In this thought provoking paper, sponsored by Partnership, the author puts forward persuasive arguments why annuities will continue to play an important role in retirement income planning. Looking to the future, he suggests that innovation, a more sophisticated use of these products, deeper understanding of behavioural issues and an increase in personal underwriting will further increase their attractiveness.

With mortality drag being arguably one of the least understood aspects of annuities, Billy looks to further explain this phenomenon and provide the first comprehensive review of it in relation to enhanced annuities. He describes mortality drag as being like an invisible force that provides an important boost to annuity payments and consequently makes it harder for drawdown policies to provide the same level of income without the investor taking undue risk.

Essentially, when someone buys an annuity, they benefit from the mortality cross-subsidy i.e. those who die before their normal life expectancy subsidises those who live longer, but those who invest in a drawdown plan don’t benefit from this mortality cross-subsidy.

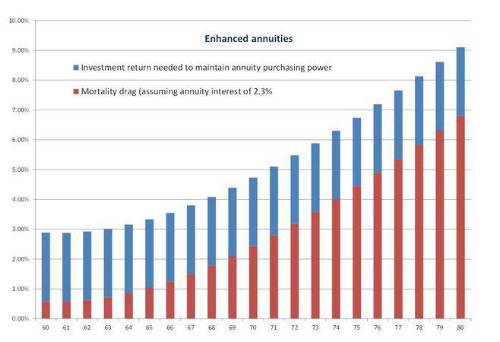

The chart below shows the additional investment returns need in order for a drawdown plan to maintain its annuity purchasing power each year for someone who qualifies for an enhanced annuity. At age 70, the additional investment return required is nearly 4.73% return before charges.

Mortality Drag [Standard vs. Enhanced Annuities]:

Billy Burrows, commented

“It is important to separate the benefits of annuitisation from the poor image associated with some annuity policies. The case for annuities can be made strongly on a number of fronts when the benefits such as a guaranteed income for life are examined and the outcomes compared to products such as drawdown. As the mortality drag chart shows, annuities, especially enhanced, are a hard to beat when compared to drawdown. The investment returns required to maintain the annuity purchasing power increase with age and this is the time when investors should be taking less risk not more.”

Andrew Megson, Managing Director of Retirement at Partnership, said

“As an enhanced annuity provider, we are obviously convinced of the benefit of our products but we felt it was important for them to be analysed by analysed by a well-respected independent commentator. This is a report that advisers and consumers can use to fully understand when and why annuitisation makes sense. Mortality drag is one of the least understood aspects of annuities and this paper helps to explain this phenomenon as well as clearly highlights where and why annuities still have an important place and are beneficial for many retirees.”

|