4,000 and 6,000 miles and whose vehicle is kept at home during the day - increased from 23% of the total in March to 26% in April.

• Fewer drivers in new cars – One segment of the market that saw its quote representation fall dramatically between March and April was recently purchased, previously owned vehicles, at least a year old, having an engine size of 1.5L or less, for policyholders having no NCD entitlement. This segment went from representing 15% of the total quotes in March to only 9% in April.

Graham Wright said: “This analysis showed that some of the initial market-level price reductions seen post-lockdown were driven more by the significant shifts in customer quoting patterns. And although quoting patterns reverted towards more normal trends towards the end of the quarter, the research has only highlighted further the need for insurers and intermediaries to look closely at how they price for the so-called new normal.”

“Looking further ahead, as we emerge from lockdown and roads become busier, insurers are attempting to predict claims and adjust prices before the full impact of Covid-19 on both medium and long-term frequency and severity trends is known. Whilst there are trends that simultaneously point to both higher and lower levels of driving than before – such as less use of public transport balanced with more working at home - a further headache is estimating the impact on severity from broken repair supply chains, more cyclists on the roads and recessionary trends. These are just some of the moving parts that will make pricing risk correctly even harder than before the COVID-19 crisis – meanwhile all of the challenges from before such as whiplash reforms, inflation and Brexit remain.”

|