|

|

Most DB schemes in recent years have either started, or are well progressed, on a de-risking journey – moving from high-risk assets, such as equities, to assets that better match their liabilities (gilts, corporate bonds and LDI). The Pensions Regulator’s draft Funding Code of Practice takes this one stage further, by requiring schemes to put in place a de-risking plan so that they have a “low dependency” on their employer by the time they are “significantly mature”. |

Chris Ramsey, Partner and Head of DB Endgame Consulting at Barnett Waddingham But this creates several big questions for trustees. For starters, how should trustees make decisions on whether and when to de-risk? Should trustees worry about market volatility? And how should de-risking be managed in practice? Here are my top tips on managing your scheme’s de-risking journey:

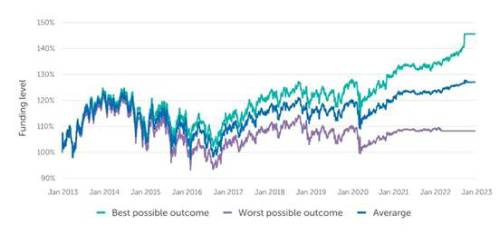

How much does volatility matter? For example, let’s say a scheme that was 100% funded at 1 January 2013 started a ten year de-risking plan, with 10% of its assets switching from equities to gilts each year. In this simplified example, the only choice the trustees would have had was when in the year they make the 10% switch from equities to gilts. The following chart illustrates just how wide the potential outcomes for this scheme were – with the best possible outcome being the scheme is 146% funded on 1 January 2023, the worst being 108% funded, and a full spectrum in between.

Most DB schemes in recent years have either started, or are well progressed, on a de-risking journey – moving from high-risk assets, such as equities, to assets that better match their liabilities (gilts, corporate bonds and LDI). All of these options had the same investment strategy and same journey plan on paper – the huge fluctuations are only caused by the trustees’ choice of when to implement the de-risking throughout the year. I wish I could say I had an easy way to make sure your scheme always picked the best or near-best time to de-risk – but that is not possible. None of us knows what markets are going to do next, and so trying to get a trustee board to predict this isn’t realistic. So what can you do? The best you can do is firstly decide what is “good enough” in your circumstances – i.e. what you would be happy with – then capture that opportunity if it emerges.

Deciding what is “good enough” – when should you de-risk? This is about getting the balance right between reducing risk (and expected return), reducing the contributions payable by the employer, trying to get to your target faster, or some combination of the three. Just because you think you are “ahead” doesn’t automatically mean you should de-risk – the employer in the example scheme shown in the chart below could argue that it would instead like to continue to take risk for longer to try to get to buy-out sooner.

Once that high level principle has been established it is time to get into the detail. There are many different ways of approaching de-risking, but I like to build de-risking strategies around the following two key principles:

Impact on funding This means understanding what the impact will be on the discount rate your Scheme Actuary will propose.

Impact on journey plan For example, if buy-out is your goal, your de-risking framework should check that you are still on target to reach buy-out in a sensible timeframe after you have done the de-risking. The last thing you would want to do is de-risk too much, and make buy-out an unrealistic goal.

How do you capture an opportunity?

1) Identify the opportunity early

2) Make your decisions up front

But having the right information at the right time isn’t good enough in and of itself. You also need to be able to take the necessary decisions quickly enough, and then also quickly implement the changes. This is where a lot of schemes could make changes to add value.

A month is not very long for trustees to decide what to do, consult the employer and then implement a change. And of course that is just an average – markets may move against you before then. That is why in my view is it is much more effective to make these decisions and have the discussion with the employer in advance. That way you have a good chance of moving quickly. There are various flavours of this type of arrangement – from de-risking triggers that are implemented without trustee input (“hard triggers”), triggers that are implemented only after trustee final sign off (“soft triggers”) or something more informal. Each of these approaches have their upsides and downsides, but the important point is they are all much more effective than the traditional model of considering quarterly reports at trustee meetings.

3) Consider the practicalities These issues may seem trivial, but they can frustrate a de-risking process if not thought through in advance.

Summary

Agree if, when and how you will de-risk in advance; |

|

|

|

| Take the lead client-facing projects ... | ||

| Various locations - Negotiable | ||

| Choose Life! Choose a major global co... | ||

| Various locations - Negotiable | ||

| Actuarial skillset? Apply now for Snr... | ||

| South East / hybrid with travel requirements - Negotiable | ||

| Financial Risk Leader - ALM Oversight | ||

| Flex / hybrid - Negotiable | ||

| Be the very model of a modern Capital... | ||

| London - Negotiable | ||

| Pensions Actuary seeking a high-impac... | ||

| London or Scotland / hybrid 3dpw office-based - Negotiable | ||

| Great opportunity for Pensions Actuar... | ||

| London or Scotland / hybrid 3dpw office-based - Negotiable | ||

| Responsible Investing Manager - Clima... | ||

| London/Hybrid - Negotiable | ||

| Quant Strategist | ||

| London/Hybrid - Negotiable | ||

| Multiple remote longevity contracts | ||

| Fully remote - Negotiable | ||

| Multiple remote inflation hedging con... | ||

| Fully remote - Negotiable | ||

| Play a vital role in shaping a new He... | ||

| London or Scotland / hybrid 50/50 - Negotiable | ||

| Support the Longevity team of a globa... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Delve into financial risk within a ma... | ||

| Wales / South West / hybrid 1dpw office-based - Negotiable | ||

| Project-based Life Pricing Actuarial ... | ||

| South West / hybrid 2 dpw office-based - Negotiable | ||

| Pricing Actuary | ||

| London - £120,000 Per Annum | ||

| Develop your career in motor pricing | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Experience real career growth in home... | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Be at the cutting edge of technical p... | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Use your passion for innovation and t... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd