• Disaster risks are increasing but insurance hasn't kept pace: the estimated USD 1.3 trillion On average, over the last 10 years, only 30% of catastrophe losses were covered by insurance and the remaining 70%, or around USD 1.3 trillion, were paid by individuals, firms and governments. gap between insured and total losses remains stubbornly large, hampering a country's ability to recover

• Governments are uniquely exposed as they typically shoulder the cost of relief and recovery and also pay for reconstruction of infrastructure

• Uninsured losses following a catastrophe impact economic growth over several years, hampering a country's ability to bounce back

• Innovative insurance solutions can help countries, cities and individuals preserve hard-won development gains, even in the face of major natural disasters and climate change but it's crucial to arrange them before disaster strikes

• Governments increasingly use these solutions to manage their budgets and fiscal contingencies; successful examples can be found in many emerging markets as well as in OECD countries but more needs to be done

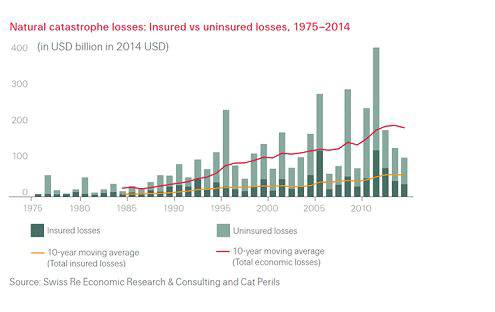

In "Disaster risk financing: Smart solutions for the public sector" Swiss Re shows that the economic cost of natural catastrophes has grown markedly in the last 40 years. The protection gap – the difference between economic and insured losses – remains large despite the availability of innovative insurance solutions. Narrowing this gap helps strengthening a country's financial resilience.

"The insurance industry is already rising to the challenge of underinsurance in both developed and developing countries through innovative risk management measures," said Swiss Re's Group Chief Executive Officer Michel M. Liès. "The risk landscape is becoming more and more complex as the world becomes more interdependent. No country can afford to be left unprotected."

On average only about 30% of catastrophe losses have been covered by insurance over the last 10 years. That means that about 70% of catastrophe losses – or USD 1.3 trillion – have been borne by individuals, firms and governments.

Governments typically shoulder the cost of relief and recovery, but also pay for reconstruction of infrastructure and, in the case of underinsured individuals or businesses, they even fund private rebuilding efforts. Yet, most governments will seek the funds only after a catastrophic event, and often revert to increasing taxes, borrowing or soliciting international aid, often incurring high costs and delays. These events can wipe out years of hard-earned development gains. Rating agency Standard & Poor's recently published a report warning that a country's disaster preparedness could be linked to its credit rating going forward.

More needs to be done

As a first priority, governments should enable a functioning insurance market. This will help absorb a major part of disaster losses suffered by individuals and businesses. Pre-event financing solutions can alleviate the remaining financial burden on governments. Post-disaster financing (such as debt financing or donor aid) should only come into play to cover residual losses once all other risk transfer solutions have been exhausted.

"For risk protection to be effective, funds need to be quickly available in the wake of a natural catastrophe, meaning that financing arrangements must be in place already beforehand," says Martyn Parker, Chairman of Swiss Re's Global Partnerships, a unit that works with public sector clients. "Financial preparedness lowers the volatility of the state budget and improves planning certainty for the public sector, besides making a country more attractive to investors."

The study – launched at the World Bank /IMF annual meetings in Lima – points to a number of countries working in collaboration with insurers to innovative solutions. Mexico, for example, is a pioneer in securitising earthquake and hurricane risk. Uruguay has developed an ingenious risk transfer mechanism to mitigate the risk of low rainfall on its hydroelectric power generation. Central American and Caribbean governments have insured their risk against hurricanes and earthquakes The Africa Risk Capacity insures several countries against drought risk.

The publication also highlights activities in Thailand, Bangladesh and Africa, with more updates to be published on swissre.com over the next months

|