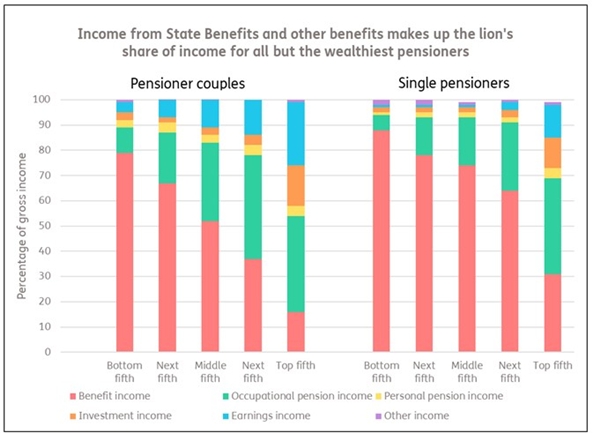

Stephen Lowe, group communications director at Just Group, commented: “The data shows that the average pensioner was no better off in 2023/34 than they have been for most of the last 10 years. Pensioner couples have seen gross incomes flatline over that period while single pensioners have seen a modest 5% rise. During that time the contribution of State Pension and other benefits to overall income has increased a little for couples but remained flat for singles. Half (50%) of pensioners are in the top half of the overall population income distribution which is about the same as a decade ago, but compares to 38% in 1995. The State Pension and other benefits continue to be the bedrock of retirement finances, making up 37% of gross income for pensioner couples and 56% for pensioner singles. In fact, more than half of pensioner couples and four fifths of singles receive more than half of their income from the State (see chart below). The figures reinforce the message that building up private pension is the key to having a better standard of living later in life. It also underlines the importance of people approaching retirement to think carefully about how to generate a sustainable income, taking regulated advice and making use of resources such as the government’s free, independent and impartial guidance service Pension Wise will help.”

Mike Ambery, Retirement Savings Director at Standard Life, part of Phoenix Group said: “Pensioners continue to draw on a range of income sources in retirement, making the task of managing their retirement finances more complex than ever. The latest data from the Pensioners’ Income Series1 shows that almost three quarters (70%) of pensioners rely on income from a private pension, and almost two thirds (61%) receive income from investments, however for the 90% of those not in receipt of financial advice, this puts the onus firmly on them to manage this income and any tax implications. There is also continued dependence on secure income sources like the state pension, with benefit income (which includes the state pension) the largest component of total gross income, making up 56% for single pensioners and 37% for pensioner couples. This reliance is more pronounced for older pensioners, who have lower average incomes that younger pensioners, thus making them even more reliant on the state pension. With defined benefit schemes in steady decline and defined contribution schemes set to take over in the coming years, the need for a more diverse range of retirement income solutions to help people maximise their DC pension savings has never been greater. The good news is that the FCA’s Retirement Income Advice review has put individuals’ retirement income needs front and centre, and has led to increasing recognition around how a mix of income solutions is often the best way to ensure these needs are met. Having an element of guaranteed income can play an important role, providing certainty and security that essential spending is met, while keeping some savings accessible and used for growth – such as in a smoothed managed fund which helps dampen the impact of day-to-day market fluctuations – can provide the flexibility and potential growth that individuals also seek. However ensuring good outcomes at retirement remains one of the big challenges faced by the pensions industry, and we must go further to help the 90% of consumers who can’t or don’t seek financial advice. The use of guided defaults could help individuals move towards appropriate solutions that align with their financial circumstances, while giving providers more flexibility to offer targeted support would ensure retirees are better equipped to make informed decisions. Furthermore, as people face the challenge of balancing secure income with growth potential, it is vital that the industry continues to innovate and offer products that combine both flexibility and guaranteed income. The industry has been responding in earnest with new retirement income products being brought to market, and this innovation must be encouraged as we continue to navigate the UK’s evolving retirement landscape.”

Carolyn Jones, Retirement Director at Scottish Widows, commented: "While the DWP’s update shows signs of improvement among certain groups of retirees, such as the narrowing between single female and male pensioners, who now have just £14 difference in average weekly incomes, there are still larger affordability concerns at play given today’s high-cost climate. It is troubling that although pensioners’ average weekly incomes have doubled since 1995 - this growth has plateaued over the last 15 years - and in doing so comes up short against the higher cost demands on today’s current and soon-to-be retirees. Our latest Retirement Report predicts 38% of people are not on track for even a minimum retirement lifestyle. Driving increased productivity and real wage growth will be key to creating more headroom for people to be able to actively save and increase their pension contributions earlier in their careers. We also believe that a Lifetime Savings Commission should be established to consider the challenges of retirement savings (pensions, other savings, other investments, other forms of income), the role of housing and the need to build financial resilience. For those approaching retirement, to combat the tougher retirement climate, planning early is vital as well as regularly evaluating your current pot to ensure it is working its hardest. Knowing exactly how much money you have, and therefore any shortfall you need to make up, can be hugely empowering and motivating for the future.”

DWP Pensioner Income Series Report

|