By Jack Sharman, Principal and Senior Consulting Actuary and Lewys Curteis, Principal and Senior Consultant - Corporate Actuary at Barnett Waddingham

Nearly two years since Clara-Pensions became the first superfund to complete its regulatory assessment, and over five years since the Government’s original White Paper proposing a commercial consolidation market, we are still waiting for the first deal to be announced, and for new entrants to provide depth to the market.

In spite of market and regulatory headwinds, good progress has been made on isolated cases. But what has been holding back providers, and what more can be done to help the market grow?

Impact of market movements

In hindsight, 2022 was a very difficult year in which to attempt to launch a new risk transfer solution.

Over the past year significant increases in both short-term and long-term interest rates reduced the value placed on pension scheme liabilities. Although the net effects on individual schemes were varied (depending on their investment strategies and their responses to the ‘gilts liquidity crisis’), many schemes will have benefited from these market movements and seen material improvements in their funding levels.

To put that another way, many schemes will now find themselves in a much more advanced position on their ‘journey plan’ towards securing their members’ benefits than would have been expected two years ago.

The superfunds rely on being able to find schemes with funding levels such that the superfund premium is affordable but a full buyout is out of reach. The rapid progress in schemes’ journey plans means that many schemes previously targeted by superfunds have now found themselves closer to buyout, and are therefore considered unsuitable for a superfund transaction according to the Pensions Regulator’s (TPR) interim guidance.

This is supported by our experience advising clients in this area and our research with the superfunds themselves. A number of superfund deals have been close to completion, before the trustees and sponsors turned their attention instead to the bulk annuity market.

Of course, if some better-funded schemes have now moved beyond the reach of the superfunds, there will also be new schemes, previously too far behind on their journey plans, who are now coming into the ‘target zone’ for superfund pricing. A particular challenge with these schemes, however, may be that they have not yet carried out the preparatory work needed to ensure a smooth transaction process.

Regulatory challenges

A further constraint on this market is the onerous regulatory environment under which superfunds have been operating. As we have previously discussed, the high standards to which TPR is holding the superfunds under its interim regime means that the formal regulatory assessment process has taken several years to complete, delaying their ability to start engaging in earnest on potential transactions.

In the case of Clara, even after getting over the initial hurdle of regulatory assessment, there have remained significant barriers to completing transactions. The ‘gateway’ clearance process that schemes must pass before transacting with a superfund requires significant work from trustees and sponsors, with limited guidance as to how this will be supervised by TPR. This has no doubt been off-putting to some schemes which might otherwise have considered the superfund option.

Impact of the revised regime

Despite the well-publicised challenges, we do still believe there is a space in the market for consolidation alongside the traditional bulk annuity route. And the Government has made the case separately for more productive use of pension scheme assets through consolidation.

With this in mind, it was pleasing to see TPR recently reviewing its interim rules. The changes should help ease the way for the initial transactions by:

reducing the high funding requirements, allowing the superfunds to offer more competitive pricing relative to insurance companies whilst maintaining a high level of security for member benefits; and

applying greater flexibility in the timescales under which transactions will be assessed by TPR.

These changes are particularly important, because we are already seeing an incredibly busy insurance market. Where only schemes who prepare thoroughly can expect to get full engagement from insurers, it is important that other viable ‘exit routes’ for trustees and sponsors should exist.

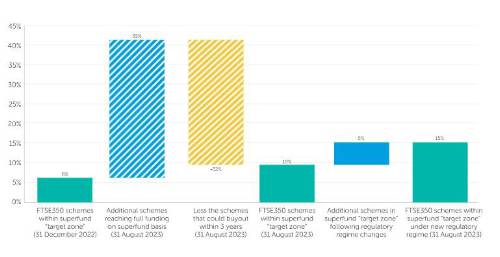

Our latest analysis of FTSE 350 schemes offers some encouragement for the superfunds. Our analysis shows that there remains a material proportion of schemes who might meet the requirements to pursue a superfund transaction, and that group will have expanded still further if the pricing becomes more competitive as expected in light of the new TPR guidance. This is illustrated in the chart below.

The chart shows that the regulatory regime changes have increased the proportion of FTSE350 schemes in the superfund ‘target zone’ (defined as having sufficient funding to transfer to a superfund without a contribution from the sponsoring employer, but where buyout funding is over three years away), illustrating the positive impact of the regulatory changes on the potential superfund market. There is also likely to be a wider group of schemes that could transfer to a superfund via a contribution from the sponsoring employer, expanding the potential market further.

One key item missing from the recent TPR review, however, was an updated stance on allowing superfund providers to return capital to investors during the lifetime of the arrangement if the portfolio performs well. TPR say they will return to this topic in future but, until they do, they are limiting the range of solutions available and dissuading new providers from exploring the superfund market.

These positive changes to the superfund regime may take some time to feed through the system. In the meantime, we continue to see strong interest in ‘capital-backed journey plan’ (CBJP) solutions. These can potentially achieve some of the same objectives as a superfund, but with more flexibility and fewer regulatory hurdles. We look forward to discussing the diverse and growing CBJP market in a future article.

|