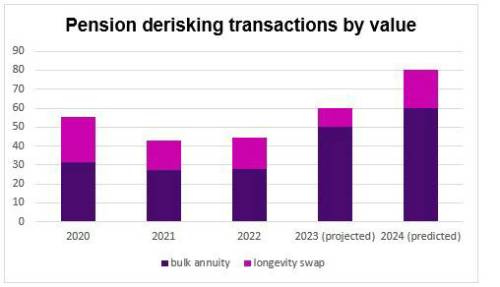

According to WTW’s annual Pensions De-risking report, insurers are primed to buy out £60bn in bulk annuity transactions and £20bn in longevity swaps this year, making 2024 the biggest year on record for pensions de-risking.

Last year saw historically high numbers of pension schemes securing their liabilities through an insurance led buyout, with over £50bn written in bulk annuity transactions alone. WTW expects this trend to only increase, with many schemes having already changed their investment strategies to lock in favourable funding positions throughout the year and many also preparing their data in order to approach the insurance market this year.

Jenny Neale, director in WTW’s Pensions Transactions team, said: “It’s clear that funding improvements have turbo-charged the pensions de-risking market and, from a capacity perspective, we have already seen that the insurance market is capable of scaling up to meet demand. The attractiveness of these opportunities is also enticing new insurers to enter the market adding additional capacity, which we believe will be sufficient to meet requirements in the year to come.”

“Despite the increased demand for de-risking, the Chancellor’s proposed Mansion House Reforms could give pause for thought for some pension schemes and their sponsoring employers. Whilst we expect buyout to be the long term destination for the majority of our clients, we have seen a number of schemes with strong sponsors initiating a fresh review of their long-term target and more schemes may choose to seek value in running on their pension scheme and delaying their move to buyout if a change in legislation allows easier use of any surplus run by the scheme,” said Neale. “If this is the case, it’s unlikely that these schemes would wish to run unrewarded risks and consequently could look to hedge their demographic risks through the use of longevity swaps.”

In addition to record high deal values, WTW is also anticipating several other developments in the UK pensions de-risking market in 2024, including:

An increased focus on non-price factors when selecting an insurer:

While price remains an important consideration, trustees will increasingly prioritise other factors, such as brand reputation, member experience and financial strength, when selecting an insurer. With more schemes considering full scheme buy-ins as a stepping stone to buyout, member experience will be an increasingly important consideration.

Opportunities for schemes of all sizes:

Despite the choice of transactions on offer, insurers are continuing to support schemes of all sizes. In 2024, WTW expects to see more multi-billion pound transactions for large pension schemes, as well as suitable counterparties for smaller schemes to transact with. However, in a busy market, the quotation process will need to be tailored to each scheme's situation to maximise insurer engagement.

Superfund transactions for the right schemes:

With the first superfund transaction taking place in 2023, this year will be crucial in the superfund market's development as pension schemes explore whether this option suits their circumstances. While superfunds may not become a mainstream endgame for the majority, a few transactions in 2024 could pave the way for future momentum in the space.

|