|

|

Fueled by the rapid growth in sophisticated technologies like artificial intelligence (AI), the ever-changing landscape of cyber risk can make reserving for cyber insurance claims incredibly challenging. This article discusses the current UK cyber insurance covers and market, outlines the key challenges, and analyses reserving methodologies. Lastly, we discuss risk mitigation strategies that can help minimise cyber risk exposure, which could, in turn, reduce reserve uncertainty. |

Cyber threat is one of the biggest loss scenarios for UK businesses. A cyber attack can cripple the whole business operation and expose the business to litigation from its customers or other external stakeholders for causing data breaches. Below are some statistics to reflect the magnitude and frequency of the cyber attacks impacting the UK and global economy:

First party cover

Third party cover

Exclusions

Global cyber insurance premium trend

The cyber insurance market experienced steady growth between 2012 and 2020, and, due to low claims costs, insurers could keep the premium low during this period to increase their market share. However, in 2017, the world started to experience large cyber attacks, including the two largest attacks to date in terms of loss, the NotPetya and WannaCry ransomware attacks which happened in 2017, causing global losses of $10bn and $4bn, respectively. Alongside this, in 2018, the EU started the implementation of the General Data Protection Regulation (GDPR) and imposed a hefty fine of twenty million euros or 4% of annual turnover for breaching these data regulations. These recent events compelled the insurance industry to move from its low premium-high market share strategy to a high premium-hard market strategy. Insurance firms significantly increased cyber insurance premiums from 2020 to 2023 to maintain profitability. Insurance companies added more exclusions to their cyber insurance covers. They adjusted their policy wordings and terms and conditions following the Prudential Regulation Authority’s (PRA) Dear CEO letter in 2019 and Lloyd’s market bulletin in 2019. (Details of these documents are provided in Silent Cyber section of this article). This resulted in a reduction in claims frequency and severity between 2020 to 2023. Despite the falling trend of claim incidence, future premium growth is expected for cyber.

Key challenges and considerations

Lack of available and credible data and long tailed nature of cyber insurance claims

Accumulation of risk

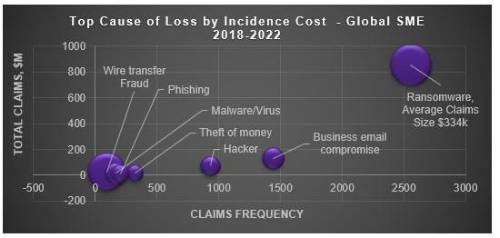

Ransomware

Silent Cyber In 2017, the PRA published its "Supervisory statement SS4/17 - Cyber insurance underwriting risk ”, in which the PRA recommended that Solvency II insurers should introduce robust wording exclusions to manage Silent Cyber exposure. As a follow-up to the SS4/17 supervisory statement, in 2018, the PRA surveyed UK insurers and published the results of the survey in 2019 in its “Dear CEO Letter: Cyber underwriting risk , providing an opinion that the UK insurers’ response to managing the Silent Cyber exposure was not adequate and advising firms to increase their activity in this area. In line with the PRA’s expectations, Lloyd’s published a bulletin Ref: Y5258, setting out requirements for Lloyd’s underwriters to explicitly put the wording in the terms and conditions of the insurance contracts to exclude or include the coverage of cyber risk. They wanted this to be implemented in phases: for the first-party property damages policies through phase 1, starting from the beginning of 2020, and other liability classes and reinsurance treaties through phases 2 and 3 in 2020/2021. The London Market Association (LMA) also produced sample wording for one hundred model classes for seventy lines of businesses in Lloyd’s. This initiative aimed to reduce the uncertainty around the risk exposure and create a more robust estimation of future claims cost. Moreover, the Institute and Faculty of Actuaries (IFoA) Cyber Risk Investigation Working Party produced a Silent Cyber Assessment Framework, which provides a detailed process for identifying silent cyber exposures in non-affirmative cyber policies. Due to the volatile cyber landscape, some exclusions might still be loosely defined, creating scope for coverage disputes. Such disputes and the resulting litigation can significantly lengthen the tail of cyber exposures.

State-backed cyber attack exclusion In bulletin Ref: Y5381, Lloyd’s stated its requirement for the syndicates offering stand-alone cyber policies to add a suitable clause to exclude liability for losses arising from state-backed cyber attacks. Lloyd’s also recommended that other non-cyber policies should include clauses and robust wording to exclude cyber attack exposures arising from war and non-war state-backed cyber attacks. That was a significant development in limiting cyber risk exposure from war and non-war state-backed cyber attacks. However, it would be extremely difficult to prove that an attack was state-backed because countries would participate in this form of warfare in such a way as to make their participation discreet.

Post-COVID-19 working environment

Geo-political risk

Cyber reserving methods For less developed claims or in the earlier years of the claims development, an exposure based method like the Expected loss ratio (ELR) method can be used with a blended approach of deriving (or selecting, where appropriate) the loss ratios from pricing or benchmark sources. Another exposure based method would estimate Incurred but Not Reported (IBNR) as a percentage of premiums written for different development years using benchmarks derived from market practice or specialist knowledge. For more developed years, claims development methods like Chain Ladder can be applied with benchmark claims development factors or a blend between the factors based on historical data and benchmark development factors. Different loadings can be applied to existing methods to make an allowance for large or catastrophe claims. For example, benchmark cat loads, derived from market practice or specialist knowledge, can be applied within the ELRs to estimate the catastrophe cyber reserves. This can be viewed as a contingency reserve, which can reduce the pressure on free reserve requirements under the Solvency II regime. Similarly, the full cyber risk exposure has to be considered when Technical Provision (TP) are calculated under the Solvency II and Lloyd’s requirements. TPs are based on the best estimate, including the Events Not in the Data (ENIDs), which includes the risk arising from exposure to cyber loss events that are not reflected in the historical claims experience. Another useful reserving method is frequency-severity modelling, which models the frequency and severity of the claims separately to estimate the total expected losses. In its IRIS 2022 report (IRIS-2022 Information Risk Insights Study ), Cyentia analysed ten years of data between 2012 and 2021 to construct both frequency and severity models and provide useful statistics for the cyber insurance market. Insurers can use rolling annualised data each month to increase the number of observations and improve the model's predictive ability. The underlying model chosen is the Poisson Log-Normal for frequency and Log-Normal for the claim severity. The parameters are determined using the maximum likelihood method and running the Kolmogorov-Smirnov test and the Cramér-von Mises statistical tests to analyse goodness of fit (Parameters used for these models can be found in IRIS-2022 Information Risk Insights Study ).

Validating Reserve Adequacy

Simulation methods

Scenario analysis The maximum and average loss for a scenario related to a cyber threat can be estimated based on historical events and industry trends and discussions with experts from internal sources like claims, underwriting and risk management teams or external experts. Examples of modelled scenarios could be business interruption (caused by ransomware attacks), service provider outages and data breaches. Some scenarios could be interconnected, so a correlation matrix needs to be constructed to explain the dependencies between these scenarios. This matrix could be estimated by analysing any historical loss events of a similar nature and talking to experts from IT and the claims departments. Allowing for correlations between different scenarios will capture the accumulation of risk. The scenarios and the correlation matrix can then be used as input for Monte Carlo simulations.

Exceedance Probability Curve

Tail risk

Reserve risk mitigation strategies.

Controls

Marsh Commercial has identified the following key controls to strengthen a Company’s cyber security:

Reinsurance

According to The Geneva Association , the following initiatives could increase the cyber reinsurance market:

In a nutshell |

|

|

|

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Head of Capital | ||

| London - Negotiable | ||

| Portfolio Actuary | ||

| London - £140,000 Per Annum | ||

| Deputy Head of Capital | ||

| London - £140,000 Per Annum | ||

| Senior Pricing & Portfolio Management... | ||

| London - £150,000 Per Annum | ||

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Lead Capital Actuary | ||

| London - £150,000 Per Annum | ||

| Take the lead on capital oversight | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Be at the forefront of creative GI co... | ||

| London/hybrid 2-3dpw office-based - Negotiable | ||

| Remote Market and Credit Risk Calibra... | ||

| Remote - Negotiable | ||

| Contact us about a Capital Contract i... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Head of Insurance Risk | ||

| London - £160,000 Per Annum | ||

| Director - Pensions Risk Transfer (PRT) | ||

| London, Midlands, North West - hybrid working 2dpw in the office - Negotiable | ||

| Dip a toe into public sector work wit... | ||

| Flex / hybrid 2 days p/w office-based - Negotiable | ||

| P&C Consultant | ||

| London / hybrid 3dpw office-based - Negotiable | ||

| Take the lead client-facing projects ... | ||

| Various locations - Negotiable | ||

| Choose Life! Choose a major global co... | ||

| Various locations - Negotiable | ||

| Actuarial skillset? Apply now for Snr... | ||

| South East / hybrid with travel requirements - Negotiable | ||

| Financial Risk Leader - ALM Oversight | ||

| Flex / hybrid - Negotiable | ||

| Be the very model of a modern Capital... | ||

| London - Negotiable | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd

By Lynette Calitz, Actuarial and Risk Director and Shamsul Haque, Actuarial and Risk Assistant Manager at Grant Thornton

By Lynette Calitz, Actuarial and Risk Director and Shamsul Haque, Actuarial and Risk Assistant Manager at Grant Thornton