The fiduciary management (FM) industry has faced a multitude of challenges this year as it strives to adapt to the new landscape following the CMA Review and the testing market conditions posed by a rotation away from growth assets, War in Ukraine and a Treasury-inspired gilt crash and LDI collateral crisis.

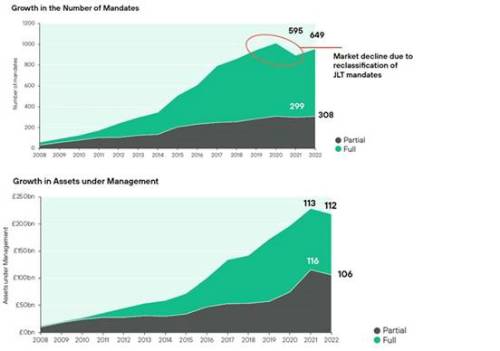

Despite these challenges, FM rebounded in 2022 with the total number of mandates growing 7% versus 2021. However, the growth rate remains below pre-2020 levels, suggesting growth may have peaked, while the industry’s total assets under management (AUM) fell for the first time since pre-2008.

Isio’s annual FM survey, ‘Latest trends in Fiduciary Management’ quantifies the impact of challenging market conditions for fiduciary managers, finding that total AUM decreased 5% to £218bn in 2022, largely as result of a rise in yields driving declines in gilts and LDI portfolios, and the difficult backdrop for growth assets.

Isio found that the impact of market conditions on AUM was significant enough to outweigh the rise in assets from pension schemes that were new to fiduciary management over the year. In 2022, a few large schemes entered the market through OCIO solutions with fiduciary providers and, without these, the fall in AUM would have been much greater.

Growth of smaller FM mandates

While the number of £1bn+ pension schemes using FMs has increased, the percentage of the market they represent stayed level. By contrast, there was a more significant increase in the number of smaller schemes using FMs and those with less than £100m in assets now represent 62% of all mandates by number, versus 54% in 2021.

Big mandates drive down fees

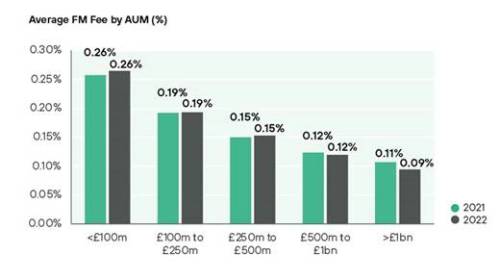

Isio asked FMs what their fee would be for a scheme targeting a return of gilts + 2% per annum in five different asset size buckets. The data shows no movement in fees over the year except for schemes of £1bn+ in size, which have driven down fees from 0.11% in 2021 to 0.9% in 2022. The data contrasts sharply with the previous year when fees for schemes of £1bn+ increased (from 0.10% in 2020 to 0.11% in 2021), while those for every other mandate size stayed the same or fell.

Fee pressure from larger schemes is likely a result of continued retender activity prompted by the CMA’s review and 2021 deadline, competitive pressures in the market between fiduciary managers and operational costs decreasing, from technology improvements to economies of scale.

A positive outlook

Despite the challenges of the past year, pension schemes are moving rapidly along their journeys towards buy-out and self-sufficiency, buoyed by the strong performance of growth assets in the post March 2020 environment and the more recent decrease in buy-out liabilities as yields have risen. Connected to this, Isio found higher liability hedging targets across all fiduciary managers up to June 2022, with the proportion of schemes more than 80% hedged rising from 68.6% in 2019 to 94.1% in 2022.

In parallel, FMs have decreased return targets for schemes, with the proportion targeting 2.51%-3.5% above liabilities falling from 28.6% in 2019 to 21% in 2022. Meanwhile, those with targets of 0.51% to 1.5% above liabilities rose from 24.2% in 2019 to 34.4% in 2022.

From equities to credit

Isio asked FMs how they would invest the assets of a £500m scheme to target a return of gilts plus 2% per annum and found the average strategic asset allocation is diversifying away from equities, however the split between hedging and growth assets over the past three years has remained broadly stable.

Credit has been the main beneficiary, with allocations rising 5.7% to 22.8% at a total portfolio level since 2019. Meanwhile, equity allocations fell from 20.6% to 15.7% over the same time period.

Paula Champion, Head of Fiduciary Oversight at Isio said: “This year’s market volatility and challenging macroeconomic environment have tested fiduciary managers, shrinking total AUM despite a healthy increase in mandates among the largest and smallest schemes.

“While it’s great to see schemes are further along their journeys to buyout and self-sufficiency, and the impacts of the CMA’s review are now bedded in, there are significant hurdles ahead for the FM industry. First and foremost is the decision on whether to continue increasing hedging levels following the LDI crisis, as well as a broader revaluation of the role that LDI, which had been increasingly significant to portfolios, should play from here.

“Longer-term, FMs will have to adapt to both the increasing impact of regulation, in particular around ESG, as well as the changing face of the industry as DB schemes mature. Currently Task Force for Climate-Related Financial Disclosures (TCFD) reporting requirements only apply to schemes with assets exceeding £1bn, but we expect this to be extended to all schemes in the foreseeable future.

“And while DC only accounts for 11.4% of FM mandates versus 88.6% of mandates which are DB schemes, the balance will shift in the future with significant implications for the FM market.”

|