The MCGPI is a comprehensive study of global pension systems, accounting for two-thirds (65 per cent) of the world’s population. It benchmarks retirement income systems around the world highlighting some shortcomings in each system and suggests possible areas of reform that would provide more adequate and sustainable retirement benefits. The top three systems, all receiving an A-grade, are sustainable and well-governed systems, providing strong benefits to individuals.

The considerable increase in the UK index score was driven by a strong improvement in the adequacy sub-index value – which went from 59.2 in 2020 to 73.9 this year. The impact of auto enrolment, in turn improving the net replacement rate as calculated by the OECD, was the key factor behind this increase. However, there remains room for improvement in areas such as the gender pensions gap and pensions adequacy for lower paid workers.

Tess Page, Partner and Trustee Leader at Mercer, said: “The UK pensions system is in a much improved position from last year. We have benefitted from auto-enrolment pushing up savings rates, as well as mostly helpful policy and regulatory changes.

However, many members still face a cliff edge at retirement and, as ‘generation DC’ approaches pensions age, this issue is only expected to accelerate. There are a number of actions that employers, trustees, and the Government could take to help improve the UK system and deliver better long-term retirement outcomes. A great start would be further increasing auto-enrolment contributions and coverage – notably to better serve those who are self-employed.”

Ms Page added: “One real bright spot of opportunity, as highlighted in our recent survey with the CBI, is the UK’s leadership on managing pension scheme climate change risk. By managing climate risk, it provides a path to sustainable investment returns and helps with scheme member engagement. That said, so far it has been a little too much talk and not enough action. Many pension schemes do not know where to begin, but there are small changes that can be effective such as basic assessments to evaluate what actions will ensure most impact.”

Olivier Fines, CFA, Head of Advocacy EMEA at CFA Institute said: “With the Pension Schemes Act 2015, the UK government aimed to bring more flexibility into the system and permit a redistribution of risk between employers, individual members and intermediary third parties. This was done to allow the system to better cater to people’s needs. However, it has also upped the ante for individuals to take responsibility for their own long-term savings needs and decisions around their benefits. This is where the financial sector has a role to play. Members should expect that the advice they obtain from professionals on such crucial decisions which affect their livelihoods be guided by fiduciary duty and suitability. In 2019, membership of occupational defined contribution schemes in the UK for the first time exceeded that of traditional defined benefit schemes. A tool like the Mercer CFA Institute Global Pension Index can help the industry and policy makers better appreciate the structural and long-term impacts of policy decisions and provide meaningful context for this crucial debate.”

Gender differences in pension outcomes

The MCGPI’s analysis highlighted that there was no single cause of the gender pension gap, despite all regions having significant differences in the level of retirement income across genders. The UK and Denmark have broadly similar employment rates for men and women, but quite different gender pension gaps. The UK’s gender pension gap stands at 40.5% raising some concern about pension design and socio-economic inequality.

While employment issues are major contributors and are well known – more female part-time workers, periods out of the workforce for caring responsibilities and lower average salaries, for example – the study found that pension design flaws were aggravating the issue. This includes non-mandatory accrual of pension benefits during parental leave, absence of pension credits while caring for young children or elderly parents in most systems, and the lack of indexation of pensions during retirement, which have a larger impact on women due to longer life expectancy.

By the numbers

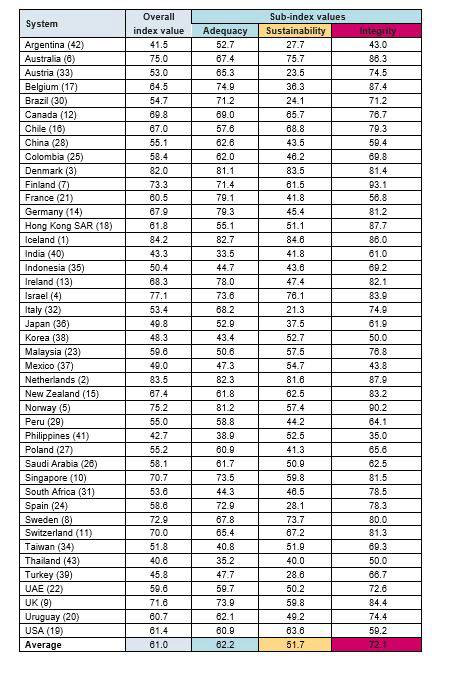

Iceland had the highest overall index value (84.2), closely followed by the Netherlands (83.5). Thailand had the lowest index value (40.6).

The Index uses the weighted average of the sub-indices of adequacy, sustainability and integrity. For each sub-index, the systems with the highest values were Iceland for adequacy (82.7), Iceland for sustainability (84.6) and Finland for integrity (93.1). The systems with the lowest values across the sub-indices were India for adequacy (33.5), Italy for sustainability (21.3) and the Philippines for integrity (35.0).

In comparison to 2020, China and the UK showed the most improvement as a result of significant pension reform, which improved outcomes for individuals and pension regulation.

2021 Mercer CFA Institute Global Pension Index

|