The survey, which captures long-term institutional investment trends by seven main investor groups across ten alternative asset classes, showed that of the top 100 alternative investment managers, real estate managers have the largest share of assets (35% and over $1.4 trillion), followed by private equity fund managers (18% and $695bn), hedge funds (17% and $675bn), private equity funds of funds (PEFoFs) (12% and $492bn), illiquid credit (9% and 360bn), funds of hedge funds (FoHFs) (6% and $228bn), infrastructure (4% and 161bn) and commodities (1%).

In terms of the growth in asset classes among the top 100 asset managers, illiquid credit saw the largest percentage increase over the 12-month period, with AuM rising from $178bn to $360bn. Conversely, assets allocated to direct hedge fund strategies among the top 100 asset managers fell over the period, from $755bn to $675bn.

Luba Nikulina, global head of manager research at Willis Towers Watson, said: “As capital supply and competition have increased in some segments of the illiquid credit universe, such as direct lending for example, yields are not always offering sufficient compensation for illiquidity and risk. At the same time, we have seen some withdrawal of capital from hedge funds in the face of high fees, skewed alignment of interests and performance headwinds. It appears that the growing groundswell of negative sentiment that has arisen due to the aforementioned issues is now showing up in the decisions of asset allocators. We have been surprised it has taken this long to observe the trend turn, however this is aligned with our long-held view that the hedge fund industry needs to change, with those willing to offer greater transparency and display value for money likely to prosper going forward.”

Data for the total alternative investment universe, shows that overall alternative assets under management now stand at just under $6.5 trillion, across 562 entries. North America continues to be the largest destination for alternative asset manager allocations (54%). Overall, 33% of alternative assets are invested in Europe and 8% in Asia Pacific, with 6% invested in the rest of the world.

The research also highlights that, when looking at the distribution of assets within the top 100 alternative asset managers by investor type, pension fund assets represent a third (33%) of assets. This is followed by wealth managers (15%), sovereign wealth funds (5%), endowments & foundations (2%), banks (2%) and funds of funds (2%). Notably, insurance companies’ proportion among the top 100 alternative asset managers grew from 10% to 12% of total manager assets.

“Although the alternative asset manager universe continues to be dominated by pension fund assets, as solutions have continued to evolve that are better aligned to investor needs and incorporate lower cost structures, we have seen growing interest from other investor groups such as insurers looking to lock-in alpha opportunities presented by continued volatility,” said Luba Nikulina.

Pension fund assets managed by the top 100 alternative asset managers now stand at $1.6 trillion, up 9% compared to last year’s study, and represents 51% of their total AuM. Illiquid credit allocations for this group doubled to 8% over the 12 months, whilst real estate managers continue to have the largest share of pension fund assets with 41%. This is followed by private equity FoFs (18%), hedge funds (12%), infrastructure (8%), illiquid credit (8%), private equity (7%) and FoHFs (5%).

“Despite the elevated levels of macro and political concerns, long lease property strategies in Europe have continued to see interest from de-risking pension funds given the expected return differential relative to bonds and higher inflation expectations. We believe this demand is likely to persist as long as bond yields remain low which makes the ability to source attractive assets in this area ever more important,” said Luba Nikulina. “Private equity has also continued to thrive following the period of strong distributions and investors looking for alpha which is becoming more challenging to achieve with the abundance of capital and limited supply of deals contributing to incredibly rich pricing. Investors are now having to find areas of the market that aren’t as expensive or are viewed as contrarian in hopes of achieving successful outcomes.”

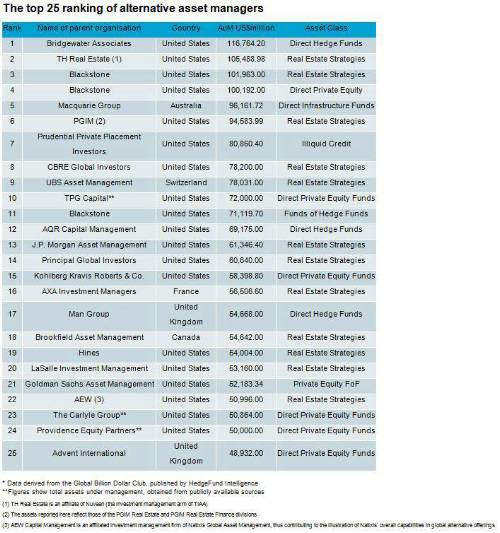

According to the latest data in the research, Bridgewater Associates is the largest manager in terms of overall assets under management, with over $116 billion invested in direct hedge funds. TH Real Estate – an affiliate of Nuveen, the investment management arm of TIAA – is the largest real estate manager globally, overseeing more than $105 billion in assets, whilst Blackstone continues to look after the highest volume of private equity and FoHF assets at just over $100 billion and $71 billion respectively. Prudential Private Placement Investors is the most significant illiquid credit manager with nearly $81 billion under management.

Full report: Willis Towers Watson’s Global Alternatives Survey

|