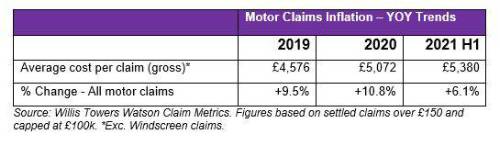

The H1 2021 figure compares to an inflation rise of 10.8% during the full year 2020.

Accidental Damage (AD) has increased at the fastest rate over the last 18 months, with AD claims inflation rising by 8.2% during H1 2021 and by 8.4% in 2020, according to the data from Claim Metrics, which provides deep analysis of claims activity in the personal lines insurance market, benchmarking over £17 billion of motor claims spend and more than 40% of the UK motor market.

Tom Helm, Head of Claims Consulting, Willis Towers Watson, said: “The cost of settling claims continues to climb despite driving behaviour changing dramatically during the pandemic. The second quarter in 2020 saw the greatest impact from lockdown with a substantial change in the types of accidents arising. The proportion of claims that were hit-in-rear accidents fell sharply by seven percentage points, despite previously accounting for about 21% of all UK claims. Meanwhile, cyclist claims, which are typically more costly but low in volume, more than doubled their normal share of the overall claim numbers in the same period.

“Understanding this change in mix of claims types during the lockdowns is important because, whilst overall accident frequency was down, an increase in the proportion of higher-severity claim types, like accidents with cyclists, has been a key driver behind the latest increase in average claims cost. It also means we cannot solely rely on assumptions and patterns of the past to forecast future claims outcomes. Tracking whether this mix fully readjusts in the second half of 2021, as driving levels return to 90% of pre-pandemic levels, will be vital.”

The data also shows a wide variance in the rate of claims inflation between UK regions, with a difference of seven percentage points between the fastest and slowest increasing regions, with London leading the way at 9.9%.

Tom Helm said: “Claims inflation has the potential to rise further in 2022 driven by a combination of factors, including widespread supply chain issues affecting manyindustries such as automotive repairs. With inflationary pressures expected to intensify further due to rising used car prices impacting total loss settlement costs, the impact of the Whiplash Reforms should be closely monitored for early signs of the measures’ ability at least partially to offset this rise in vehicle damage costs.

“Add into the mix the fact that there will be increased volatility of motor premiums in the New Year owing to FCA pricing reforms and that remote working continues to impact claims patterns, the trading environment will remain fraught with uncertainties for insurers. Increasing customer expectations, spurred by the rise of digital-first competitors, continue to disrupt the market, which means efficiency and improving claims handling accuracy will prove decisive in such conditions.”

(1) Claim Metrics data is based on claims between £150 (£500 PI) and £100,000, excluding windscreen claims.

|