|

|

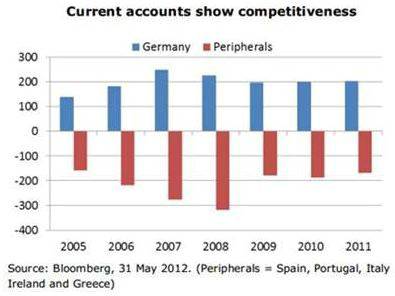

John Greenwood, Chief Economist at Invesco Ltd Eurozone Crisis Q: Would it be a financial disaster if Greece and others left the euro? What would be the catalyst for an exit? How would it work? How would a new currency be produced overnight? A: Whatever course Greece takes, it is going to be very painful and very costly. They can either remain in the euro, in which case they are going to have years of recession - virtually depression - and high unemployment in an attempt, basically, to reduce their internal cost structure. That is very difficult to do, so the cost of that should not be underestimated. On the other hand, if they quit, they could introduce a new currency, they could renege on a lot of their external debt, and they could restore competitiveness and growth. That has a lot to be said for it and it may even turn out to be the case after two or three more failures of these restructuring programmes. The roadmap for that kind of exit has been quite well mapped out. There have been no less than 67 exits from monetary unions since the Second World War. Admittedly, not all of them have occurred during a debt crisis, but a good example is the way in which Slovakia separated from the Czech Republic in 1994 - and this is on the mechanics of what would happen. They passed a law on the Friday evening, essentially saying that, from Monday morning, all domestic contracts and bank deposits would be redenominated in Slovak crowns as opposed to Czechoslovak crowns. They called in banknotes and over-stamped them, and that could be done. Basically, the new system started out on a one-to-one basis on the Monday or the Tuesday morning. After a while, the currency started to depreciate, which gave Slovakia much more competitiveness, and it would be the same in the case of Greece. Q: Could it be replicated in exactly the same way? Would the consequences for the monetary union not be much more difficult to deal with than in the case of Czechoslovakia? A: Yes, there would be spill-over effects. The main risk is contagion: that is that, immediately Greece or any other country left the eurozone, there would be fears about other countries leaving, which, in turn, would precipitate either bank runs or fears of devaluation in those other countries. Along with that kind of exit, I think that would force the ECB and the other authorities to impose some degree of capital controls or of what they did in Argentina - a corralito; that is, controls on deposit withdrawals in the affected countries, which would, essentially, be the other southern European economies. This is not something that is to be taken lightheartedly, but, if the rest of the union was to be preserved, something like that would have to be done. Q: Given the extent of the debt which is held within Spain and Italy, is there enough of a firewall within the eurozone? A: It is a topical question because, just this morning, Italy's sovereign debt has been downgraded by two notches by Moody's. Italian sovereign debt is of the order of €2 trillion; Spanish sovereign debt is €0.8 trillion; the size of the firewall is a mere €700 billion, so only 25%of just those two countries. The fact of the matter is that the ESM (European Stability Mechanism) - the rescue fund - is a poor substitute for a full federal fiscal union. That is really the core of the problem and, until the eurozone moves to something much more credible, like a full fiscal union, there are going to continue to be doubts over the sustainability of these incremental programmes that have been put in place so far. Q: I do not see that the straitjacket of tight fiscal union would help the eurozone, because of the political consequences between the member nations. How can those things be reconciled? A: I do not think they can be reconciled. Look at the United Kingdom: we have a fiscal union between England and Wales, Scotland and Northern Ireland, and a monetary union which envelops exactly the same group, so there is a match between the fiscal union and the monetary union, and it is exactly the same in the United States. The point is that, at the end of the day, if people are afraid about their money in the banks, they can rely on deposit insurance and on deposit withdrawals, but, if, at the end of the day, all of those fail, there is only one thing to support those deposits, which is for the government to step in. In the eurozone, there is no federal European government to step in. European depositors, at the end of the day, are dependent on individual member states that are already over-indebted, so the mechanism is not going to work. Q: Are the underlying problems facing the eurozone about sovereign debt or is the real issue about the competitiveness of southern Europe? A: The eurozone debt crisis seems to keep changing shape; it started out as a housing crisis in Spain and Ireland, then transformed into a sovereign-debt crisis, and has recently become a Spanish banking crisis. Fundamentally, however, all these are symptoms of an underlying problem, which is the combination of inadequate savings right across Europe combined with pre-emptive use or spending of those savings by hungry governments - excessively large welfare states. In that circumstance, what needs to happen is that savings rates need to rise because, at the end of the day, growth and investment can only be financed out of savings. At the moment, with governments across Europe running very large budget deficits, gross national savings are not being built up again, so we need to close those deficits in order to rebuild savings in order to start growing again.

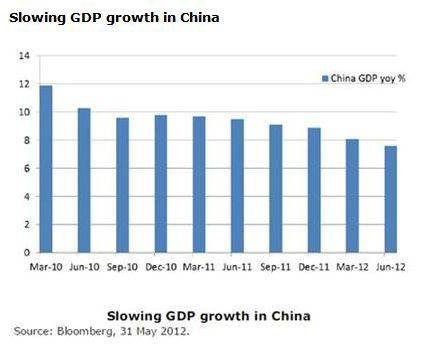

Q: Do austerity programmes work? Can they restore competitiveness and stimulate growth? If that is the case, how does it work? A: There have been very few cases where austerity on its own has worked. If you look at the typical IMF programme for rescuing emerging markets in the last two or three decades, they have always combined a temporary loan to enable the country to remain current on its debt, a restructuring programme of the kind that we are seeing across many countries of southern Europe, combined with - and this is the bit that is missing - devaluation of the currency to kick-start growth. It is also true, if you look at the major countries like Japan, the UK and the US in the 1930s: the way they got out of that depression was through Britain and Japan coming off the gold standard - i.e. devaluing their currency - and then the dollar being devalued from 1934 onwards. You need a combination of those things. The only place recently that has succeeded with internal deflation alone is the case of Hong Kong after the Asian crisis of 1997-98. All the other countries across Asia had, basically, devalued; Hong Kong did not devalue. In the Hong Kong case, it took six years, from 1998 to 2004, with price declines of 16-17% and real wage declines, to get a recovery. In Europe, it would take much longer, and the question is really whether European political and social systems have what it takes to withstand that sort of adjustment. I do not think they do. Q: Do you derive any help from the example of Ireland, which seems to be getting through its austerity period with a degree of success. A: Ireland has a very flexible labour market - flexible in two senses: it is Anglo-Saxon in the sense that wages and prices have been very adjustable, but we also see quite a bit of emigration, so labour mobility is an important part of that, and that is singularly lacking in large parts of Europe, which makes the adjustment problem more difficult. Q: What is your opinion on the attractions of a split currency within the eurozone? Can there be economic adjustment between north and south eurozone countries without exchange-rate adjustment? A: I simply do not think that a southern-zone euro is credible at all. They lack the fiscal discipline, for a start, so combining a lot of countries with very poor fiscal backgrounds and very high debt is just not going to be credible. I do not think that is even a starter. Could Germany leave and leave the rest to themselves? I think there would then be broad breakup if that happened, and I do not think the Germans want to do that in any case. I think that Germany and other core countries are committed to remaining within a broad eurozone, but one or two of the southern peripheral countries will ultimately exit. Q: Do you believe that Eurobonds - i.e. bonds with thebacking of all eurozone governments - would be a cheap and effective way of funding public-sector deficits, in order to at least buy some time? A: The problem with Eurobonds is that, without the ability of a government backing them to raise revenues through taxation and to control expenditures, they really would not be credible. You cannot create bonds in isolation; they need an entity - a company or a country - underlying them to generate the revenues to, first of all, pay the coupons and then to repay the principal. Without that, I just do not think Eurobonds would be credible. What that means is that, in effect, you need a full fiscal union to ensure that Eurobonds are going to be credible. Q: So the real option for survival of the euro is full fiscal union, but, in practice, that seems quite remote, so does that imply that you expect things simply to stutter on for an indefinite period? A: Broadly, yes. I think there is no short-term fix or short-term solution. Gradually, the leaders are getting the message, and we saw, at the last summit in Brussels, a commitment to, for instance, a banking union. These are small steps along the way to greater fiscal union. The system started with a customs union and it moved on to an economics union and now a monetary union, and the leaders have always said that, ultimately, they are looking for political union. Now, however, we are starting to see that, without a fiscal union, the monetary union simply cannot stand up. Q: Do you think recent proposed changes to EU banking will solve the banking crisis? A: No, I do not, and let me illustrate that in a slightly different way. One of the proposals underlying the banking union is that there should be common deposit insurance across Europe, and common banking supervision, but, in order to have common deposit insurance, you have to have a common fund, so that means a mutualisation of debt right across the eurozone; in effect, another step towards a fiscal union. Fiscal union, then, is the ultimate goal, but to get there requires a lot of countries to give up a considerable degree of individual sovereignty and, so far, the member states are not prepared to do that. Until member states agree to commit to that, I think we will still see the monetary union stuttering along. Q: A wholesale bailout of southern Europe would create a massive strain on the public finances of the north of the eurozone, so, surely, the only answer is a series of piecemeal compromises to minimise the shock. Why do the markets not embrace Merkelism? A: Merkelism is fine in theory: that is, slow, progressive adjustment to an ultimate goal. The problem, however, is that the markets do not have the patience to wait. Markets, in a sense, are not social arrangements that can be manipulated, massaged and steered in one direction or another; they are, basically, mechanisms. The two extreme or what we call ‘corner' solutions to this problem are either breakup - exits of some countries - or a full fiscal union. What we are seeing in the markets is that the system is being driven to one of those two solutions. Merkelism, or gradual, incremental change, might work if countries were in a strong position, but they are not. They are in weak positions and, in the meantime, they have a lot of adjustment to do. Their prices and wages etc are too high and have to come down. As I said earlier, we have to see years of internal deflation for that to be successful. Q: How and when are the eurozone problems going to end? Will the market lose patience with the missed deadlines? A: In my view, there are two ways in which this problem is going to be forced to a quicker solution than might otherwise occur under Merkelism: there will be election results, either in the north or in the south, which pre-empt middle-of-the-road political views, and we just missed that in Greece. If we had had the extreme Syriza party elected, they might have opted for an exit. We could, however, next summer or in a few years' time, easily have a more radical party come to power in northern Europe. You would have bailout fatigue in the north or austerity fatigue in the south - one of those two things will happen. That is one set of mechanisms. The other mechanism that could come into force and accelerate any solution is a worsening of the bank runs in southern Europe. We are already having a silent run on the banks. If that accelerates and worsens, that will precipitate a crisis and, I think, at the same time that one or more country exits, that will force a fiscal union on the rest of the countries in order to rescue the banks. Stuttering along making small compromises is where we are at the moment. I think that markets will push things further than the politicians want to go. China Q: Have the Chinese authorities engineered the economic slowdown or is it something we should be concerned about? A: There are two parts to the Chinese economic slowdown: there is a domestic slowdown, which is engineered and deliberate, and then there is an external slowdown - the slowdown of exports - which is involuntary. Basically, China made the mistake of injecting too much money and credit in 2009-10, and they are still suffering from that: property prices are still very high; they have at last got inflation under control but they do not want to release that genie out of the bottle again, so they are going to keep a lid on things domestically. In terms of the external side, with the slowdown in Europe and in the United States, there is very little they can do, but, because they have built an export-oriented economy, they are very vulnerable to it.

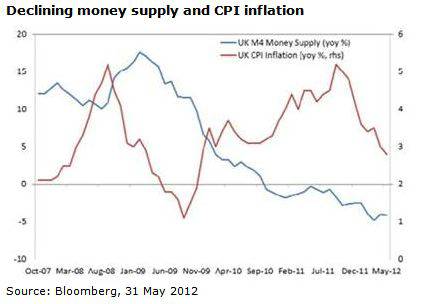

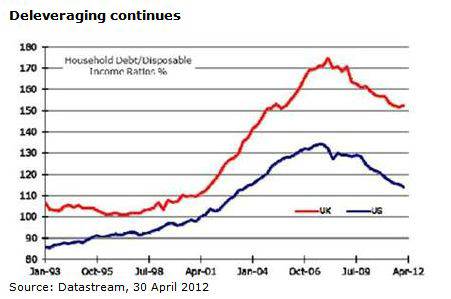

Q: We have seen some new figures this morning which suggest that China's growth has slowed down to a shameful 7.5%. Is that very significant or is it, as some of the commentators are saying, pretty much within the range of expectation? A: It was widely expected. The figure was 7.6% and, on an annualised basis, it was an improvement over the first quarter. The improvements came from the primary sector - agriculture - and from the tertiary sector; it was only the manufacturing sector - secondary industry - which is still weak, and that is the part which is most dependent on overseas demand. That, then, is the weakest area of the economy at the moment. Q: How far down the road is China in terms of shifting from an export-led economy to one which is driven by internal consumer demand? A: China has a long way to go still on that track. On the official figures, China's consumption is only 35% of GDP, compared with, say, 70% in the United States or the UK. Those figures slightly understate the amount of consumption expenditure, because they leave out certain things like housing and medical expenses. Even so, China has a long way to go. Investment expenditure is still nearly 50% of GDP, so it will take a long time for China to reorient its economy. The important thing, however, is that they are now reaching a point in their external accounts where prices, wages and the currency level together are making them rather less competitive than they were and, therefore, the trade surplus has been diminishing. That is helping the rebalancing but it will take a number of years to restructure the economy. Q: There is talk about non-performing loans in China. Will that cause any major issues as far as the Chinese banking system is concerned? Would the Chinese authorities step in if necessary? A: It has already caused some issues. The underperformance of the Chinese banks has been notable in the last few months, and is certainly reflecting worries about non-performing loans. The official figures for non-performing loans - from the CBRC, the Chinese banking regulator - significantly understate, in my view, the extent of the non-performing loans. As we saw in the 1990s, following the bubble of the early 1990s, China had a long tail of non-performing loans in the banking system, and the reason why, I think, the overall Chinese stock market has been so weak has been around concerns with the health of the banking system. It is not surprising: China created credit growth of 50% over a two-year period. No economy can generate that amount of money and credit and not expect some of those loans to have gone into the wrong hands. We have not yet seen those bad loans show up on the books of the banks, at least in terms of proper accounting process. United States Q: Why does the United States, using the same currency across states with widely differing economies, seem to work so much better than the eurozone? What is th ekey difference? A: The US has a matching fiscal and monetary union, but what is interesting is that the fiscal union preceded the monetary union. This was as a result of the work of Alexander Hamilton after the War of Independence in the 1790s; the US did not achieve a monetary union until after the Civil War in the 1860s, so, fiscal union first, monetary union second. There are two things, I think, which are important about the difference between the US monetary union and the European monetary union: first of all, within the United States, labour and capital are far more mobile. If there is unemployment in Alabama or in Louisiana, it is much easier for workers to move to where the jobs are - say in California or Alaska - and the language and cultural differences are much less. The second thing is that, if there is unemployment in one particular part of the United States, the unemployment benefits and the unemployment insurance are paid by the federal government, not by the state government, so it does not accentuate or cause the state government's finances to deteriorate. In terms of the eurozone, however, it is the Irish government which is paying the Irish unemployment benefits and the Portuguese government which is paying the Portuguese unemployment benefits and, therefore, worsening their own fiscal situation. Thus, labour and capital mobility and the different form in which the fiscal transfers occur -- the lack of a central fiscaltransfer system in Europe -- is the key flaw. Q: You are describing a situation which would not easily be replicated in Europe. A: Not until member states agree to give up much more fiscal sovereignty. Q: Is the US fiscal cliff a bigger potential concern, ultimately, than the eurozone sovereign-debt crisis? A: No, I do not think it is. I think the eurozone sovereign-debt crisis is a much bigger concern, but the US fiscal-cliff problem is significant. It consists of two parts: there are mandated plans for tax increases amounting to $425 billion and spending cuts of approximately $90 billion. Together, that is $515 billion of narrowing of the budget deficit to be implemented semi-automatically from January. That amounts to a cut in spending of about 3.5% of GDP. In practice, depending on the results of the election, it is highly likely that the Congress will take action to mitigate the impact of those cuts. We cannot, of course, be sure of that, but it would certainly be quite a shock, albeit it a temporary one. The US would then resume some sort of subpar growth rate, but the impact would not be as serious as the ongoing European problems. Q: The US does not seem yet to have addressed the issue of their budget deficit. Do you attribute this to political reasons only or is there any economic explanation behind it? If we eventually see austerity measures in the US, what will be the first steps and how do you think the markets will react? A: I think the US has not addressed the fiscal problem. It has not adopted austerity. On the part of the Obama administration, I think that is deliberate. On the part of the Congress, they have fought it and the Republican bias there has wanted to cut expenditures more drastically, but I think, if we step back for a moment, the key thing is this: the US entered this global downturn less leveraged and with a lower level of government expenditure than countries in Europe, or the UK for that matter. The UK went into this downturn more leveraged and with much larger government expenditure. For example, in the UK, government expenditure is currently in excess of 50% of GDP; in the US, it is only about 40% of GDP, so there is a significant margin of difference there. The other thing is that the banks and the financial system in the US, helped partly by the TARP and the US government programmes, have recapitalised themselves much more rapidly - balance sheets have been repaired more rapidly - and, as a result, we are seeing the US balance-sheet repair process much further ahead than it is either in the UK or in the eurozone. Q: Interestingly, the US appears to be growing somewhat and is not just relying on an austerity programme. Does this mean that the UK has it wrong? Is austerity the answer for the UK economy or should we be focusing more on trying to create growth? Is it possible to do both at the same time? A: The core problem is balance-sheet repair. Even if the Government were to spend a lot of money and run large deficits, very quickly UK fiscal credibility would be questioned and the yields on gilts, I think, would start to move up, which would affect mortgage rates and commercial borrowing rates for ordinary families and businesses. There are, then, distinct limits on what the Government can do in that respect. Just as the banks are having difficulty in increasing their lending while they are building up their capital, so it is for individuals and households. You cannot both spend a lot and pay down your debt at the same time, so one thing really has to precede the other. Balance-sheet repair needs to come first; then we can resume growth. Q: Is quantitative easing (QE) just about fixing the banks rather than fixing the economy, or is it possible to fix both at the same time? A: I do not think that QE is about fixing the banks; QE is about preventing the money supply from contracting. The big problem in the 1930s in America was that the money supply contracted by about one third, which precipitated deflation and a very weak economy for a long period of time. In the UK today, the stock of money - M4, as the Bank of England calls it - is still declining, so QE is helping to counter that. It is creating money to replace the money which is being limited or reduced by debt repayment. Deleveraging requires some degree of QE to counter its effects. As long as we are in a deleveraging phase, it is likely that the Bank of England may have to continue with QE. Yes, QE helps bank margins and, in turn, it will help commercial borrowers borrow more cheaply, but it is not solely about fixing the banks.

Q: What is the outlook for UK interest rates and for inflation? A: I think both are going to remain pretty low. The basic reason for low interest rates is not that the Bank of England is creating more money. As I just said, the amount of money in the system is contracting. The basic reason for low interest rates is deleveraging. The demand for credit is declining; people do not want to borrow and they are repaying debt rather than borrowing. That is why the Government has been able to borrow so cheaply. As long as you have deleveraging going on, disinflation is likely to follow. Weak growth of money and credit is leading to much lower rates of inflation. Over the past two years, we had externally generated inflation: weak sterling, higher commodity prices and so on. I think that phase is largely over. Now what we are moving into is a phase of much lower inflation, as we have just seen in the latest figures, and I think, by the end of the year, inflation will be below target. That is because, over the past two years, there has essentially been zero growth of money and credit. In effect we have tight money and credit with low interest rates. I think interest rates are likely to remain low broadly until the deleveraging process is complete, and the inflation rate will also stay very low over a comparable time period. Q: What is driving US and UK sovereign-debt yields to such historically low levels? Is this a bubble or do you expect a reversal? What would cause that? A: No, I do not think it is a bubble at all. I think it is a consequence of the two factors I just mentioned: deleveraging both by the financial sector and by the household sector in both the US and in the UK. We saw very much the same sort of thing in Japan. You will be aware that interest rates in Japan have been very low for a very long period of time. We are basically reiterating or repeating that process. Deleveraging is inherently disinflationary. That is the first part of the answer.

The second part is that, with deleveraging, you get very low rates of growth of money and credit, as I have just explained, and that in turn means we are not going to have big surges of liquidity and boosts to prices in general. That is why it is very important for the Government to get inflation down, because, with low wage growth, we need even lower inflation in order to generate real wage growth. Q: Pulling all of this together, what do you think are the conclusions we can draw for the outlook for the global equity and bond markets?

A: It is all about balance-sheet repair: deleveraging by the private sector, by households and by financial institutions is leading to low interest rates and low demand for credit. That will produce very low policy interest rates, so Bank Rate will remain very close to zero. It is at 0.5% at the moment; we have 0.75% in the eurozone and even less than that in the US. As long as you have that and very low inflation, investors will be searching for yield. The search for yield means that, from an investment point of view, those companies, bonds and properties that can generate sustainable, stable and strong income will be attractive to investors. |

|

|

|

| Pricing Actuary | ||

| London - £120,000 Per Annum | ||

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Head of Capital | ||

| London - Negotiable | ||

| Portfolio Actuary | ||

| London - £140,000 Per Annum | ||

| Deputy Head of Capital | ||

| London - £140,000 Per Annum | ||

| Senior Pricing & Portfolio Management... | ||

| London - £150,000 Per Annum | ||

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Lead Capital Actuary | ||

| London - £150,000 Per Annum | ||

| Take the lead on capital oversight | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Be at the forefront of creative GI co... | ||

| London/hybrid 2-3dpw office-based - Negotiable | ||

| Remote Market and Credit Risk Calibra... | ||

| Remote - Negotiable | ||

| Contact us about a Capital Contract i... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Head of Insurance Risk | ||

| London - £160,000 Per Annum | ||

| Director - Pensions Risk Transfer (PRT) | ||

| London, Midlands, North West - hybrid working 2dpw in the office - Negotiable | ||

| Dip a toe into public sector work wit... | ||

| Flex / hybrid 2 days p/w office-based - Negotiable | ||

| P&C Consultant | ||

| London / hybrid 3dpw office-based - Negotiable | ||

| Take the lead client-facing projects ... | ||

| Various locations - Negotiable | ||

| Choose Life! Choose a major global co... | ||

| Various locations - Negotiable | ||

| Actuarial skillset? Apply now for Snr... | ||

| South East / hybrid with travel requirements - Negotiable | ||

| Financial Risk Leader - ALM Oversight | ||

| Flex / hybrid - Negotiable | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd