Charles Cowling, Chief Actuary, JLT Employee Benefits, comments: “2018 was a turbulent year for pension schemes but it was not all negative. Markets were initially strong in the face of considerable political uncertainty and signs emerged that interest rates are at last on the way up. That said, there is no sign yet of an unwinding of the Bank of England’s position on quantitative easing. Additionally, the latest mortality analysis increasingly points to a sustained slowing down in the rate of improving life expectancy. All of this is good news for pension scheme deficits which have shown some modest improvement over the past year. At one point during the year, before Brexit fears resurfaced, the aggregate position for FTSE100 pension schemes moved into surplus for the first time in a decade.

“As the Bank’s Monetary Policy Committee (MPC) highlighted in its recent announcement, Brexit uncertainties have intensified considerably in recent weeks and these are weighing on UK financial markets, with significant falls in UK equities and pressure too on Sterling. All of this gave rise to increases in the outlook for inflation and a lowering of expectations for economic growth, yet still resulted in a unanimous vote from the MPC to keep interest rates unchanged and markets are not pricing in a rise in interest rates until the end of 2019. But that could all change.

“Tellingly, the MPC further commented that the broader economic outlook will continue to depend significantly on the nature of EU withdrawal and ‘The monetary policy response to Brexit, whatever form it takes, will not be automatic and could be in either direction … The Committee will always act to achieve the 2% inflation target’, underscoring the significant uncertainty that beckons in 2019.

“So, it is a very mixed picture for companies and their pension schemes. Some have successfully navigated the turbulent markets, have paid in significant additional contributions and are now looking to lock down on emerging pension surpluses by securing pension liabilities in the insurance market. We believe that 2019 will be another bumper year for insurance company buy-outs, possibly enhanced by the emergence of other superfund consolidators, who are looking at different and cheaper routes for companies to offload their pension liabilities.

“But other companies are still facing extremely difficult times. They may have gambled too much and in vain on equity returns and rising interest rates to save them from debilitating pension deficits. In particular the retail sector is seeing very difficult trading conditions. Christmas 2018 does not appear to have been kind to the high street. For the third consecutive year footfall has dropped with early indications suggesting a drop of 3% on last year. On top of this falling high street property values, as well as pension woes, are piling on the pressure. Household names such as Debenhams and Marks & Spencer are under pressure – particularly from hedge funds holding short positions – and it seems sadly inevitable that HMV will not be the only retail business falling into administration on the back of a poor Christmas.”

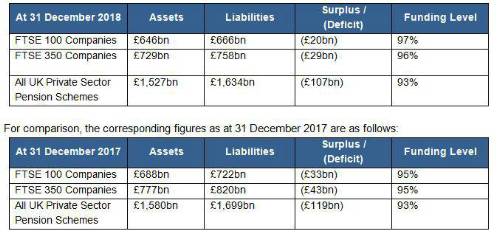

|