By Reena Tanna, FIA, Principal and Senior Investment Consultant and Mark Futcher, Partner and Head of DC at Barnett Waddingham

While the concept of using a DB surplus in this way is not new, the regulatory push over the past decade towards DC consolidation in larger Master Trusts has complicated this process for many schemes.

Here, we’ll share some insights gathered whilst acting as a lead investment consultant for two clients who have implemented innovative solutions to get around this issue, which enables them to successfully utilise their DB surpluses to fund contributions for their DC schemes.

The benefits of using your DB surplus to fund DC contributions

You may be wondering why you would do this rather than just refund the surplus directly to the Employer and give them the flexibility on how to use this. After all, using the surplus to pay for DC contributions is akin to a refund to the Employer. The answer is partly that this is a tax efficient approach, that is often more straightforward to implement than a direct refund.

In addition, who ‘owns’ a pension surplus and how any surplus is used is a highly emotive issue for some stakeholders. As such, the way surplus decisions are perceived matters. Whilst a refund of a surplus directly to an Employer may feel a little ‘dirty’ to some, there appears to be less reluctance on using it to fund DC contributions.

This may be because it appears more paternalistic and less political as the money is still being spent on pension benefits. This is especially likely to be the case if some of the surplus is used to give DC members a benefits top-up, as opposed to being used to purely pre-fund future commitments.

How does it work in practice?

If there is already a DC arrangement within the same Trust as the DB Scheme then, mechanistically, this is straightforward. Though you should still check your trust deed and rules on any wording around use of surplus – you need to make sure there aren’t any hurdles from the get-go.

What happens if you have decided that your DC scheme would benefit from moving to Master Trust?

You could still move the assets and use the surplus. The surplus would be paid to the Master Trust provider who would then use it to pay contributions.

"Things to consider with this approach would be agreeing a guarantee with the Provider which would allow the surplus to be transferred, if the company decided later that they wanted to switch to another Master Trust. There might be a variety of reasons for this, including poor performance or lagging the rest of market on technological developments. An agreement on who benefits or bares the risks of the invested surplus will also need to be determined upfront."

If the surplus at outset covers a short period, say one to two years, then the points raised above will be less significant.

Is there a way to benefit from a Master Trust offering without transferring the surplus?

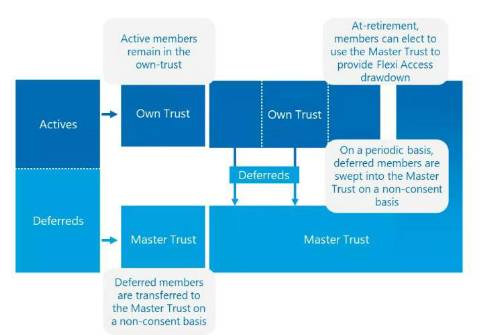

Yes - you maintain the existing, or set up a new, own-trust DC section alongside having a Master Trust. We helped a UK-based FTSE 250 service sector public limited company (PLC) set up a DC structure which allows them to use their DB surplus to pay for DC contributions. They currently project the DB surplus will fund DC contributions for around 15 years.

The DB surplus will be used to fund the DC contributions for active members within the own-trust DC section. Deferred DC members are moved to the Master Trust on a regular basis and the design also provides a seamless journey for those at retirement if they wish to drawdown benefits, since they can stay invested in the same assets before and after retirement – win: win.

For those looking to stay invested at retirement this also avoids:

high retail market fees;

transactions costs; and

out of market exposure.

For our client, this meant using the Master Trust Providers investment strategy for members pre and post-retirement to ensure there is no risk of devaluation to the members fund value as they transfer their assets from own-trust to the Master Trust.

The overall structure is set out below:

What if you want to maintain control of your investment strategy?

The trustee and company can work together to design their own investment strategy by setting up a bespoke section with the Master Trust, though the ability to do this will depend on the Master Trust’s appetite. Other than the investment strategy, it would operate in the same way as described above.

A separate client, a Standard and Poor’s (S&P) 500 consumer goods multi-national, who wanted to retain control of their investment strategy, has set-up such an arrangement. In this particular instance, the client was nervous about the pace at which illiquid assets would likely be included in the strategy, following the launch of a number of Long-Term Asset Funds (LTAFs) and the signing of the Mansion House compact by most providers. There were also some concerns around how environmental, social and governance (ESG) would be implemented.

Whilst the trustee and company are looking to align with the Master Trust investment strategy, this approach affords them flexibility to change the investments where it doesn’t align with their investment beliefs.

Are these considerations still relevant in light of the DWP’s recent consultation to remove barriers to surplus extraction?

I think so - not only may the ‘optics’ of using surpluses in this way be better, but this approach may also potentially sidestep tricky surplus powers that may remain even after any new legislation is introduced.

Let’s also not forget there are no guarantees on what might come down the line in terms of regulation; the outlook is even more uncertain given the likelihood of a change in government later this year. New legislation will also inevitably take time to implement, whereas many schemes are in the position of needing to decide how they are going to use their surplus now.

|