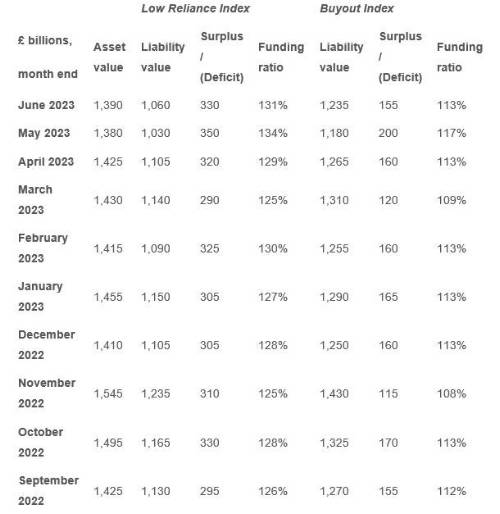

Meanwhile, the PwC Buyout Index recorded a surplus of £155bn in June, with a drop in gilt yields driving a reduction of £45bn compared to the previous month. This shows that on average schemes have sufficient assets to ‘buyout’ their pension promises with insurance companies, despite an increase in the estimated buyout cost over June.

With surpluses looking healthy, there is an increasing focus on whether more of the assets held in pension schemes can be invested in productive UK assets that could help drive economic growth.

John Dunn, head of pensions funding and transformation at PwC, said: “Despite continued turbulence in the gilt markets, UK DB schemes remain well funded. Given the resilience of the surplus and asset values holding up, we are seeing significant encouragement for DB schemes to invest more within the UK.

“This can be seen through the discussions the government is having with the pensions industry, with plans for ‘GB superfunds’ expected to be revealed in the Chancellor’s Mansion House speech next week. Just focusing on unlocking the c.£330bn surplus in UK defined benefit schemes would provide a lot of investment firepower. Although there are challenges to achieving a ‘GB superfund’, particularly answering the question ‘why would a fully funded DB scheme take more risk than needed?’ However, if done in a way which balances the interests of all stakeholders, there is a potential win-win-win scenario; with surplus funds available to invest in UK business, potential higher returns for pensioners and a boost to the UK’s economy.”

Laura Treece, pensions actuary at PwC, added: “Around half of the assets held by UK private sector DB schemes - about £700bn - are currently not invested in the UK, with about £200bn held in overseas equities. Investing even a proportion of this to support the UK could boost economic growth, while enabling pension schemes to make sure that they are generating the positive real returns needed to pay benefits for their members.

“But this might not be right for all schemes. For example, UK infrastructure is a long term illiquid asset; schemes looking to transfer to the insurance market in the short-term may not want to lock in to an asset they might not be able to pass to an insurer. However for others, if the new funding regime allows, investing in productive UK assets could be mutually beneficial for members, businesses and the wider UK economy.”

The PwC Low Reliance Index and PwC Buyout Index figures are as follows:

|