|

|

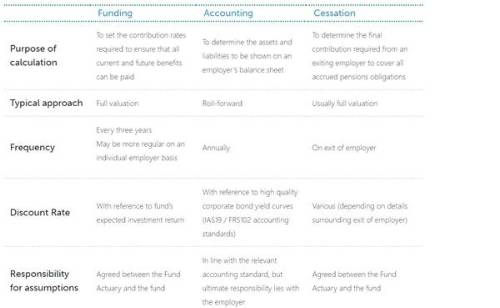

Each employer who participates in the Local Government Pension Scheme (LGPS) is subject to a number of different actuarial valuations of their pension obligations. The three main types of actuarial valuation in the LGPS which are covered are: Funding valuation, Accounting valuation and cessation valuation. This article sets out their purpose and how they differ in practice. The main point made throughout is that each type of valuation is answering a particular question and will give a (sometimes vastly) different result. |

By Roisin McGuire FFA, Associate and Actuary at Barnett Waddingham

What is an actuarial valuation?

An actuarial valuation involves determining the value of pension benefits that have been accrued by LGPS members and comparing this to the value of the assets held in respect of these pension benefits.

When carrying out a funding valuation, we receive data for each individual member and information on their accrued pension benefits. We then project each members’ benefits into the future based on a set of assumptions (e.g. salary increases and pension increases) and allowing for the probability that these future benefits will be paid (e.g. the probability of a death benefit being paid on a death in active service). Through an approach known as ‘discounting’, these projected benefit cashflows are summarised into a figure known as the “present value of obligations”, or more commonly the “liability”, and this represents the value of the future benefits at the current valuation date. A discount rate assumption is used which represents the future investment return on the fund’s assets. The lower the discount rate assumption is (with all else being equal), the higher the value of liabilities. The approach used to set the discount rate assumption is one of the main differences between the various types of actuarial valuations. In the case of accounting valuations where timescales are tight for delivering reports, a full valuation of member data is not plausible and therefore a roll forward approach is usually adopted instead. A roll-forward approach involves estimating an employer’s assets and liabilities from the latest full valuation (i.e. using individual member data) which was carried out. This involves using cashflow information to estimate changes in the assets and liabilities since the latest full valuation. The assets and the liabilities are then compared. If the assets are more than the liabilities then there is a surplus and if they are less than the liabilities then there is a deficit. Summary: Key features of each type of valuation

Funding valuation A funding valuation is typically carried out every three years as required by LGPS regulations to assess the ongoing financial position of the LGPS fund and its employers and review the contribution rates payable. Funding valuations can also happen when a new employer joins the fund.

Assumptions At BW we build a margin of prudence into the discount rate assumption which provides a cushion for experience being worse than expected. When setting all other assumptions at each triennial valuation, the BW standard approach is to set these on a best-estimate-basis, which means that each assumption is neither cautious nor optimistic and there’s an equal likelihood that the actual experience will be higher or lower than the assumption set.

Results Another key result from the valuation is the contributions required to be paid by the employer: The primary rate is the cost of accruing future benefits in respect of the current active members. This may be an open rate, i.e. allowing for new entrants, or a closed rate, i.e. assuming no new entrants. The secondary rate is an adjustment to the primary rate base on the employer’s specific circumstances. Secondary contributions are commonly required for the repayment of any deficit, so these are sometimes referred to as deficit contributions. The total required contributions are the sum of the primary and secondary contributions.

Accounting valuations The main accounting standards which apply to pension schemes in the UK are FRS102 or IAS19. FRS102/IAS19 are standards which apply to nearly all employers with a defined benefit pension scheme and one of the objectives of these standards is to allow the pension obligations of different employers to be compared on a consistent and market-related basis. It is important to note that the accounting valuation has no effect on the contributions payable by the employer.

Assumptions The discount rate is one of the main differences between an accounting valuation and a funding valuation. Due to the different discount rate assumption being adopted, we would generally expect the accounting liabilities (and therefore the accounting deficit) to be higher than when measured on the funding basis. Other differences between an accounting valuation and funding valuation include: The accounting standards require unbiased (neither imprudent nor excessively conservative) assumptions to be used whereas there is no specific requirement for the funding valuation. The accounting assumptions are ultimately the responsibility of the employer whereas those in the funding valuation are the responsibility of the Fund Actuary. In particular, the funding valuation will usually use the same set of assumptions for all employers whereas more specific assumptions can be used for the accounts. This may lead to differences in the assumptions used if the employer believes that other assumptions are more appropriate.

Results If an employer would like to see the effect of a change of assumptions on their accounting position, please let your usual BW contact know, as we can provide a modeller for this purpose.

Cessation valuations When an employer ceases participation in the LGPS, the Fund Actuary is required to carry out a cessation valuation. Depending on the details surrounding the employer’s exit and the fund’s Funding Strategy Statement, a wide variety of approaches may be taken.

Assumptions If this is no longer possible because an employer has left and no employer will become responsible for the accrued pension benefits, then the Fund Actuary may deem it appropriate to carry out the cessation valuation without allowing for this investment risk, and instead adopting a “minimum risk basis”. A minimum risk basis may use gilt yields as the discount rate. This will likely result in liabilities higher than under the accounting and funding bases as gilt yields are generally lower than the discount rates adopted for those bases. This approach can be compared to the private sector where employers secure their pension liabilities with an insurance company and similar principles are used by insurers to price such transactions.

Results The LGPS Regulations also give funds the power to offer some flexibility in making these exit payments, for example spreading the payment across a fixed period, or for the employer to remain in the fund as a deferred employer and to continue meeting its obligations on an ongoing basis. |

|

|

|

| START-UP, Lead Reinsurance Actuary | ||

| London - Negotiable | ||

| Senior Actuary | ||

| London - Negotiable | ||

| Reserving Manager | ||

| London - £130,000 Per Annum | ||

| Senior Reserving Consultant | ||

| London - £100,000 Per Annum | ||

| Head of Capital | ||

| London - £180,000 Per Annum | ||

| Head of Portfolio Optimisation | ||

| London - Negotiable | ||

| Pricing Lead/Manager | ||

| London - £130,000 Per Annum | ||

| Actuary | ||

| London/Hybrid - Negotiable | ||

| Capital Actuary | ||

| London - £110,000 Per Annum | ||

| Senior Reserving Actuary | ||

| London - Negotiable | ||

| Head of Capital | ||

| London/Hybrid - Negotiable | ||

| Head of Pricing | ||

| London - £170,000 Per Annum | ||

| Pricing Actuary | ||

| London - £120,000 Per Annum | ||

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Head of Capital | ||

| London - Negotiable | ||

| Portfolio Actuary | ||

| London - £140,000 Per Annum | ||

| Deputy Head of Capital | ||

| London - £140,000 Per Annum | ||

| Senior Pricing & Portfolio Management... | ||

| London - £150,000 Per Annum | ||

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Lead Capital Actuary | ||

| London - £150,000 Per Annum | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd