|

|

The group risk industry provided financial support to a record number of families during 2017. Industry data compiled and published by Group Risk Development (GRiD) shows that a total of over £1.6bn was paid out by the group risk industry during 2017, a £120.5 million increase on 2016. 25,906 UK families were helped to avoid financial hardship after the death, illness, accident or disability of a loved one. |

As well as financial payments, group risk insurers help people in many other ways. Julie’s story below gives just one example of how group risk policies provide practical support for policy members. Like Julie, a total of 4,944 people were helped back to work by group risk insurers after a period of sick leave, and a further 7,879 people were assisted by the industry during 2017 through referrals to help and support funded by group risk insurers.

Total benefits paid The average claim amounts (£113,479 for group life; £24,257 p.a. for group income protection; £71,463 for group critical illness) again demonstrate that these are not just benefits for top earners – these benefits throw a vital financial lifeline to people at the worst times, regardless of their salary, age or position. Total claims paid and average new claim amounts

* All values are rounded

Facilitating return to work GRiD has again captured details of the cases where the insurer supported a return to work with active early intervention (such as fast-track access to counselling or physiotherapy, funded by the insurer) before that person was eligible for a monetary payment. 2,989 people (33.1% of all claims submitted, up six percentage points on 2016) were able to go back to work during 2017 because of such early intervention (of which, 52% had help to overcome mental illness and 17% had support overcoming a musculoskeletal condition). On top of this, for the first time, GRiD has also captured details of cases to demonstrate that once a claim is in payment, help and support back to work is still given and people are not forgotten. Of the 5,255 group income protection claims that went into payment during 2016, 1,955 people were helped by the insurer to make a full return to work during that year or during 2017.

Help and support For the first time, GRiD has captured the number of referrals that group risk insurers have made to these services. 7,879 people accessed extra help and support during 2017 following a referral by a group risk insurer. This is in addition to countless self-referrals.

Main cause of claim Main causes of claim across all group risk products

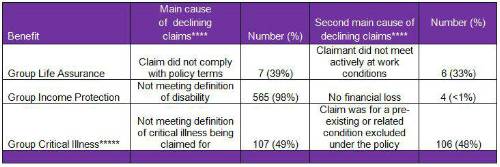

Paying claims Very few claims are declined for group life assurance. For group income protection and group critical illness claims, the numbers declined are higher. A common reason for this is that it can sometimes be difficult for an employer to be sure that the claim an employee wants to make is either genuine or something that is valid under the policy. The advice given to them generally is to submit the claim for the group risk insurer to consider. In these circumstances, the employer can then uphold their role and meet their obligations as the employee’s advocate. Such claims are captured as declined in GRiD’s reporting, even where there would have been no real expectation on the employer’s (and often the employee’s) behalf that the claim would be paid. The table below highlights the main reasons for declining claims across all three group risk products. There is further explanation and detail in the attached FAQs document. Main reasons for declining claims across all group risk products

****Please see attached FAQs document for further explanation

*****There were also 34 notifications where a member requested payment for an illness or condition that was not insured under the policy.

Katharine Moxham, spokesperson for GRiD, commented: “Once again, it’s great to be able to show how employer-sponsored group risk protection benefits support people through some really difficult times through a financial pay-out as well as in other ways. “GRiD’s latest employer research cites the key reasons why employers provide group risk benefits. These include helping with recruitment and retention/differentiating their company, being able to recoup the costs in improved productivity and team morale, and paternalism. “Enlightened employers see exactly how group risk benefits and their inherent additional services help with engagement and productivity, support employee wellbeing and enable a business to fulfil its duty of care. They also ensure fair and consistent treatment of people, and can put businesses in a prime position to comply with their role in the Government’s ambitions for healthier and more inclusive workforces. “One size doesn’t fit all – people’s needs are met when they are treated as individuals. These figures illustrate the very real difference that group risk protection products make to peoples’ lives day in and day out.”

Please also see the accompanying FAQs document. |

|

|

|

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Head of Capital | ||

| London - Negotiable | ||

| Portfolio Actuary | ||

| London - £140,000 Per Annum | ||

| Deputy Head of Capital | ||

| London - £140,000 Per Annum | ||

| Senior Pricing & Portfolio Management... | ||

| London - £150,000 Per Annum | ||

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Lead Capital Actuary | ||

| London - £150,000 Per Annum | ||

| Take the lead on capital oversight | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Be at the forefront of creative GI co... | ||

| London/hybrid 2-3dpw office-based - Negotiable | ||

| Remote Market and Credit Risk Calibra... | ||

| Remote - Negotiable | ||

| Contact us about a Capital Contract i... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Head of Insurance Risk | ||

| London - £160,000 Per Annum | ||

| Director - Pensions Risk Transfer (PRT) | ||

| London, Midlands, North West - hybrid working 2dpw in the office - Negotiable | ||

| Dip a toe into public sector work wit... | ||

| Flex / hybrid 2 days p/w office-based - Negotiable | ||

| P&C Consultant | ||

| London / hybrid 3dpw office-based - Negotiable | ||

| Take the lead client-facing projects ... | ||

| Various locations - Negotiable | ||

| Choose Life! Choose a major global co... | ||

| Various locations - Negotiable | ||

| Actuarial skillset? Apply now for Snr... | ||

| South East / hybrid with travel requirements - Negotiable | ||

| Financial Risk Leader - ALM Oversight | ||

| Flex / hybrid - Negotiable | ||

| Be the very model of a modern Capital... | ||

| London - Negotiable | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd