While Hurricane Ida was the costliest natural disaster in 2021, winter storm Uri and other secondary peril events caused more than half of total losses as wealth accumulation and climate change effects in disaster-prone areas drive claims. Man-made disasters triggered another USD 7 billion of insured losses, resulting in estimated global insured losses of USD 112 billion in 2021.

”In 2021, insured losses from natural disasters again exceeded the previous ten-year average, continuing the trend of an annual 5–6% rise in losses seen in recent decades. It seems to have become the norm that at least one secondary peril event such as a severe flooding, winter storm or wildfire, each year results in losses of more than USD 10 billion. At the same time, Hurricane Ida is a stark reminder of the threat and loss potential of peak perils. Just one such event hitting densely populated areas can strongly impact the annual losses,” said Martin Bertogg, Head of Cat Perils at Swiss Re.

The two costliest natural disasters of the year were both recorded in the US. Hurricane Ida wreaked USD 30 – 32 billion in estimated insured damages,including flooding in New York, and winter storm Uri caused USD billion in insured losses. Uri brought extreme cold, heavy snowfall and ice accumulation, especially in Texas where the power grid experienced multiple failures on account of freezing conditions. The costliest event in Europe meanwhile was the July flooding in Germany, Belgium and nearby countries, causing up to USD 13 billion in insured losses, in comparison with economic losses of above USD 40 billion. This indicates a still very large flood protection gap in Europe. The flooding was the costliest natural disaster for the region since 1970 and also the world's second highest, after the 2011 Thailand flood.

”The impact of the natural disasters we have experienced this year once again highlights the need for significant investment in strengthening critical infrastructure to mitigate the impact of extreme weather conditions,” said Jérôme Jean Haegeli, Swiss Re's Group Chief Economist. ”Investments in infrastructure support sustainable growth and resilience and need to be upscaled. In the US alone, the infrastructure investment gap to maintain critical and aging infrastructure is USD 500 billion on average per year until 2040. Partnering with the public sector, the insurance industry is critical for strengthening society's resilience to climate risks, by investing in and underwriting sustainable infrastructure.”

Further devastating secondary peril activity in Europe included severe convective storms in June, with thunderstorms, hail and tornadoes causing widespread damage to property in Germany, Belgium, the Netherlands, Czech Republic and Switzerland. The resulting insured losses are estimated at USD 4.5 billion. Elsewhere in the world, there were severe flooding events in China's Henan province and British Columbia in Canada, among others.

On the other end of the extreme weather spectrum, Canada, adjacent parts of the US and many parts of the Mediterranean experienced record temperatures in 2021. During the last days of June, a "heat dome" set a new all-time Canadian temperature record of nearly 50°C in a village in British Columbia. Temperatures in the Death Valley, California reached 54.4°C during one of multiple heatwaves in the southwest. The exceptional heat was often accompanied by devastating wildfires. However, the associated insured losses were lower than in recent years, when the fires affected more populated areas. In California, wildfires destroyed in particular large forest areas but in contrast to 2017, 2018 and 2020, encroached on areas of lower property concentration.

These sigma catastrophe loss estimates are for property damage and exclude claims related to COVID-19. Loss estimates in this media release are preliminary and are subject to change as not all loss-generating events have been fully assessed yet. For example, catastrophe activity in December has remained elevated and resulting losses are still being assessed. COVID-19 has elongated the claims lifecycle, particularly for large events, and it will take considerably longer than normal to assess the final tally.

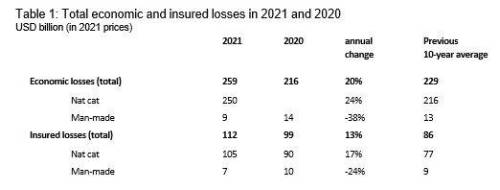

Note: Due to rounding, some totals may not correspond with the sum of the separate figures.

Source: Swiss Re Institute

|