Canada Life is calling on the Treasury to increase the Money Purchase Annual Allowance (MPAA) in the forthcoming Spring Budget. The MPAA effectively restricts future pension savings where someone has flexibly accessed their pension, removing the benefit of tax relief on annual contributions of more than £4,000.

The pension provider has submitted a paper to the Treasury, setting out the arguments for a review of the current threshold. Canada Life proposes restoring the MPAA to £10,000, which was the original allowance in 2015 before it was cut in 2017 to just £4,000.

The company argues the current low limit penalises and discourages older workers who have taken time out from employment, drawn on their pensions and wish to resume saving for retirement. This change would also help those who have accessed their pension pot at relatively young ages, for example 55-60, to pay off expensive debt, cope with the current cost-of-living crisis, or to tide people over who have been made redundant.

Lindsey Rix, Canada Life’s UK CEO said: “Increasing the MPAA back to £10,000 would help strengthen the UK economy and boost the retirement provision of the hundreds of thousands of workers who left employment during the pandemic. We believe this is a measure which would positively impact people of all social and economic backgrounds. It would help encourage a return of older experienced staff for many businesses, large or small, and whichever sector they operate in. And it will align well with other Government policy initiatives, such as the mid-life MOT and auto enrolment.

“Any modest cost to the Exchequer from the higher allowance could be more than offset through increased tax revenues. Even a modest boost to employment would result in higher income tax revenues, as well as downstream tax revenues such as higher VAT from increased spending.”

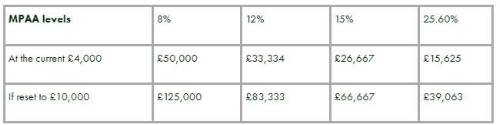

As the table below illustrates, someone in their 50s joining a good defined contribution pension scheme, only needs to be earning above £26,667 to fall foul of the MPAA. These contribution levels include both employee contributions, employer contributions and tax relief:

Salary levels at which the MPAA is relevant, for different MPAA levels and contribution rates

Source: Canada Life. 8% is the default auto-enrolment contribution rate. 12% is the minimum required for the Pension Quality Mark. 15% is the rate required for the Pension Quality Mark+. 25.6% is the average contribution rate for a private sector defined benefit pension scheme.

How many people are affected?

Canada Life estimates between 500,000 and 1 million people in the UK of working age are now restricted by the MPAA. This is based on the numbers who have used the pension freedoms and the fluctuations in employment patterns over the course of the pandemic.

Since the MPAA was cut in 2017, the world has become a very different place; The UK has left the EU, suffered the worst pandemic in over 100 years, seen war in Europe and suffering a cost-of-living crisis, with rising inflation and fuel bills. Canada Life contends a policy intended to target only higher earners making lifestyle choices and not those forced to draw in their pensions due to unforeseen circumstances, is now penalising hundreds of thousands of ordinary workers.

How much would it cost?

The cost to the Treasury of changing the MPAA back to £10,000 is very modest relative to the potential benefits. Clearing this obstacle to employment for hundreds of thousands of older workers would cost around £75 million a year, according to the original Treasury impact assessment. By comparison, getting an extra 100,000 people back into employment on an average wage of £30,000 a year, would generate income tax revenues alone of £400 million.

|