|

|

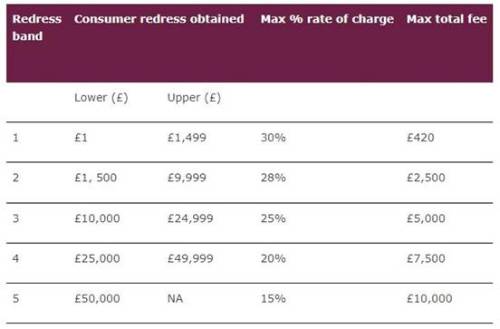

From today, new restrictions will apply to claims management companies (CMCs) to prevent them from charging excessive fees to consumers owed compensation from financial services firms. |

Under new Financial Conduct Authority (FCA) rules in force from today, the maximum consumers can be charged will depend on how much redress they are due. For example, if the redress amount is below £1,500 consumers can only be charged a maximum of 30% of their claim, or £420, whichever is lower. (See redress bands below for full details and maximum charges). The changes are expected to save consumers £9.6m a year and thousands of pounds on some individual claims. The cap will apply to most claims where a consumer is awarded monetary redress from a financial services firm, either directly from a firm, via the Financial Ombudsman Service (Ombudsman Service) or if a firm has gone out of business, from the Financial Services Compensation Scheme (FSCS). For other financial services claims, the rules require charges to be reasonable. The new rules do not apply to PPI claims which are already subject to a 20% cap, set by Parliament. The rules mean CMCs must also disclose key information to consumers before entering a contract, such as giving more detail about how fees will be calculated and making sure they are aware of the free routes to redress available. For example, if consumers make a complaint or a compensation claim themselves to the Ombudsman Service or the FSCS they would keep all redress awarded. Sheldon Mills, Executive Director of Consumers and Competition at the FCA, said: 'Our rules protect consumers from losing a significant amount of their compensation in excessive fees, particularly when there are ways for them to make claims without incurring any fees. 'The changes are part of our ongoing work to drive a fundamental shift in industry mindset so we can stop consumer harm before it happens, and to ensure more consistent standards of protection'.

|

|

|

|

| Take the lead client-facing projects ... | ||

| Various locations - Negotiable | ||

| Choose Life! Choose a major global co... | ||

| Various locations - Negotiable | ||

| Actuarial skillset? Apply now for Snr... | ||

| South East / hybrid with travel requirements - Negotiable | ||

| Financial Risk Leader - ALM Oversight | ||

| Flex / hybrid - Negotiable | ||

| Be the very model of a modern Capital... | ||

| London - Negotiable | ||

| Pensions Actuary seeking a high-impac... | ||

| London or Scotland / hybrid 3dpw office-based - Negotiable | ||

| Great opportunity for Pensions Actuar... | ||

| London or Scotland / hybrid 3dpw office-based - Negotiable | ||

| Responsible Investing Manager - Clima... | ||

| London/Hybrid - Negotiable | ||

| Quant Strategist | ||

| London/Hybrid - Negotiable | ||

| Multiple remote longevity contracts | ||

| Fully remote - Negotiable | ||

| Multiple remote inflation hedging con... | ||

| Fully remote - Negotiable | ||

| Play a vital role in shaping a new He... | ||

| London or Scotland / hybrid 50/50 - Negotiable | ||

| Support the Longevity team of a globa... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Delve into financial risk within a ma... | ||

| Wales / South West / hybrid 1dpw office-based - Negotiable | ||

| Project-based Life Pricing Actuarial ... | ||

| South West / hybrid 2 dpw office-based - Negotiable | ||

| Pricing Actuary | ||

| London - £120,000 Per Annum | ||

| Develop your career in motor pricing | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Experience real career growth in home... | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Be at the cutting edge of technical p... | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Use your passion for innovation and t... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd