When taking on a new job, salary is usually one of the biggest deciding factors, while the benefits and pension package can often be an afterthought. However, new analysis from Standard Life, part of Phoenix Group, demonstrates how the pension contribution levels a company offers can have a huge impact on retirement outcomes, and should therefore be a key consideration when job hunting.

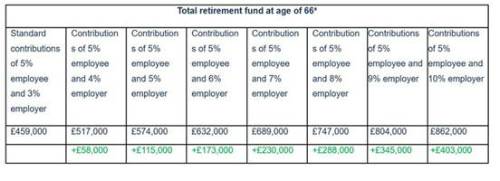

Someone that began working full-time at a company with a salary of £25,000 per year and paid the standard monthly auto-enrolment contributions (5% employee, 3% employer) from age of 22, would amass a total retirement fund of £459,000 at the age of 66, not taking inflation into account. However, if they were to join a company on the same salary but with a more generous company pension scheme that paid an additional 2% (5% employee, 5% employer) from the age of 22, they would accumulate £574,000 by the age of 66* – an extremely significant £115,000 more than the standard contributions would achieve.

*assuming £25,000 starting salary, 3.50% salary growth per year, and 5% a year investment growth. Figures are not reduced to take effect of inflation. Annual Management Charge of 0.75% assumed. The figures are an illustration and are not guaranteed. Earning limits not applied.

To emphasise this further if a company was to contribute even more, for example an additional 5% (5% employee, 8% employer) from the age of 22, a pension pot of £747,000 would be achieved – £288,000 more than standard.

Dean Butler, Managing Director for Customer at Standard Life said: “Workplace pension packages can massively differ, and it’s therefore important to understand what your employer is offering when deciding whether to start a new job. Our analysis shows that even a small increase in monthly pension contributions from your employer can have an extremely significant impact over the course of a career.

“For example, if you had two different jobs offers that pay the same salary, but one offer includes a pension package that pays just 2% more in pension contributions (5% employee and 3% employer vs 5% employee and 5% employer), this would produce £115k of additional savings by the time you retire. That’s the equivalent of around 42 months of average salary for a UK full time worker**. The more generous your employer’s pension package, the bigger impact it could have over time.

“Of course, there are many factors to take into account when accepting a job offer, including salary, but the full benefits package should be considered as part of the decision-making process. It’s worth taking time to understanding the short- and long-term impact on both your monthly income and pension savings, so you can weigh up what’s best for your individual circumstances.”

|