Analysis shows this could increase by a further £10bn when schemes have incorporated the latest data on the impact of the Covid-19 pandemic.

PwC’s Buyout Index - which tracks the position of the UK’s DB schemes against an estimated cost of insurance buyout - also continues to show that, on average, schemes have sufficient assets to ‘buy out’ their pension promises with insurance companies, recording a surplus of £160bn.

John Dunn, head of pensions funding and transformation at PwC, said: “Although schemes on the whole remain very well funded, there’s still plenty for the sponsors and trustees of the UK’s DB pension schemes to be thinking about. A big debate for the last two years has centred on how to allow for the impact of the pandemic in life expectancy projections. More data is now available and the emerging consensus is that the lingering effects of the pandemic are likely to reduce life expectancy compared to previous projections. Once pension schemes factor this new data into their valuations, it could increase the aggregate surplus by a further £10bn on a low reliance funding measure.”

Laura Treece, pensions actuary at PwC, added: “When setting assumptions about future life expectancy of pension scheme members, most actuaries use models from the UK’s Continuous Mortality Investigation (CMI). Since the pandemic began, the CMI’s models have allowed actuaries to decide how much weight they want to place on the higher mortality experienced during the pandemic - in essence a ‘Covid-19 allowance’. Initially the CMI, and many actuaries, opted to place no weight on the data during the pandemic years, as it was very hard to assess the longer term impact on life expectancy.

“However, the data is now more stable and for the first time the CMI believe that - sadly - it may be somewhat indicative of the future trend. Its latest model proposes to place a 25% weighting on the mortality experienced in 2022. For pension schemes that haven’t made any allowance for the pandemic, that’s broadly equivalent to assuming that their members will, on average, live for between half and three-quarters of a year less, depending on when life expectancy was last assessed. That could be equivalent to a 1.5% to 2% fall in liabilities. Even if half of schemes have already made a Covid-19 allowance, that’s £10bn extra funding for the rest. Every scheme is different so sponsors and trustees should make sure they understand how the pandemic and its associated effects have impacted members of their pension schemes specifically.”

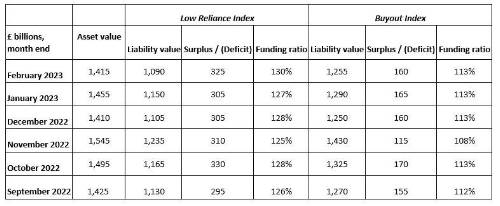

The PwC Low Reliance Index and PwC Buyout Index figures are as follows:

|