|

|

The European Insurance and Occupational Pensions Authority (EIOPA)’s latest report on the Prudential Treatment of Sustainability Risks marks a significant step in aligning prudential frameworks with sustainability objectives. Focused on transition risks, non-life underwriting impacts, and social risk integration, the report outlines potential changes that could reshape insurers’ balance sheets and capital strategies. Headlining the recommendations is a call for higher capital charges to reflect transition risks in fossil fuel-linked assets: |

By Bob Tyley, Head of Credit Risk and Sarah Dawes, Senior Consultant at Hymans Robertson Headlining the recommendations is a call for higher capital charges to reflect transition risks in fossil fuel-linked assets: 40% multiplicative increase for bonds 17% additive increase for stocks. EIOPA’s analysis highlights that many insurers’ models fail to account for the role of climate adaptation measures in reducing underwriting risks, potentially overlooking key risk mitigations. On social risks, EIOPA stresses its increased relevance and recommends further guidance for assessing these risks in the ORSA. The report, published on 7 November 2024, was in response to Article 304c of the Solvency II Directive, which mandated EIOPA to assess the potential for dedicated prudential treatment of assets and activities associated with environmental or social objectives. EIOPA shared its findings and recommended policy implications with the European Systemic Risk Board. The Board will review the report and consider the suitability of the implementation of the recommendations. If the recommendations are implemented, EIOPA-supervised insurers (including UK insurers with EU operations) will be directly affected. In their ‘Dear CEO’ letter on 11 January 2024, the Prudential Regulation Authority (PRA) confirmed they will be updating Supervisory Statement 3/19, which will expand on its expectations of how UK insurers should manage the financial risks from climate change. Undoubtedly, the PRA will reflect on EIOPA’s recommendations and the new UK government’s policy stance on climate. We expect the PRA will consult on its update to SS3/19 later in 2025.

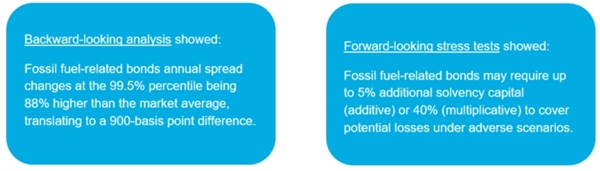

Transition Risk: A Call for Action on Fossil Fuel Exposures EIOPA analysed the impact of transition risk on the market value of bonds, equities, and property portfolios. The analysis includes backward- and forward-looking methodologies using historical data and disorderly transition scenarios. Key findings include: Spread Risk: Fossil fuel-related bonds showed the highest risk across most scenarios, with larger risk differentials in sectors such as mining, oil refining, and electricity generation. Narrow portfolio analysis identified fossil fuel portfolios as significantly riskier than broader market portfolios.

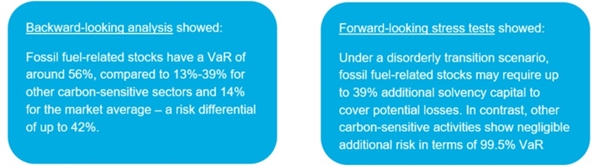

Equity Risk: Fossil fuel equities demonstrated elevated risk, especially in the sectors of mining, utilities, and oil and gas. The forward-looking analysis produced confirmed these sectors are highly sensitive to transition shocks.

Property Risk: The energy efficiency of buildings inconsistently affected risk, with only the least energy-efficient properties showing higher losses. However, various data limitations were noted, and a repeat of the analysis was suggested with the availability of improved data. The analysis indicates increased balance sheet volatility, prompting the need for measures to protect consumers and stakeholders from potential threats to firms' financial soundness. EIOPA evaluated policy options to address this, including no change, adjusted asset treatment, and dedicated capital requirements. Based on impact assessments, EIOPA has recommended the following specific capital charges:

A 40% multiplicative increase in capital charges of fossil fuel-related corporate bonds. Due to mixed evidence, no definitive treatment for property risk has been recommended at this time. Insurers may choose to move their investment strategies away from fossil fuel-intensive assets to mitigate these increased capital requirements. The impact is likely to be greater for Standard Formula firms, who have less flexibility than Internal Model firms to adapt their risk calibrations. However, insurers with minimal exposure to these assets may see only marginal impacts. Ultimately, the findings highlight the need for insurers to assess transition risks in their portfolios and consider adapting investment strategies accordingly.

Non-Life Underwriting: Allowing for climate adaptation Despite the potential difference in risks for products with and without adaptation measures, EIOPA reports that most internal models currently make no explicit allowance for this in the SCR. The report investigates what prudential treatment could be recommended. Using quantitative analysis of premium risk data, EIOPA finds an average reduction in the premium risk standard deviation parameter of 18% when comparing underwriting pools with adaptation measures to those without. The findings suggest a moderate impact of adaptation measures on premium risk. However, further analysis is needed for a more robust conclusion due to the small data sample size. For non-life insurers, this presents both a challenge and an opportunity. Whilst no immediate changes to prudential treatment are recommended at this time, firms should consider how to incorporate adaptation measures into their risk frameworks to better reflect their actual exposure and resilience.

Social Risks: Enhancing risk management

adequate living standards and working conditions. These have direct and indirect relevance for insurers’ assets and liabilities. EIOPA’s report stops short of recommending specific capital charges or disclosure requirements under Pillars I and III due to limited data. Instead, EIOPA suggests the development of guidance for assessing social risks through the Pillar II ORSA framework. This signals a growing regulatory expectation that insurers must demonstrate robust governance and proactive management of social risks.

Strategic Impacts for Insurers

Risk models should incorporate climate adaptation measures and transition risk more explicitly to reflect the evolving risk landscape accurately. Insurers primarily need to consider how proactive and forward-looking their approaches are to risk management, investment strategy, and product development are. |

|

|

|

| Take the lead client-facing projects ... | ||

| Various locations - Negotiable | ||

| Choose Life! Choose a major global co... | ||

| Various locations - Negotiable | ||

| Actuarial skillset? Apply now for Snr... | ||

| South East / hybrid with travel requirements - Negotiable | ||

| Financial Risk Leader - ALM Oversight | ||

| Flex / hybrid - Negotiable | ||

| Be the very model of a modern Capital... | ||

| London - Negotiable | ||

| Pensions Actuary seeking a high-impac... | ||

| London or Scotland / hybrid 3dpw office-based - Negotiable | ||

| Great opportunity for Pensions Actuar... | ||

| London or Scotland / hybrid 3dpw office-based - Negotiable | ||

| Responsible Investing Manager - Clima... | ||

| London/Hybrid - Negotiable | ||

| Quant Strategist | ||

| London/Hybrid - Negotiable | ||

| Multiple remote longevity contracts | ||

| Fully remote - Negotiable | ||

| Multiple remote inflation hedging con... | ||

| Fully remote - Negotiable | ||

| Play a vital role in shaping a new He... | ||

| London or Scotland / hybrid 50/50 - Negotiable | ||

| Support the Longevity team of a globa... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Delve into financial risk within a ma... | ||

| Wales / South West / hybrid 1dpw office-based - Negotiable | ||

| Project-based Life Pricing Actuarial ... | ||

| South West / hybrid 2 dpw office-based - Negotiable | ||

| Pricing Actuary | ||

| London - £120,000 Per Annum | ||

| Develop your career in motor pricing | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Experience real career growth in home... | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Be at the cutting edge of technical p... | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Use your passion for innovation and t... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd