|

|

Major geopolitical events are rarely out of the headlines, but as Matt Tickle examines, are they really driving movement in investment markets? Geopolitical concerns have arguably been at an elevated level for much of the past decade; however, these truly came into focus with the economic and financial disruption following the Russian invasion of Ukraine. These concerns have spread with the expanding conflict in the Middle East over the past nine months. |

By Matt Tickle, FIA, Partner and Chief Investment Officer at Barnett Waddingham.

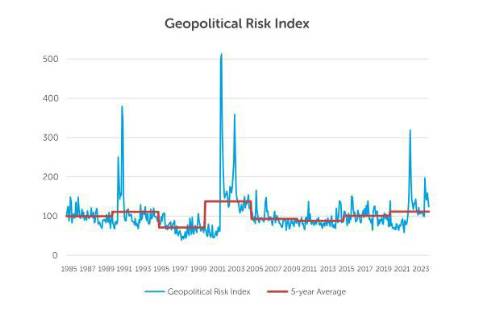

Source: Caldara, Dario and Matteo Iacoviello (2022), “Measuring Geopolitical Risk” However, while the humanitarian impact is always terrible from any conflict, the unfortunate reality is that for most recent conflicts the economic impact has been limited. Another source of uncertainty are elections. These can dominate headlines with coverage of often small changes in opinion polls and campaign promises that are not always enacted. In contrast, seemingly small and lightly reported policy changes or rising geopolitical tensions between major economies can have a substantial economic impact. In this blog we explore how investors can make better decisions by taking a step back from those geopolitical developments that will dominate headlines, but that are unlikely to reward the time spent following them, and instead focusing time and energy on those developments that could have the largest impact on your portfolio.

Conflict in the Middle East

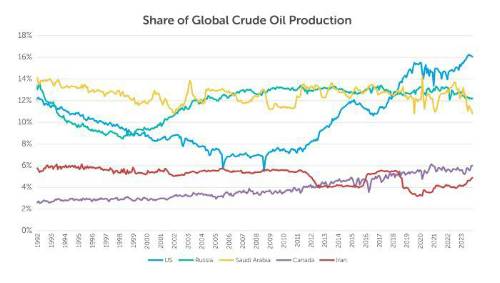

Energy markets The world is far less dependent on oil overall than it used to be. The amount of oil required per unit of global GDP is less than half of that required in the 1970’s. The US is the world’s largest oil producer for the first time since the early 1970’s. Therefore, the world is far less dependent on Middle Eastern oil than it was in the 2000’s at the low point of US production.

Despite heavy sanctions since 2022, Russian production has barely fallen, although the ultimate destination of the oil has changed.

Source: Refinitiv, International Energy Agency There is a risk to this view however, stemming from the disruption of maritime trade, particularly through the Strait of Hormuz. The Iranian-backed Houthis have shown their ability to disrupt shipping elsewhere, in the Red Sea, which has raised shipping prices, albeit with prices remaining far below the post-pandemic high points of 2021 and 2022. However, fully blocking this chokepoint would likely dramatically escalate the conflict, potentially bringing Saudi Arabia and the other Gulf states into direct confrontation with Iran. Because this would be such a huge escalation, markets consider it unlikely and have done little to price in this outcome. Instead energy markets have continued to move more in line with changes in macroeconomic factors such as global growth.

Investors’ exposure to the region

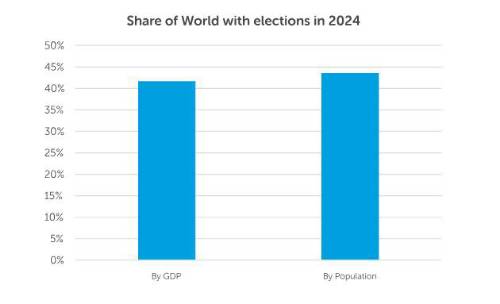

2024: the year of elections

However, even in the largest countries, investors may not need to spend too much time considering the outcome. The elections may not be free or fair and so unlikely to lead to change (notably the recent election in Russia) or the current government may be highly likely to retain power. In Mexico and India, the current government parties have huge leads in the opinion polls and in Indonesia, the winning candidate was backed by the popular outgoing President. Instead of focusing on elections, we feel investors should spend more time thinking about individual policies as they are implemented and try to look ahead at the wider implications of those policies as they come into force.

What Geopolitical factors have been driving markets?

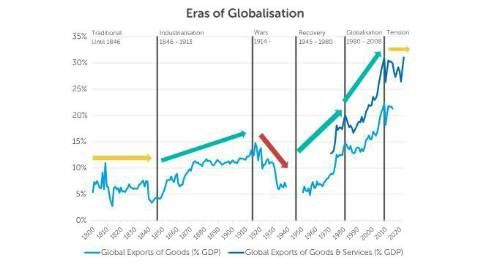

Trade Policy These measures are all part of a global “re-shoring” trend. Countries are looking to bring production back under domestic or allied control, particularly for “strategically important” industries. This has contributed to a stagnation in global trade in recent years. If tensions continue to rise, particularly with China which is the world’s largest exporter, then this trend is likely to continue with potential - albeit contained - implications for global growth and inflation and monetary policy, and on corporate revenues and profits.

Source: Barnett Waddingham, World Bank; Federico & Tena, 2018, "Federico-Tena World Trade Historical Database : Openness"

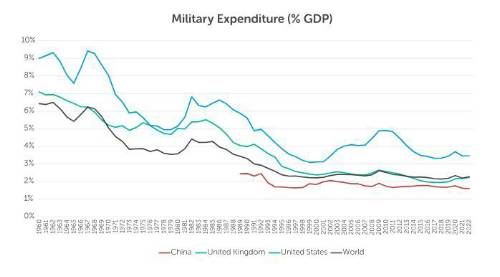

Defence spending

Source: World Bank However, because defence spending has been so low, even a relatively small increase translates into a substantial increase in revenue which is shared between a handful of large aerospace and defence companies. Since the Russian invasion of Ukraine, the FTSE World Aerospace and Defence sector has outperformed the FTSE World Index by 24%. For investors with exclusions from defence industries this is likely to harm returns relative to the overall index; albeit the impact is likely to be modest as the sector makes up only 1.9% of the FTSE World equity index. So even this political act is unlikely to materially drive overall portfolio level returns.

Conclusion This article features contributions from Callum Smith, Senior Research Analyst. |

|

|

|

| Take the lead client-facing projects ... | ||

| Various locations - Negotiable | ||

| Choose Life! Choose a major global co... | ||

| Various locations - Negotiable | ||

| Actuarial skillset? Apply now for Snr... | ||

| South East / hybrid with travel requirements - Negotiable | ||

| Financial Risk Leader - ALM Oversight | ||

| Flex / hybrid - Negotiable | ||

| Be the very model of a modern Capital... | ||

| London - Negotiable | ||

| Pensions Actuary seeking a high-impac... | ||

| London or Scotland / hybrid 3dpw office-based - Negotiable | ||

| Great opportunity for Pensions Actuar... | ||

| London or Scotland / hybrid 3dpw office-based - Negotiable | ||

| Responsible Investing Manager - Clima... | ||

| London/Hybrid - Negotiable | ||

| Quant Strategist | ||

| London/Hybrid - Negotiable | ||

| Multiple remote longevity contracts | ||

| Fully remote - Negotiable | ||

| Multiple remote inflation hedging con... | ||

| Fully remote - Negotiable | ||

| Play a vital role in shaping a new He... | ||

| London or Scotland / hybrid 50/50 - Negotiable | ||

| Support the Longevity team of a globa... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Delve into financial risk within a ma... | ||

| Wales / South West / hybrid 1dpw office-based - Negotiable | ||

| Project-based Life Pricing Actuarial ... | ||

| South West / hybrid 2 dpw office-based - Negotiable | ||

| Pricing Actuary | ||

| London - £120,000 Per Annum | ||

| Develop your career in motor pricing | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Experience real career growth in home... | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Be at the cutting edge of technical p... | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Use your passion for innovation and t... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd