|

|

The assumptions that need to be made as part of the Local Government Pension Scheme (LGPS) valuation process are varied and many. For example, what investment returns will the Fund achieve in future? What are members going to be earning? How long will they live? |

By Matthew Paton FFA, Actuary at Barnett Waddingham

The process of setting an assumption is rather like setting sail in stormy seas

We know where we want to get to (a well-funded pension scheme!) but it is very likely we will need to change course from time to time in order to get there. Nowhere is this better illustrated than in the process of setting mortality assumptions. At the last valuation, we made an assumption about how long members will live. A few years on, are we still happy with our assumption or do we need to correct our course? Well, let’s climb into the crow’s nest and have a look at the sea of evidence to find out.

Specifically, we can have a look at the latest population data from England and Wales and identify any trends in the mortality statistics. Helpfully, the Continuous Mortality Investigation (CMI), a research arm of the Institute and Faculty of Actuaries, has carried out such an analysis for us and indeed they do so on an annual basis.

Their latest findings are that mortality rates in the population during 2018 were very similar to those in 2017. In other words, mortality improvements during 2018 were very low, with an overall improvement rate of just 0.2% for males and females combined.

This in fact continues a trend of lower mortality improvements which have been observed since 2011. The causes of this are not clear and these effects are currently the subject of much debate.

Knowing the ropes when determining life expectancies

To consider the impact on LGPS valuations, we need to briefly explore the mechanics of how we determine life expectancies. In a nutshell, the process can be summed up in three steps:

A standard “base” table of mortality rates is chosen which we think is a close match to the Fund’s actual mortality experience.

These tables are typically compiled by the CMI using a vast amount of data from self-administered pension schemes (SAPS).

However, as it takes some time to complete these investigations, the tables are already out of date by the time we can get our hands on them.

Our table therefore needs to be brought up to today’s date so we can estimate what current mortality rates might be. To do this, we can apply reductions to the historical mortality rates in line with recent improvements we have seen in the general population.

We then need to project these “current” mortality rates into the future, allowing for further potential improvements. Initially, we can continue to apply the same rate of improvements we have been seeing in the population recently. Over the longer term, however, much more judgement is required and it is by no means clear what the “long term rate” of mortality improvements might be, or indeed for how long improvements may continue at all. At the last set of triennial valuations, the most common assumption by LGPS actuaries was that the long term rate of improvement would be 1.5% p.a. which is currently higher than what we are seeing in general population data.

For steps 2 and 3, we use the CMI’s “projection model” which is updated on an annual basis, incorporating the latest mortality improvements in the population. Indeed, this is the model that is currently used by all of the LGPS actuarial firms in order to project mortality rates into the future and estimate the future chances of ending up in Davy Jones’ Locker. CMI 2018 was released in March 2019 and it is particularly significant as this is the model that will likely be used by most actuaries in the upcoming 2019 valuations for English and Welsh funds.

Taking the wind out of improvements in life expectancy

Given the slowdown over the last few years, the most recent versions of the model have been incorporating lower initial improvements. In other words, mortality rates in the early part of the projection have been edging upwards. As the overall life expectancy is a result of the combination of mortality rates at each age, the effect is that our estimate of life expectancies has been steadily reducing over the last few years.

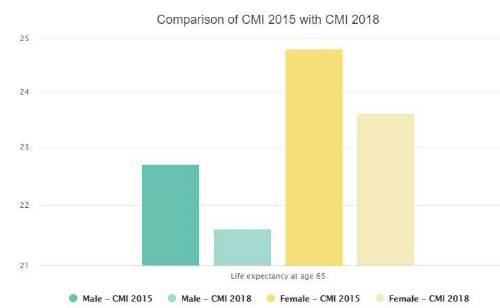

At the 2016 valuations of English and Welsh funds, CMI 2015 was adopted. Let’s now compare CMI 2015 with CMI 2018 and see what the impact on liabilities might be at the 2019 valuation:

As at 1 March 2019, using the S2PA tables and a long term rate of 1.5% p.a.

As can be seen, life expectancies at age 65 are around 13 months shorter for males and 14 months shorter for females, compared with the model adopted at the 2016 triennial valuations. All else being equal, for a typical LGPS fund this could reduce liabilities by around 3%-5%, a welcome tailwind speeding us on to port. Yo ho ho!

Let’s not go overboard

Of course, not everything else is equal so it is not quite “Land Ahoy!” yet. At the upcoming valuation, we are also likely to move to the S3 mortality tables and a full longevity analysis covering the last five years will be carried out for many of our funds, which will inform the precise choice of base table that we use. More details on both of these subjects can be found in our recent briefing note

Choosing the right mortality table for your Fund. Additionally, many other assumptions will be reviewed besides mortality which will affect liabilities. Given the recent pause in the “cost cap mechanism” and the McCloud judgement, there is even uncertainty regarding what the actual LGPS benefits are going to be. Perhaps another assumption we will need to make! Shiver me timbers!

One other change to the core version of the CMI 2018 model is that slightly more weight is now being given to mortality data in recent years compared with before. This is because there is a growing consensus that the slower mortality improvements we are currently seeing are part of a new trend rather than a short term fluctuation. This change accounts for a significant amount of the reduction in overall life expectancies we can see above.

In conclusion, we are expecting that changes to the post-retirement mortality assumptions, all else being equal, will lead to a small improvement in the funding position for most funds at the 2019 valuations. A lot of thought certainly needs to be given to the long term rate of improvement. There is still much uncertainty as to whether the current low levels of mortality improvements will continue for the foreseeable future and it would seem reasonable to remain cautious for the time being.

There is also much evidence out there to suggest that members of self-administered pension schemes experience a significantly higher level of mortality improvements than the general population (on which the CMI projection model is based), perhaps reflecting the better quality of life in retirement that people enjoy when they have additional pension provision. Therefore, we will also need to think about whether the level of initial improvements in the CMI model is appropriate. Arrr!

Whilst it is not all plain sailing, the good ship Barnett Waddingham will be steaming ahead with the 2019 valuations over the coming months. As part of this we will be working with funds to determine a mortality assumption that is entirely tailored to their own membership, so look out for us in a port near you soon!

Sources: CMI Working Papers 115 and 119.

|

|

|

|

| START-UP, Lead Reinsurance Actuary | ||

| London - Negotiable | ||

| Senior Actuary | ||

| London - Negotiable | ||

| Reserving Manager | ||

| London - £130,000 Per Annum | ||

| Senior Reserving Consultant | ||

| London - £100,000 Per Annum | ||

| Head of Capital | ||

| London - £180,000 Per Annum | ||

| Head of Portfolio Optimisation | ||

| London - Negotiable | ||

| Pricing Lead/Manager | ||

| London - £130,000 Per Annum | ||

| Actuary | ||

| London/Hybrid - Negotiable | ||

| Capital Actuary | ||

| London - £110,000 Per Annum | ||

| Senior Reserving Actuary | ||

| London - Negotiable | ||

| Head of Capital | ||

| London/Hybrid - Negotiable | ||

| Head of Pricing | ||

| London - £170,000 Per Annum | ||

| Pricing Actuary | ||

| London - £120,000 Per Annum | ||

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Head of Capital | ||

| London - Negotiable | ||

| Portfolio Actuary | ||

| London - £140,000 Per Annum | ||

| Deputy Head of Capital | ||

| London - £140,000 Per Annum | ||

| Senior Pricing & Portfolio Management... | ||

| London - £150,000 Per Annum | ||

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Lead Capital Actuary | ||

| London - £150,000 Per Annum | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd