Nearly four million workers, many in their 20s and 30s, are only saving at the minimum rates set by the government, and cannot hope to ease their way gently into retirement in later life.

The report, ‘The Mirage of Flexible Retirement’, builds on previous analysis by Royal London which highlighted the way that low levels of pension saving under the ‘automatic enrolment’ programme could leave people unable to afford to retire. It finds that the frequently discussed idea of a ‘flexible’ or gradual retirement may be a ‘mirage’ for millions of people saving at current levels.

The new research looks at what would happen if someone who has only saved into a pension at the legal minimum level who decides to draw a state pension as soon as they can and immediately cuts down to part-time work. It considers those who are targeting a ‘gold standard’ retirement (where income at retirement is two-thirds of pre-retirement levels) or a ‘silver standard’ retirement (where income at retirement is half of pre-retirement levels).

For those who want a pension which simply provides a flat income with no protection against inflation and no support for a widow or widower, the research finds:

- A worker targeting a ‘gold standard’ retirement who retires gradually will have to work until they are 79 before they can afford to retire; this compares with retirement at 74 for a worker who defers taking a state pension and maintains full-time hours until they stop working;

- A worker targeting a more modest ‘silver standard’ retirement but who retires gradually would have to work on until they were 69; this compares with retirement at 68 for a worker who defers their state pension and continues in full-time work;

Those targeting a pension which provides protection against inflation and something for a widow or widower could still be working into their 80s before they have enough money to afford to retire.

As well as offering these stark warnings about the implications of starting the process of retirement too soon, the report does offer some hope. It finds that these extreme retirement ages are the product of simply putting too little money into a pension. If people save more than the legal minimum of 8% into a pension the report finds:

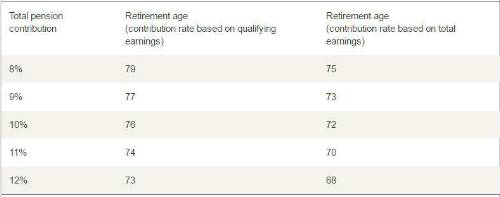

- A contribution rate of 10% allows an individual to retire around three years earlier, whilst a contribution rate of 12% allows an individual to retire around six years earlier;

- As a rule of thumb, even for workers who do not start saving into a pension until they are in their thirties, each extra 1% on the pension contribution rate reduces the number of years that they have to work by at least one year;

The table shows these results in more detail, with contribution rates based first on the current rules which apply only to a band of ‘qualifying earnings’ and then to contribution rates based on contributions applying from the first pound of earnings.

Estimated retirement ages for an average earner to achieve ‘gold standard’ retirement – impact of different contribution rates

Table assumes that the individual is targeting an income in retirement with no inflation-linked increases and no provision for a surviving spouse or partner.

With average earnings assumed at £27,600 per year, an additional 1% of ‘qualifying earnings’ (the excess over the floor of £5,824) would be just over £4 per week, including any contribution from the employer, the employee and tax relief. In other words, even relatively modest increases in the amount saved can have a significant impact on working lives.

Commenting on the results, Steve Webb, Director of Policy at Royal London said: “A flexible retirement, where we can gradually reduce our hours and stop work at an acceptable age, is likely to be a mirage for millions of people based on current levels of saving. Those who opt for a gradual retirement, drawing a state pension as soon as they can and cutting their working hours could easily find themselves unable to afford to retire fully until they are in their late seventies or beyond unless they have built up a significant private pension pot”.

“The good news is that there is an antidote to excessive working lives and this is higher rates of pension contributions. We find that each one per cent on pension contribution rates takes at least one year off the number of years for which you have to work to achieve a decent retirement. For those who want to have choices in later life about when and how they retire, doing more now to build up a decent pension pot is becoming essential. These findings need to be considered carefully by the Government as it reviews the rules around automatic enrolment in 2017”.

|