Key points:

An over-valuation of how long people are likely to live is equivalent to continuing to pay everyone’s pension for 4 months after they’ve passed away;

Companies with 2017 valuations could face bigger cash calls to shore up deficits than necessary. Given low interest rates, this has the potential to tip some schemes into closing;

Hedging out the uncertainty in future longevity trends becomes more affordable than many trustees think, and is now more accessible to smaller pension schemes.

Commenting, Douglas Anderson, Founder of Club Vita, said: “With rock-bottom interest rates causing pension deficits to swell, trustees and sponsors of defined benefit pension schemes need to avoid unnecessary margins in assumptions. Companies with schemes facing record funding deficits in 2017 valuations will be feeling the heat. They, and scheme trustees, should look at whether they’re taking an unnecessarily prudent approach. It could be distorting important decisions on the future startegy of their schemes.”

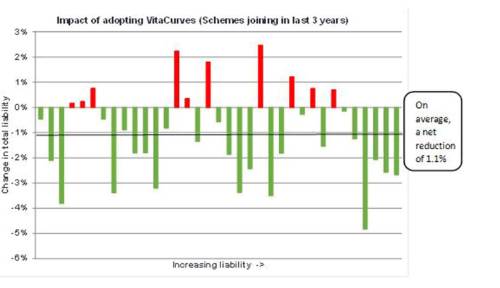

Analysis from Club Vita, which pools the longevity data of over 200 DB schemes and insurers, shows that trustees are typically still taking unnecessary margins in setting their longevity assumptions. For the latest DB schemes to join Club Vita, the chart below shows the change in valuation of each scheme’s liabilities from swapping the trustees’ previous assumptions for Club Vita’s best estimate assumptions, known as VitaCurves. Increases in the value placed on the scheme’s future liabilities are shown in red, whilst reductions are shown in green.

Source: Club Vita – 34 new schemes joining between July 2013 and June 2016, relative to each scheme’s previous technical provision assumption for baseline longevity

“When we take on a new scheme, on average there’s an over-valuation of liabilities of around 1%, with several schemes enjoying far larger reductions to their deficits. The 1% average reduction is equivalent to continuing to pay everyone’s pension for 4 months after they have passed away. If the same pattern was seen across all the UK’s defined benefit pension schemes, then deficits could fall by £25bn by adopting Club Vita’s methodology*. You might have expected that bigger schemes would be better at assumption-setting than smaller schemes but that’s not so, with several £1bn+ schemes overestimating liabilities by substantial amounts.”

Explaining what’s causing the over-valuation in longevity he added: “Having helped almost 250 schemes get a better handle on longevity risk over the last decade, we’ve observed three main causes. First, using final salary (as well as postcode) as a predictor of longevity refines the valuation of mid-sized pensions. Under the traditional approach, you don’t know whether a typical £5,000 annual pension relates to a long-serving, low-salary person or a short-service, high-salary person – two people would have very different life expectancies.

“Second, the data underpinning Club Vita’s survival tables is fresher than the CMI tables typically used by schemes and captures heavier mortality in recent years. For example, the 2016 VitaCurves data is based on 2012-2014, compared to CMI S2 tables which use data from 2007. Finally, when adjusting “standard” CMI tables, there is a natural behavioural bias to err on the side of caution in the face of uncertainty. VitaCurves capture a wider spectrum of diversity of our population than CMI tables (shown by the 10 years range of life expectancies rather than 5 years for CMI), reducing the need for subjective, manual adjustments.”

“Naturally, the ultimate cost of a pension scheme will be determined by how long its members actually live. But assumptions made today really do matter for such long duration commitments. The confidence that trustees gain from more insightful longevity assumptions does change behaviours, affecting members’ benefits, their security and businesses’ ability to invest.”

Explaining how managing longevity risk is no longer the preserve of larger schemes he added: “Rightly, we have seen longevity management move higher up schemes’ agendas. With DB schemes maturing and investment risk being dialled down, longevity is now a bigger risk than ever before. Fortunately, hedging out the uncertainty in future longevity trends may be more affordable than many trustees think. This is particularly relevant now that longevity insurance is available to smaller pension schemes through innovations like Club Vita’s VitaHedge service. Until fairly recently, insurers were only confident to offer attractive prices to the biggest schemes, but that’s now starting to change. Given a combination of increasing costs of longevity risk and improved access in the market, we expect many more schemes to take proactive steps to manage longevity risk in 2017.”

|