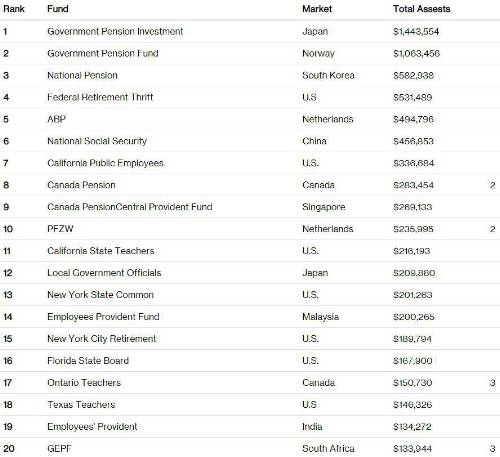

The research conducted in conjunction with Pensions & Investments, a leading U.S. investment newspaper, shows the top 20 funds account for 41.1% of the AUM in the ranking, marking a slight increase from 40.3% in the previous year.

Emerging markets have become more prominent in the rankings in recent years, with the Employees’ Provident Fund (India) a new entrant into the top 20 in 2017. A total of four new entrants from emerging market countries have entered the top 20 over the last ten years, from Asia (3) and Africa (1).

Roger Urwin, global head of investment content at Willis Towers Watson, said: “The increased number of the largest funds originating from emerging market regions is reflective of a longer-term trend, with a great deal of progress being made in terms of governance structures and resiliency. These countries are especially interesting to monitor as they are typically in the earlier stages of maturity and can continue to adapt and develop their investment models.”

Commenting on the findings, Bob Collie, head of research for the Thinking Ahead Group added: “This is a period of extraordinary change for large pension plans, driven by a confluence of factors. It’s not just demographic change and the changing global economic balance; it’s not just changes in social expectations, politics, sustainability, or regulation; it’s not just technology. It’s all of these, and it’s the way the changes compound one another. Many of these organisations are fairly young and have grown rapidly. This puts a spotlight on their governance and how they operate.”

Among the top 300 funds, defined contribution (DC) assets increased during 2017 by 17.6% whilst defined benefit (DB) assets grew 13.5%. DB assets accounted for 64.7% of the disclosed total AUM, (down from 65.5% in 2016).

The share of reserve funds (those set aside by a national government against future liabilities) saw a slight increase at 11.8% (11.5% in 2016), whilst hybrid funds (those with both DB and DC components) accounted for less than 1% of the total.

“Whilst the longer-term shift from DB to DC is widely understood and remains unchanged, it is striking that DB assets continue to grow and form the majority of the total assets. We see the hybrid market as an interesting area of the landscape to watch, with its growth expected to continue as asset owners shift away from traditional DB strategies,” Urwin added.

Sovereign and public sector pension funds account for 68.6% of the total assets, increasing by 0.2% from 2016.

North American funds remain the largest region in terms of AUM, accounting for 42.3% of all assets in the research, followed by Asia-Pacific (27.3%) and Europe (26.5%). North America shows the fastest annualised growth during the period 2012/17 at 6.2%, slightly outpacing Asia-Pacific’s 6.1% and Europe’s 3.8%.

A total of 26 new funds entered the top 300 over the last five years, with the U.S. contributing the greatest net number of new funds (9). The U.S. continues to have the largest number of funds within the top 300 ranking (133), followed by the U.K. (25), Canada (18), Japan and Australia (both 17).

On a weighted average for the top 20 funds, assets are predominantly invested in equities (46.3%), followed by fixed income (36.1%), and alternatives and cash (17.6%). Looking at the allocations by region, APAC funds had the largest allocation to fixed income (52.5%) and North American the largest allocation to alternatives (34.8%).

Top 20 pension funds (US $ millions)

1. The Thinking Ahead Group is the executive team to the Institute

2 . As of March 31, 2018

3. As of March 31, 2017

|