|

|

As the Government seeks to reinvigorate the UK and stimulate growth, a new Pensions and Lifetime Savings Association (PLSA) report makes practical recommendations to create the necessary investment conditions for pension schemes to allocate a greater portion of the nation’s retirement savings to promising UK growth areas. |

Since early 2023 there has been considerable debate about whether and how pension funds can be supported to allocate more to emerging – but higher risk – sectors that could drive UK economic growth. The PLSA set out six ways to achieve this in its report on Pensions & Growth last year (see background below). Today’s report follows up on how the UK needs to ensure there is a pipeline of investible opportunities.

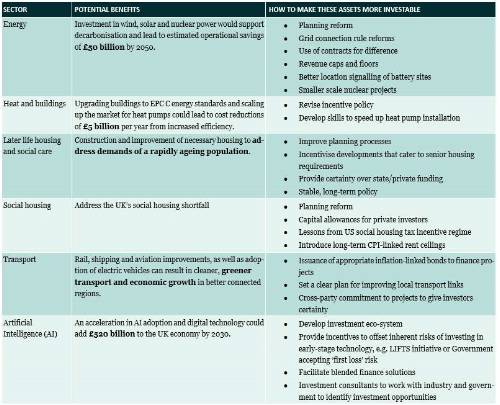

EXAMPLES OF REQUIRED ACTION BY SECTOR

NEXT STEPS

Crucially, pensions funds have a fiduciary duty and will only invest where the risk-return characteristics of potential investments meet the needs of their members. But with government, pension funds, investment managers, investee companies and consultants all playing their part, there is substantial potential to open the pipeline of assets to attract the investment of pension funds to support UK growth. This report makes specific recommendations for each of these groups (summary p. 12).

However, we highlight below our recommended actions for two of them: pension funds and the Government.

Trustees and pension funds should:

• Develop investment strategies that consider how to allocate to private market assets appropriately to meet the needs of the scheme and future liabilities. • Be aware that training may be required to ensure there is an appropriate level of knowledge and understanding of social and climate issues and how to integrate these into investment decisions. • Encourage advisers and consultants to further consider growth assets in investment strategies put forward for DB and DC schemes, and consider any gaps in service provider expertise. • Understand the risks involved in different types of investments and how to effectively diversify their portfolio, including clarifying fiduciary duty so trustees are clear that climate considerations can be compatible with their fiduciary duty. • Ensure Statements of Investment Principles clearly articulate trustee views on which investment sectors to prioritise. • Consider what blended finance structures would make sectors more investable.

We call on the government to:

• Provide policy and regulatory certainty to improve the UK’s appeal versus investment opportunities globally. This includes developing a long-term strategy for investment and growth, outlining the Government’s priority investment sectors, its approach to blended finance and how it will work with the pensions industry. • Offer targeted fiscal incentives to make UK growth assets more attractive than competing assets from other countries. Enhancing the tax treatment of domestic investments, as they do in France and Australia, merits further exploration. In addition, initiatives like LIFTS, which supports investment in UK start-ups and companies requiring late-stage growth capital, should also be considered. • Expand the area of focus beyond private equity and venture capital to encompass infrastructure, alternative assets and a variety of funding models. • Take control in bringing key industry groups together to develop solutions to growth challenges. • Produce a plan for the development of skills to achieve growth. • Lead and collaborate on AI and net zero at international scale. • Continue to work closely with regulators and others to get the right approach to investment risk, including DC, open DB and the LGPS, where this is in the interest of scheme members. • Deliver planning reform to enable crucial energy, infrastructure, social housing and later life care development Nigel Peaple, Director Policy & Advocacy, PLSA, said: “The UK has considerable need of greater investment to achieve the Government’s goals on growth and the transition to net zero. “Pension funds have an important part to play in achieving greater investment in the UK where this is consistent with achieving the right returns for pension savers. The PLSA has highlighted these issues in our conferences, supports the Mansion House Compact, provided input to the National Wealth Fund, and last year identified the policy and regulatory changes needed to achieve this goal. “Our new report looks at how to create more investible opportunities in the UK by identifying the Pension Fund and Government actions needed and calls on all parties to work together to achieve these goals.” Download the report

BACKGROUND

An estimated £1 trillion of pension fund capital is allocated to UK-domiciled assets, for structural reasons the majority is deployed in government debt, other fixed income assets and publicly listed companies. Since early 2023 there has been considerable debate about whether and how pension funds can be encouraged to allocate more to emerging – and higher risk – opportunities that could drive UK economic growth. In response, the PLSA identified six areas where either existing barriers could be removed or where pension funds might be incentivised or encouraged to allocate more to the domestic economy. These actions included: • Pipeline of assets: Ensuring there is a stream of high-quality investment assets suitable for pension fund needs. • DB regulation: Introducing greater flexibility into the funding regime for private sector DB schemes, in particular for open DB schemes and those schemes with longer investment time horizons. • Taxation: Introducing fiscal incentives for pension funds so that investing in UK assets is more attractive than investing in similar assets of other countries. • Consolidation: Prioritising the passage through Parliament of a Bill to place DB superfunds on a statutory footing and carrying forward, in a pragmatic way, its current programme of measures related to DC Master Trusts and the LGPS. • Market for DC under automatic enrolment: Taking a range of actions to encourage more focus on performance and less on cost, for example, the greater use of Value for Money tests and setting the right regulatory regime for advice to employers and schemes. • Raising pensions contributions: Increasing the flow of assets into DC schemes by raising automatic enrolment contributions from 8% to 12% over the next decade. |

|

|

|

| Take the lead client-facing projects ... | ||

| Various locations - Negotiable | ||

| Choose Life! Choose a major global co... | ||

| Various locations - Negotiable | ||

| Actuarial skillset? Apply now for Snr... | ||

| South East / hybrid with travel requirements - Negotiable | ||

| Financial Risk Leader - ALM Oversight | ||

| Flex / hybrid - Negotiable | ||

| Be the very model of a modern Capital... | ||

| London - Negotiable | ||

| Pensions Actuary seeking a high-impac... | ||

| London or Scotland / hybrid 3dpw office-based - Negotiable | ||

| Great opportunity for Pensions Actuar... | ||

| London or Scotland / hybrid 3dpw office-based - Negotiable | ||

| Responsible Investing Manager - Clima... | ||

| London/Hybrid - Negotiable | ||

| Quant Strategist | ||

| London/Hybrid - Negotiable | ||

| Multiple remote longevity contracts | ||

| Fully remote - Negotiable | ||

| Multiple remote inflation hedging con... | ||

| Fully remote - Negotiable | ||

| Play a vital role in shaping a new He... | ||

| London or Scotland / hybrid 50/50 - Negotiable | ||

| Support the Longevity team of a globa... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Delve into financial risk within a ma... | ||

| Wales / South West / hybrid 1dpw office-based - Negotiable | ||

| Project-based Life Pricing Actuarial ... | ||

| South West / hybrid 2 dpw office-based - Negotiable | ||

| Pricing Actuary | ||

| London - £120,000 Per Annum | ||

| Develop your career in motor pricing | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Experience real career growth in home... | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Be at the cutting edge of technical p... | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Use your passion for innovation and t... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd