By Martin Hooper, FIA, Associate at Barnett Waddingham

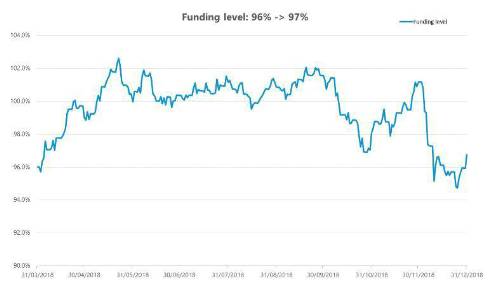

The position was looking much more favourable at the end of November but a sharp fall equity markets and a reduction in corporate bond yields pushing up liabilities wiped out most of those gains during December.

What will happen in the run up to “Brexit”?

The UK is currently due to leave the EU on 29 March, which is the last working day before 31 March. Market conditions and asset valuations at this date will be used to determine assets and liability values for IAS19 valuations. It is possible that markets will be volatile in the run-up date, particularly if negotiations on agreeing a deal run right up to the deadline. It is also unclear whether such volatility will result in the position being better or worse at the year end. Much will depend on how much exposure schemes have to equity markets, overseas markets and how well hedged the funding position is against movements in expected future interest and inflation rates.

It will be difficult for companies to take any definitive action to mitigate against the potential volatility at this stage but they should ensure they understand what impact significant market movements could have on their IAS19 position if the accounting position is a material concern.

GMP equalisation – we now have some clarity

The judgement in the Lloyds Bank case confirmed that UK schemes with GMP liabilities accrued between 17 May 1990 and 5 April 1997 will almost certainly need to recalculate and increase benefits for many scheme members. The emerging trend is for the expected cost of doing so to be recognised in profit and loss for the period covering the date of the judgement 26 October 2018. Our understanding is that most major audit firms are likely to insist on this treatment unless it can be clearly demonstrated that the IAS19 already included a realistic provision for the cost of GMP equalisation.

Where companies have not already done so they should engage with their advisers to understand the expected impact and the extent to which there are any options available to mitigate the impact on the year-end figures. Our experience so far is that the cost will lie somewhere in the range of 0% to 3% of the overall scheme liabilities but it is highly dependent on the scheme demographics and benefits structure.

|